Best Medicare Supplement (Medigap) Plans for 2026

The best Medicare Supplement is Plan G from AARP/UnitedHealthcare. It has cheap rates and great coverage.

Best Medicare Supplement Plans

If you're intimidated by Medigap or not sure where to start, take a look at Plan G first.

Plan G is the best Medicare Supplement policy for most people because it pays for nearly all your health care costs Medicare doesn't cover. Plan G has an average price of $180 per month for 2026.

AARP/UnitedHealthcare is the best company overall for Medicare Supplement (Medigap) plans because of its low rates and valuable extras.

What is the best Medicare Supplement plan in 2026?

Plan G is the best Medicare Supplement policy for most people.

Plan F offers the most coverage of any Medicare Supplement option, but you can only buy it if you became eligible for Medicare before Jan. 1, 2020. If you can get Plan F, it could be a great option. But if you're new to Medicare, start by looking at Plan G.

Plan F vs. Plan G

Plan F often doesn't make sense because it can cost you more overall than Plan G, on average.

That's because Plan G has the same coverage as Plan F, except Plan G won't pay your $283 Medicare Part B deductible. Because Plan F costs an average of $564 per year more than Plan G, you will often spend more money than you'd save with Plan F.

As you compare Medicare Supplement insurance plans, think about how much medical care you need, how often you go to the doctor and how much you can afford to pay toward your medical bills yourself. Each Medigap plan has a different level of coverage, so you should find one that fits your specific needs.

