Best Cheap Home Insurance Companies in North Carolina (2026)

State Farm is the cheapest home insurance company in North Carolina, at an average of $803 per year. | ||

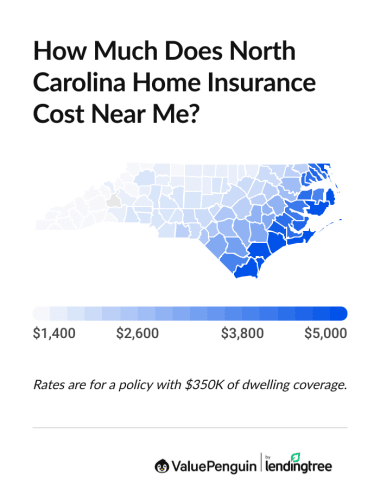

Home insurance in North Carolina costs an average of $2,566/yr, or 7% more than the national average. | ||

Homes along the North Carolina coast tend to pay the most for home insurance, with rates nearly five times the state average. |

State Farm is the cheapest home insurance company in North Carolina, at $803 per year. | ||

Home insurance in North Carolina costs an average of $2,566/yr. But cities near the coast may see rates nearly five times that amount. |

Find Cheap Home Insurance Quotes in North Carolina

What is the best cheap home insurance in North Carolina?

What are the cheapest options for homeowners insurance in North Carolina?

The cheapest North Carolina home insurance company is State Farm, with an average rate of $803 per year.

Find Cheap Home Insurance Quotes in North Carolina

- State Farm is the cheapest option for NC home insurance, no matter how much coverage you need. It's about two-thirds cheaper than the state average, whether you have coverage of only a few hundred thousand dollars, or a very expensive home.

- NC Farm Bureau is the cheapest option for coastal homes. Rates are about half the average in cities like Topsail Beach and Surf City. But State Farm is still the cheapest option in Wilmington.

