Do I Need Special Auto Insurance to Modify My Car?

According to the Specialty Equipment Market Association, consumers spent a whopping $52.65 billion in 2024 on automotive specialty equipment parts and accessories. But once you add features or modify your car—whether it’s a custom paint job or a major performance modification like a supercharger–-you will likely need to get special auto insurance coverage, either as an endorsement or separate policy.

Find Cheap Car Insurance Quotes in Your Area

Modifications a standard policy will and won't cover

The terms modification and customization are often interchangeably used in the car industry and basically mean the same thing. These are changes or additions made after the car has left the factory — including aftermarket parts — and they are typically excluded from standard insurance policies.

Some insurers regard an automobile as customized or modified when the chassis, body and/or frame are structurally enhanced, the car's performance is considerably augmented or the value of a custom paint job exceeds several thousands of dollars.

"An auto insurance company generally does not provide any coverage for enhancements to an automobile. The exception is tires and rims — for which you’ll need to furnish receipts, and even then only a portion of their value will typically be reimbursed in a loss settlement," says Christopher Paradiso, owner of Connecticut-based Paradiso Insurance. Paradiso adds that vehicle value is typically based on the factory-installed components of the vehicle.

The coverage you need for customizations

Although a standard policy won't reimburse the value of a customization if you need to file a loss claim, you may have two options:

- Supplemental coverage: Many insurers offer endorsements that provide supplemental coverage for modifications and aftermarket components. For example, Esurance offers an optional customized parts and equipment coverage that will pay up to $4,000 if those parts or equipment are damaged and need to be repaired or replaced. Depending on the insurer, the premium for this extra coverage can equate to approximately 10% of the value of the modifications.

- Classic/collectible car insurance: Some insurance companies specialize in policies for exotic, antique or modified cars. This includes companies like Hagerty, J.C. Taylor, Condon Skelly, Grundy and American National. The coverage limits may be higher with this option than for supplemental coverage.

Insurance considerations before modifying your car

Before tricking out your ride — or even making a minor modification — consider the following:

- Read your existing policy thoroughly to understand coverage exclusions and exceptions.

- Consult with your insurer. "Let your agent know if you plan to make changes to your vehicle at any time before or during the policy term," says Kristofer Kirchen, president of Tampa, Florida-based Advanced Insurance Managers, LLC.

- Ask for clarifications in writing. To ensure that your modifications are properly covered, ask your agent to clarify any confusing policy language and request that confirmation in a written letter, email or document. Your insurer is obligated to honor whatever its agent promises you in writing.

- Don't hide a customization from your insurer. "If your car is worth more after being modified, and you’re involved in an accident and the car isn't insured for the right amount, you’ll only be paid for the car based on its original amount, as the losses weren't originally priced in the policy," says Loretta Worters, a vice president at the Insurance Information Institute. Even worse, your insurer may cancel/void your policy and deny the claim because you didn't disclose the customizations, which can be considered a "material misrepresentation" for which they can legally drop you as a customer. That would leave you on the hook for paying for losses out of your own pocket.

- Ponder cost and risk factors carefully. Even if your insurer covers you, it may result in a higher annual increase in your premiums.

Find Cheap Car Insurance Quotes in Your Area

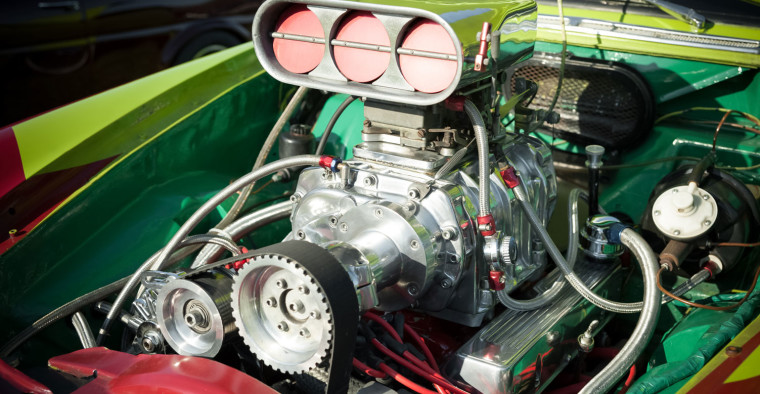

Common customizations

Examples of popular modifications that drivers make to their vehicles, and which usually require supplemental or separate insurance, include:

- Custom paint job, murals, graphics or decals

- Electronic equipment like a custom stereo, PC, TV or video system

- Custom tires, wheels or spinners

- Custom spoilers, louvers, scoops or grilles

- Speed enhancements like turbochargers, blowers and strokers

- Anti-roll/anti-sway bars or winches

- Added chrome

- Accent/auxiliary lights

- Suspension enhancers or hydraulics

About the Author

Senior Insurance Analyst

Mark is a former Senior Research Analyst for ValuePenguin focusing on the insurance industry, primarily auto insurance. He previously worked in financial risk management at State Street Corporation.

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.