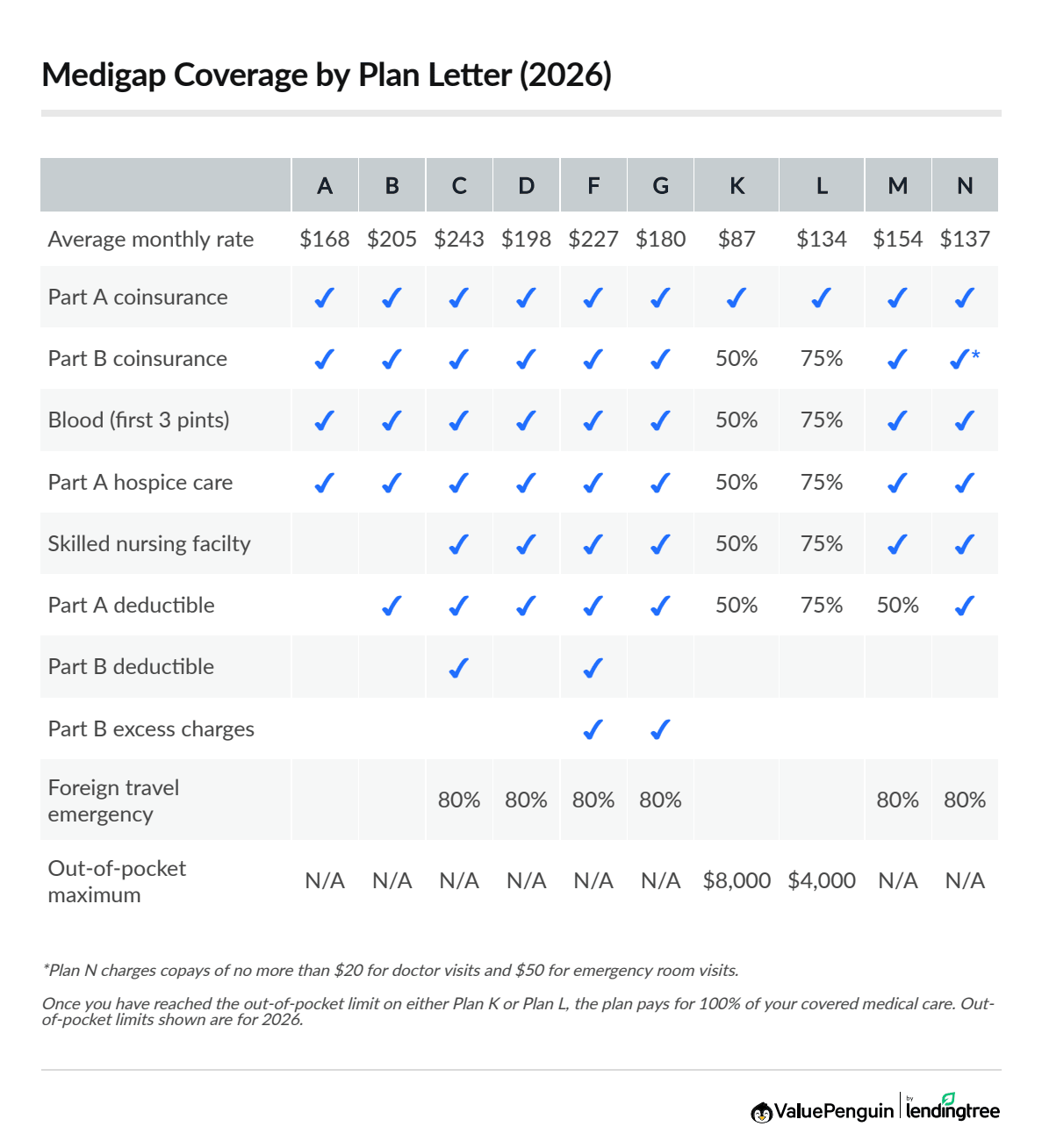

Medicare Supplement comparison tables

Click the image below to download a PDF version of ValuePenguin's Medigap comparison chart.

With Original Medicare (Parts A and B), you're responsible for paying roughly 20% of your hospital bills.

Medigap plans pay for some or all of your remaining costs, depending on your plan letter. Without a Medigap plan, you might have to pay very high medical costs.

The best Medicare Supplement plan for you depends on your health and budget.

Medigap Supplement comparison tables

Average costs are for a 65-year-old woman who doesn't smoke. Rates vary by location, age, gender and other factors.

Plan A | Plan B | Plan C | Plan D | Plan K | Plan L | Plan M | |

|---|---|---|---|---|---|---|---|

| Monthly cost | $168 | $205 | $243 | $198 | $87 | $134 | $154 |

| Part A coinsurance | |||||||

| Part B coinsurance | 50% | 75% | |||||

| Blood (3 pints) | 50% | 75% | |||||

| Part A hospice care | 50% | 75% | |||||

| Skilled nursing facility | 50% | 75% | |||||

| Part A deductible | 50% | 75% | 50% | ||||

| Part B deductible | |||||||

| Part B excess charges | |||||||

| Foreign travel emergency | 80% | 80% | 80% |

Average costs are for a 65-year-old woman who doesn't smoke. Rates vary by location, age, gender and other factors.

- Plan G is good for people who want very few medical bills and are willing to pay more each month to avoid them. This can give you peace of mind because you won't be surprised by high medical costs. However, a cheaper Medicare Supplement plan may make better sense if you don't visit the doctor often.

-

Plans F and C have better coverage than Plan G, but you can't get them if you're a new enrollee. Plus, these plans might not save you money because of their high monthly rates.

Switching Medigap plans isn't easy, so picking the right plan when you first sign up is important. Insurance companies can use your health history if you get a plan outside the six months around your 65th birthday, called the "initial enrollment period." If you buy a plan with low coverage when you're 65 and later decide to upgrade to something better, such as Plan G, companies may quote you a high rate or deny you coverage entirely.

Best Medigap plan for seniors: Plan G

Plan G has the best coverage for most seniors and others on Medicare.

Plan G will pay all your Medicare-related costs except for the $283 Medicare Part B deductible. After you pay this, Plan G will pay for medical care such as doctor visits, blood tests or outpatient medical treatment.