Cheapest NC home insurance by dwelling coverage

$200,000

$350,000

$500,000

$1 million

Company | Annual rate | ||

|---|---|---|---|

| State Farm | 3.5 out of 5 | $581 | |

| Nationwide | 3.8 out of 5 | $966 | |

| Farm Bureau | 4.3 out of 5 | $1,054 | |

| Allstate | 2.8 out of 5 | $1,607 | |

| Auto-Owners | 3.0 out of 5 | $2,495 | |

| USAA | 3.3 out of 5 | $1,736 | |

Key takeaways

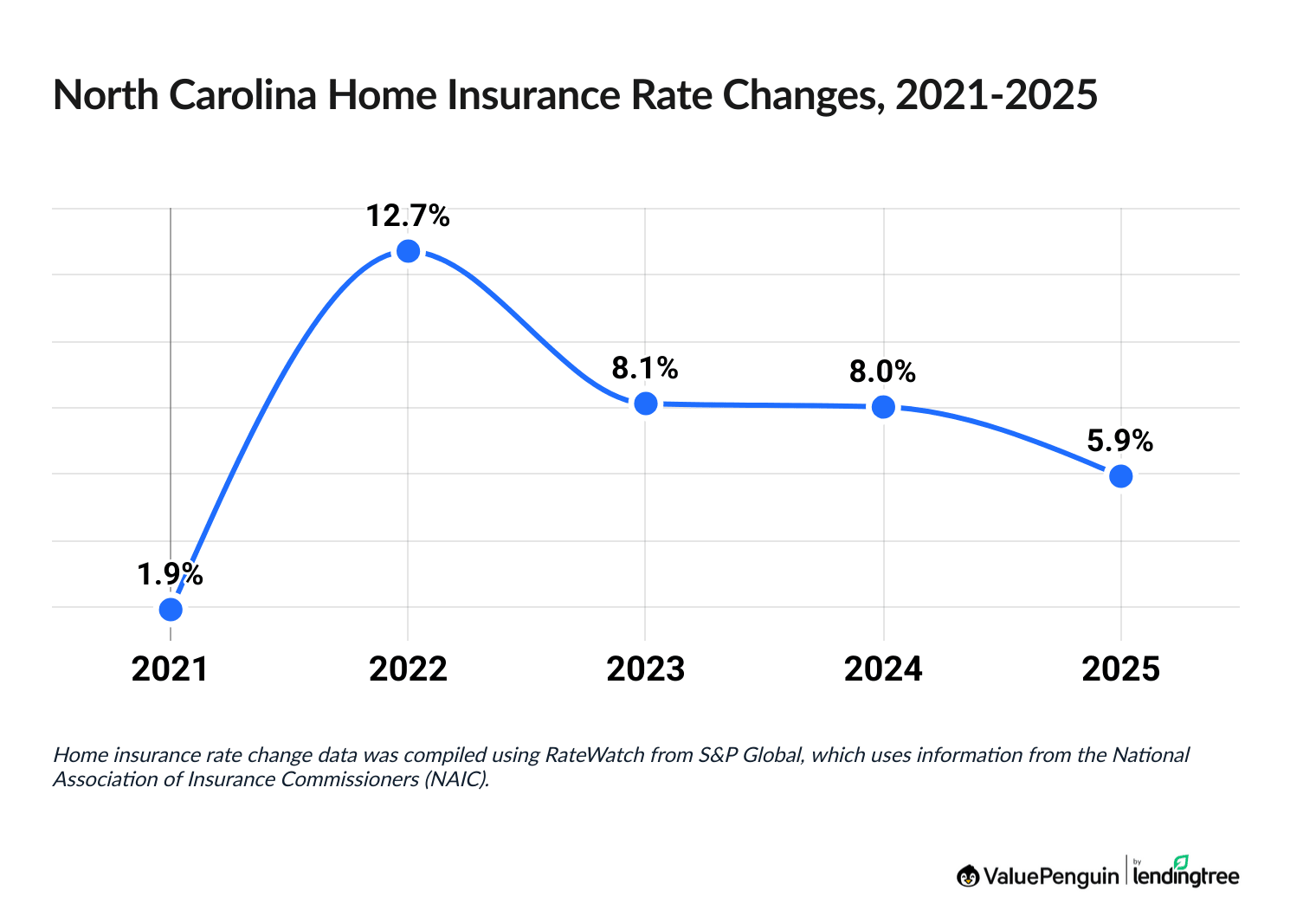

- North Carolina home insurance rates went up 5.9% in 2025, about in line with the increase nationally. Home insurance cost increases in North Carolina may be linked to increasingly frequent coastal storms.

- American Family, Liberty Mutual and Chubb raised rates in North Carolina the least among major insurers, at about 16% over the past five years. Meanwhile, Auto-Owners has more than doubled home insurance prices since 2021.

- North Carolina homeowners should make sure their homes are protected against wind damage, which caused the most damage to homes across the state in 2024. Most home insurance policies include wind coverage, but if your home is in a high-risk area, you may need to buy separate wind insurance.

Best NC home insurance for most people: State Farm

-

Annual cost$803Average rate for a $350,000 home

-

Monthly cost$67Average rate for a $350,000 home

-

Customer complaints Average

Cheapest for homes on the NC coast: Farm Bureau

-

Annual cost$1,784Average rate for a $350,000 home

-

Monthly cost$149Average rate for a $350,000 home

-

Customer complaints Low

Best home insurance in NC for extra coverage: Nationwide

-

Annual cost$2,745Average rate for a $350,000 home

-

Monthly cost$229Average rate for a $350,000 home

-

Customer complaints Low

Best-rated homeowners insurance companies in North Carolina

Farm Bureau and Nationwide have the best customer service in North Carolina.

These companies both receive very few complaints from consumers, meaning you're likely to be satisfied with the service you get at both companies.

Nationwide also did well in J.D. Power's customer claims satisfaction survey.

For those with military ties, USAA is also an excellent option, though it's only available if you or a direct relative has served in the military. It's also much more expensive.

North Carolina home insurance company reviews

Company |

Rating

|

Complaints

|

|---|---|---|

| Farm Bureau | 4.3 out of 5 | Low |

| Nationwide | 3.8 out of 5 | Low |

| State Farm | 3.5 out of 5 | Average |

| USAA | 3.3 out of 5 | Low |

| Auto-Owners | 3.0 out of 5 | Low |

| Allstate | 2.8 out of 5 | Average |

What is the average cost of home insurance in North Carolina?

The average cost of home insurance in North Carolina is $2,566 per year for a policy with $350,000 in dwelling coverage.

Dwelling coverage | Average rate |

|---|---|

| $200,000 | $1,406 |

| $350,000 | $2,566 |

| $500,000 | $3,445 |

| $1 million | $6,460 |

North Carolina's home insurance prices are slightly higher than the nation as a whole, but cheaper than many surrounding states. Home insurance prices in North Carolina are 17% cheaper than in South Carolina and 25% cheaper than in Tennessee, but 3% more expensive than in Virginia.

North Carolina home insurance rates by city

The most expensive city for home insurance in North Carolina is Topsail Beach, a barrier island near Wilmington.

In Topsail Beach, home insurance costs a staggering $12,451 per year, on average. It's the fourth-most expensive city in the United States for home insurance.

Homeowners insurance is generally much more expensive for homes located on the NC coast, including on the Outer Banks.

The cheapest city in the state for home insurance is Burnsville, a mountain town near the Tennessee border, where the average rate is $1,442. In Raleigh, the cost of home insurance is about $2,013 per year.