- Popular plan that covers nearly all of your health costs

- Often a better value than Plan F

- Rates can be expensive, at $180 per month, on average

- Cheaper plans may be a better deal if you rarely visit the doctor

Best Medicare Supplement for complete coverage: Plan F

Plan F has the best coverage of any Medigap plan overall.

But you can only buy Plan F if you were able to get Medicare before Jan. 1, 2020. Plan F covers all of your Medicare costs that you would normally pay for out of pocket, including deductibles, copays and coinsurance.

- Pays for nearly all medical costs

- High monthly rates

- Not available to new Medicare enrollees

Best affordable option with good coverage: Plan N

Plan N has similar coverage to Plan G but costs less.

Plan N is a budget-friendly option with coverage that's nearly as good as Plan G but at a cheaper rate. With Plan N, you have to pay $20 for doctor visits and $50 for trips to the emergency room. Plan N also doesn't cover what's called Medicare Part B excess charges.

-

Covers nearly all of the costs you're responsible for with Medicare

-

Plan N costs about $137 per month, which is $43 per month less than Plan G

- Extra costs you're responsible for paying when you visit the doctor could cancel out savings

- You may have extra fees if your doctor doesn't accept the prices set by Medicare

Cheapest Medicare Supplement plan: High-deductible Plan G

High-deductible Plan G has the cheapest monthly rate of any Medigap policy.

A high-deductible Plan G policy costs just $52 per month, on average. The main downside to high-deductible Plan G is that before coverage starts, you have to pay $2,950 in medical costs, called a deductible.

A normal Plan G policy is cheaper than high-deductible Plan G coverage if you need a lot of medical care. Remember, companies can charge higher rates or deny coverage because of your health history if you change Medicare Supplement plans outside the six months around your 65th birthday. That means you may be stuck with a high-deductible Plan G when you're older and in worse health, costing you more in the long run.

- Cheap rates, at $52 per month on average

- Strong coverage after you've met your deductible

- You have to pay $2,950 each year before coverage starts

- Not the best deal if you need ongoing medical care

Neither Original Medicare nor a Medicare Supplement plan covers prescriptions. For that, you'll need a separate Medicare Part D plan.

Best Medicare Supplement companies

AARP/UnitedHealthcare is the best Medicare Supplement company overall because it has affordable rates and good customer satisfaction.

Medicare Supplement plans with the same letter have the same coverage no matter which company you choose. This means that Medicare Supplement Plan G from AARP/UnitedHealthcare gives you the same coverage as Plan G from Aetna, Blue Cross or any other company. However, different companies have different rates, customer service and plan experiences.

Best overall Medicare Supplement company: AARP/UnitedHealthcare

-

Cost of Plan G$177/moAverage rate for a 65-year-old woman

-

Medigap plans offered A, B, C, D, F, G,

high deductible G, K, L, N

Best for flexible coverage: Blue Cross Blue Shield (BCBS)

-

Cost of Plan G$189/moAverage rate for a 65-year-old woman

-

Medigap plans offered All plan letters,

including high-deductible F and high-deductible G

Best Medicare Supplement for customer service: Mutual of Omaha

-

Cost of Plan G$207/moAverage rate for a 65-year-old woman

-

Medigap plans offered A, B, C, D, F, G, M, N, HD-F, HD-G

What are the worst Medicare Supplement companies?

Blue CareFirst, Aflac and Medica stand out for having poor customer service for their Medigap plans.

Each company on this list gets far more complaints than an average company its size. It's a good idea to choose a company that gets few complaints because you're less likely to run into problems when you file a claim.

Company | Plan G cost |

Complaint rate

|

|---|---|---|

| Blue CareFirst | $171 | 9.4 times more than average |

| AFLAC | $161 | 6.9 times more than average |

| Medica | $164 | 6 times more than average |

| Avera | $305 | 5.1 times more than average |

| Humana | $195 | 4.5 times more than average |

Average monthly cost of Plan G

Humana is good for other types of plans, such as workplace coverage or Medicare Advantage. However, the company's Medigap plans are expensive and have a high rate of complaints.