Cost of North Carolina home insurance by city

City | Average rate | Cheapest company | Cheapest rate |

|---|---|---|---|

| Aberdeen | $2,138 | State Farm | $362 |

| Advance | $1,711 | State Farm | $294 |

| Ahoskie | $2,441 | State Farm | $526 |

| Alamance | $1,953 | Farm Bureau | $1,298 |

| Albemarle | $1,822 | State Farm | $288 |

| Albertson | $3,196 | State Farm | $886 |

| Alexander | $1,482 | State Farm | $236 |

| Alexis | $2,071 | Farm Bureau | $1,328 |

| Alliance | $4,519 | State Farm | $1,464 |

| Almond | $1,577 | State Farm | $849 |

| Altamahaw | $1,761 | State Farm | $283 |

| Andrews | $1,512 | State Farm | $257 |

| Angier | $2,318 | State Farm | $491 |

| Ansonville | $2,235 | State Farm | $400 |

| Apex | $1,987 | State Farm | $379 |

| Arapahoe | $4,532 | State Farm | $1,544 |

| Ararat | $1,647 | State Farm | $292 |

| Archdale | $1,876 | State Farm | $321 |

| Archer Lodge | $2,235 | State Farm | $466 |

| Arden | $1,490 | State Farm | $242 |

| Ash | $5,316 | State Farm | $1,279 |

| Asheboro | $1,874 | State Farm | $310 |

| Asheville | $1,496 | State Farm | $325 |

| Atkinson | $5,616 | State Farm | $1,273 |

| Atlantic | $8,946 | Farm Bureau | $5,560 |

| Atlantic Beach | $11,991 | Farm Bureau | $6,645 |

| Aulander | $2,506 | State Farm | $602 |

| Aurora | $4,177 | State Farm | $1,082 |

| Autryville | $2,749 | State Farm | $732 |

| Avery Creek | $1,481 | State Farm | $231 |

| Avon | $8,287 | Farm Bureau | $5,151 |

| Ayden | $2,826 | State Farm | $691 |

| Aydlett | $4,952 | State Farm | $1,453 |

| Badin | $1,824 | State Farm | $300 |

| Bahama | $1,897 | State Farm | $366 |

| Bailey | $2,130 | State Farm | $450 |

| Bakersville | $1,647 | State Farm | $270 |

| Bald Head Island | $12,131 | Farm Bureau | $6,645 |

| Balfour | $1,505 | State Farm | $244 |

| Balsam | $1,705 | Farm Bureau | $1,126 |

| Balsam Grove | $1,716 | Farm Bureau | $1,089 |

| Banner Elk | $1,491 | State Farm | $273 |

| Barco | $4,952 | State Farm | $1,455 |

| Barium Springs | $1,996 | Farm Bureau | $1,338 |

| Barker Heights | $1,505 | State Farm | $244 |

| Barnardsville | $1,480 | State Farm | $227 |

| Barnesville | $3,172 | State Farm | $1,435 |

| Bat Cave | $1,703 | Farm Bureau | $1,126 |

| Bath | $4,174 | State Farm | $1,061 |

| Battleboro | $2,207 | State Farm | $462 |

| Bayboro | $4,526 | State Farm | $1,506 |

| Bayshore | $8,147 | State Farm | $3,186 |

Rates are for a policy with $350,000 of dwelling coverage.

What are the most common disasters in North Carolina?

Hurricanes are the biggest worry when it comes to your homeowners insurance in North Carolina. Each year, homes in the Tar Heel State suffer millions of dollars in damage from high winds and flooding. However, lightning strikes also cause major losses to North Carolina homeowners.

Hurricanes and flood insurance in North Carolina

Severe storms and hurricanes are regular occurrences in North Carolina, with an average of about one severe storm per year and a tropical cyclone about every two years. Because hurricanes and floods can be devastating one year and not the next, the best plan is to have active insurance coverage at all times.

Does NC home insurance cover wind damage?

Wind damage from hurricanes and storms is almost always covered as part of your standard homeowners insurance. This includes things like shingles falling off the roof and trees being uprooted.

However, you should always confirm this by reading your coverage details. If you live in an area that companies see as high risk, they may exclude wind damage from your regular policy and require you to buy it as an extra coverage. Wind damage is especially common in Surry and Wake counties, with more than 30 serious wind-related events in 2025 in each county.

Does NC home insurance cover flooding?

Flood damage is almost never covered by standard home insurance. Floods can be extremely expensive for insurers when they occur, damaging thousands of insured properties at the same time. Flooding was the single most expensive type of disaster in North Carolina in 2025, causing more than $40 million in damage statewide.

If you're in a high-risk flood zone, you should consider buying a separate flood insurance policy through the government-sponsored National Flood Insurance Program (NFIP) or a private flood insurer.

Lightning strikes in North Carolina

Lightning strikes on private property are also responsible for thousands of claims in North Carolina every year.