How much does a Medicare Supplement plan cost?

Medicare Supplement plans cost $180 per month, on average, in 2026.

Medigap Plan G costs an average of $180 per month for a 65-year-old woman who doesn't smoke. These plans have the best coverage for seniors new to Medicare. A Medigap Plan G policy covers nearly all the costs you're normally responsible for with Medicare, except for the $283 per year Part B deductible.

Medigap Plan F costs $227 per month, on average, in 2026. Medigap Plan F usually doesn't make sense financially. That's because Plan G offers almost the same level of coverage but at a much lower cost.

Average cost of Medicare Supplement in 2026

High-deductible Plans F and G have the cheapest average monthly rates. A high-deductible Plan G costs only $52 per month, on average. However, that doesn't necessarily make it a good deal. That's because you have to pay $2,950 for medical care each year before coverage starts for either plan.

You're better off with a regular Plan G Medigap policy if you expect to consistently need a lot of medical care. A high-deductible Plan G policy might make sense if you are in good health and can easily afford to pay the $2,950 deductible from your savings.

Average cost of Medicare Supplement plans

Medigap plan | Monthly cost |

|---|---|

| F | $227 |

| G | $180 |

| N | $137 |

| Less popular plans |

Average rate for a 65-year-old woman who doesn't smoke

How much you pay is based on several factors, including:

- The plan you choose

- The company you choose

- Where you live

- Your age and gender (usually)

- Discounts you qualify for

- When you enrolled

Medicare Supplement plans in Massachusetts, Minnesota and Wisconsin

Massachusetts, Minnesota and Wisconsin have different Medicare Supplement plans than the rest of the country.

These states have fewer Medigap options than other states. However, in all three states, you can get coverage similar to Plan G.

In Massachusetts, you can choose between three different types of Medigap plans: Core, Supplement 1 and Supplement 1A. Supplement 1A is most similar to Medigap Plan G, making it a good choice for most people because it offers the most coverage.

The average cost of a Supplement 1A plan is $243.

In Minnesota, the best Medicare Supplement choice for most people is the Basic plan.

This plan offers a similar level of coverage as Medigap Plan G. The Basic plan covers almost all the costs you're responsible for with Original Medicare (Parts A and B). However, you may be responsible for some preventive services not covered by Medicare.

The average cost of a Basic health plan is $242 per month.

The Extended Basic plan offers even more coverage. It pays for your Medicare Part A deductible, foreign travel emergencies, preventive services not covered by Medicare and extra costs you're responsible for if your doctor doesn't accept the price set by Medicare.

However, this plan is usually not a good choice because of its high cost.

In Wisconsin, there's only one Medigap plan available, called Base Medigap.

Wisconsin Medigap customers have a lot of choices when it comes to personalizing their Base Medigap plans. In other words, you can build your own Medigap plan by adding coverage extras to your policy.

Base plans need to cover certain benefits like your Part A (hospital care) coinsurance or copay, 175 days of mental health inpatient care and some of the costs you're responsible for paying with Part B (doctor visits). Remember, this is the minimum level of coverage you can get. Many companies let you modify your policy with coverage extras, usually at a higher cost.

A Base Medigap plan costs $165 per month, on average.

You can choose a Base plan option with a lower monthly rate, but you'll pay more when you visit the doctor.

- High-deductible plans: You'll pay more before coverage starts.

- 25% cost-sharing plans: You'll pay roughly 25% of your medical costs, similar to Plan L.

- 50% cost-sharing plans: You'll pay roughly 50% of your medical costs, similar to Plan K.

How to choose the best Medicare Supplement plan

Choose a Medigap policy by comparing plan benefits and costs against the medical care you expect to need.

Decide how much coverage you need

Try to match your coverage with your specific medical needs. For example, it might not make sense to get a policy with excellent coverage like Plan G or F if you're in good health and you don't go to the doctor often. Instead, you could save money by choosing a less expensive option like high-deductible Plan G.

However, if you have a disability or ongoing illness, or you just want the peace of mind of having good coverage as you get older, you should choose a plan with better coverage like G, F or N. Even though these plans have higher average rates, you'll save money when you go to the hospital.

Keep in mind, it's difficult to change Medigap plans once you've bought one. If you want the flexibility to easily switch from a low-cost plan to a plan with better coverage, Blue Cross Blue Shield is the best option.

Its Blue to Blue rule means you can switch Medigap plans at any time without paying a higher rate because of your age or health status.

Compare companies to find the best combination of cost and quality

After choosing a plan, compare the Medigap companies in your area. In particular, look at price and customer service. Remember, plans have the same coverage if they have the same letter. So a Plan G will have the same coverage regardless of whether you buy it from AARP/UnitedHealthcare or Blue Cross Blue Shield.

While the coverage is the same, plan costs can differ by hundreds of dollars a year. Keep in mind that the cheapest plan isn't always the best option. You don't want to pick a company that has poor customer service, since that can lead to problems down the road.

Look for discounts and other ways to save

Before you pick a Medicare Supplement company, check to see if you can get discounts. For example, household discounts for married couples, civil partners and extended family members who live together are a common way to save. Some companies even extend this discount to roommates.

Depending on where you live, you may also have the option to choose a low-cost Medicare Select plan. These policies have the same coverage as a regular Medigap plan, but they restrict you to a network of doctors like an HMO.

Get in touch with a broker or buy directly through a Medicare Supplement company

You no longer need a broker to buy a Medigap policy. However, brokers can offer some advantages over a do-it-yourself approach because they have a strong understanding of the plans and prices in your area. Remember that your Medigap costs depend in part on where you live, and plan availability varies by county.

You can also buy a Medicare Supplement plan directly from a company's website. This is the quickest route to getting a Medigap policy. It's typically a good choice if you feel confident that you've identified the right plan and company for you.

Medicare Advantage vs. Medicare Supplement

What's the main difference between Medicare Advantage and Medicare Supplement plans?

A Medicare Advantage plan offers low-cost bundled coverage that includes all the services you'd get through regular Medicare along with extras like prescription drug coverage, vision, dental and fitness programs.

Medigap plans help you cover the medical costs that you're responsible for paying with Original Medicare (Parts A and B).

Is Medicare Advantage better than Medicare Supplement?

A Medicare Advantage plan is better if you want cheap monthly rates and bundled coverage.

On the other hand, you should consider a Medicare Supplement plan with Original Medicare if you value flexibility when it comes to choosing your doctor or if you think you'll need a lot of medical care in the future.

Why do people choose Medigap over Medicare Advantage?

Medicare Supplement (Medigap) plans give you greater flexibility when it comes to choosing your doctor compared to a Medicare Advantage plan. You also will likely pay less money overall with a Medigap plan if you need a lot of medical care.

Are Medigap rates going up?

The cost of Medigap Plan G went up by 13%, on average, between 2025 and 2026.

That's an increase of $21 per month, with average rates rising from $159 per month in 2025 to $180 per month in 2026.

Oklahoma had the largest average increase, at 22% year on year. The cost of a Medigap Plan G policy in OK rose from $130 to $158 per month, on average. Rhode Island, Missouri, Delaware and Hawaii had the lowest average increases, at 7% each.

State | 2025 rate | 2026 rate | % change |

|---|---|---|---|

| AK | $158 | $170 | 8% |

| AL | $142 | $162 | 14% |

| AR | $172 | $189 | 10% |

| AZ | $154 | $185 | 20% |

| CA | $182 | $202 | 11% |

All figures are monthly rates for a 65-year-old woman who doesn't smoke.