On average, insurance claims involving lightning in North Carolina average just over $13,818 per incident. The most serious incidents involve fires started by a lightning strike, while the most common are usually ground surges that overload electronics and appliances plugged into the home.

Homeowners insurance covers most kinds of damage that lightning can inflict on your property. However, the amount you actually get from insurance for lightning-related losses depends on your ability to prove the cause of damage. This can be easier for fires or stricken trees than for ground surges.

Tips to lower your North Carolina home insurance rates

The three best ways to lower what you pay for home insurance in North Carolina are to compare quotes, change your coverage and look for discounts.

Getting quotes from companies is the best way to lower what you pay for home insurance coverage.

The difference between the cheapest and most expensive home insurance companies is $3,600 per year in North Carolina. Every company changes its prices on a yearly basis, so if you're not shopping around every year or two, you may be overpaying for coverage.

Almost every company will offer a number of discounts that will lower your home insurance rates.

One of the best ways to save money is by bundling home insurance with auto or motorcycle insurance. Other discounts are available for things like repairing your roof with stronger materials or putting in a home security system.

A riskier way to lower home insurance rates is to reduce your coverage limits or raise your deductible.

Lowering your coverage and shedding extra protections will save you money. But it also means your insurance will pay less if your home is significantly damaged and may not cover anything after some disasters. You should still have enough coverage to pay for rebuilding your home and replacing your belongings if a disaster happens.

When you have a higher deductible, you'll get less from your insurance company when your home is damaged. This also means it won't be worth it to file some claims. One key thing is that you'll want a deductible you can easily afford in an emergency.

North Carolina home insurance trends

Home insurance prices are up 53.5% in North Carolina since 2021.

Costs spiked as the COVID-19 pandemic ended in 2022, with a 12.7% increase. But increases have slowed in the past few years, with a relatively small increase of 5.9% in 2025.

Home insurance cost increases can be driven by major storm events like Hurricane Helene in September 2024, as well as higher costs due to inflation

Among NC home insurance companies, Liberty Mutual, American Family and Chubb had the smallest rate increases, at around 16% since 2021. But Auto-Owners has more than doubled its prices over that time.

Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

Frequently asked questions

How much is the average home insurance in NC?

The average price of home insurance in NC is $2,566 per year for $350,000 in coverage. That makes it the 22nd-most expensive state of coverage.

What is the cheapest home insurance in NC?

State Farm has the cheapest home insurance in North Carolina. The company's average rate is $803 per year for $350,000 in coverage.

Is homeowners insurance required in North Carolina?

Homeowners insurance is not required by law in North Carolina. But you will need coverage to get some types of mortgages. This is because your lender will own part of the house and wants to make sure it doesn't lose value before your loan is paid off.

Does Progressive do home insurance in North Carolina?

Progressive sells home insurance in North Carolina, but it's underwritten by a partner company, Homesite. Policies from Homesite tend to be expensive, and the company has a poor customer service reputation.

Methodology

To find the best homeowners insurance in North Carolina, ValuePenguin gathered quotes in every ZIP code in the state from the largest homeowners insurance companies. Rates are for a 2,152 square foot home built 43 years ago, based on the average home age and size in North Carolina.

ValuePenguin sourced quotes for properties at four levels of dwelling coverage to understand the cost of coverage for a variety of homes.

- Dwelling coverage: $200,000, $350,000, $500,000 or $1 million

- Personal liability: $100,000

- Medical payments: $1,000

- Deductible: $1,000

ValuePenguin's analysis used insurance rate data from Quadrant Information Services. These rates were publicly sourced from insurer filings and should be used for comparative purposes only — your own quotes will be different.

Each company's customer service was ranked by comparing the National Association of Insurance Commissioners (NAIC) complaint index, J.D. Power's home insurance customer satisfaction and claims satisfaction rankings and ValuePenguin editor's ratings.

Disaster data was collected from the LexisNexis home trends report and the National Oceanic and Atmospheric Administration's National Center for Environmental Information database.

About the Author

Former Lead Writer

Matt Timmons is a former Lead Writer on the insurance team at ValuePenguin, where he writes in-depth and timely pieces helping find the right coverage for them.

He covered insurance at ValuePenguin between 2018 and 2026, specializing in auto and home insurance, as well as life insurance. He paid special attention to the EV insurance market, where prices are much higher than for gas cars.

Before he started writing about personal finance, Matt wrote about professional skills and online tools at an e-learning company.

How insurance helped Matt

During freshman orientation in college, Matt's iPod was stolen off his table while he was eating lunch. Luckily, he'd bought a college insurance plan the day before and he had money to buy a replacement before classes started.

Expertise

- Auto insurance

- Home insurance

- Insurance rate analysis

- Life insurance

Referenced by

- CNBC

- Miami Herald

- Yahoo! Finance

Education

- BA, Wesleyan University

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.