Nationally, the cost of a Medicare Supplement plan, across all plan letters, rose by an average of 10% between 2025 and 2026.

Plan F prices increased the most, at an average of 14%, while high-deductible Plan G increased the least, at 6% on average.

Medicare Supplement plan cost increase between 2025 and 2026

Medigap plan | 2025 cost | 2026 cost | Annual increase |

|---|---|---|---|

| F | $199 | $227 | 14% |

| G | $159 | $180 | 13% |

| N | $121 | $137 | 13% |

| K | $83 | $87 | 4% |

Average monthly rate for a 65-year-old woman who doesn't smoke

Frequently asked questions

Which Medicare Supplement plan and company is the best?

For most people, the best Medicare Supplement option is Medigap Plan G from AARP/UnitedHealthcare, which costs $177, on average. This plan covers nearly all of the costs that you're responsible for paying with Original Medicare. Plus, AARP/UnitedHealthcare has a good customer service reputation and affordable prices.

How much do Medicare Supplement plans usually cost?

A Medicare Supplement (Medigap) plan costs an average of $180 per month in 2026, across all options. The average cost of Plan G is also $180 per month.

Rates differ based on factors such as age, location and plan letter.

What's the most popular Medicare Supplement plan?

Plan G accounts for nearly 4 in 10 of all Medigap plans sold, making it the most popular choice among all Medigap plan letters. Plan G is popular because it covers nearly all of your costs with Original Medicare.

What's the least expensive Medicare Supplement plan?

A high-deductible Plan G policy costs just $52 per month, on average. However, high-deductible plans only offer protection against major medical costs, since you have to pay $2,950 before your coverage starts.

Methodology

Medicare Supplement policy details are based on info from Medicare.gov and insurance companies. Our expert recommendations are based on plan costs, customer reviews, financial strength ratings and the National Association of Insurance Commissioners’ (NAIC) index of complaints of Medicare Supplement customers for each company's largest subsidiary.

Rate data is for the 2026 plan year. Out-of-pocket maximum limits for Plans K and L and deductibles for Medicare Part B and high-deductible Medicare Plans F and G are for 2025.

Costs are for a 65-year-old woman who doesn't smoke and doesn't qualify for a household discount. Rates are also based on the preferred pricing of initial enrollment when shoppers don't have to answer medical questions. Averages exclude Select plans and plans in Minnesota, Wisconsin and Massachusetts.

Medigap plan enrollment data came from KFF.

About the Author

Former Senior Writer

Talon Abernathy is a former ValuePenguin Senior Writer who specialized in health insurance, Medicare and Medicaid. He also contributed to other insurance verticals including home, renters, auto, motorcycle and flood insurance.

Talon came to ValuePenguin in 2023. Since his arrival, he's helped to expand the site's health insurance-related content offerings. He enjoys helping readers understand the ins and outs of America's all too complicated health insurance landscape.

Before coming to ValuePenguin, Talon worked as a freelance writer. His prior work has touched on a broad range of personal finance-related topics including credit-building strategies, small business incorporation tactics and creative ways to save for retirement.

Insurance tip

In many parts of the country, you can qualify for a free Silver health insurance plan if you meet certain income requirements. Government subsidies in the form of premium tax credits and cost-sharing reductions may mean you'll pay nothing for coverage.

Expertise

- Health insurance

- Medicare and Medicaid

- Flood insurance

- Homeowners insurance

- Renters insurance

- Auto and motorcycle insurance

Referenced by

- The Miami Herald

- Money.com

- MSN

- Nasdaq

- The Sacramento Bee

- Yahoo! Finance

Education

- BA, University of Washington

- Certificate in Copyediting, UC San Diego

Credentials

- Licensed Life & Disability Insurance Agent

- Licensed Property & Casualty Insurance Agent

Editorial Note: We are committed to providing accurate content that helps you make informed financial decisions. Our partners have not endorsed or commissioned this content.