The Best and Cheapest Home Insurance Companies in New York for 2026

NYCM has the cheapest home insurance in New York, at $588 per year. | ||

Home insurance in New York costs 42% less than the national average, at $1,387 per year. | ||

Coastal Long Island has some of New York’s highest home insurance rates, while people living upstate tend to pay less for homeowners insurance. |

NYCM has the cheapest home insurance in New York, at $588/yr. | ||

Home insurance costs an average of $1,387/yr in New York, but homes in the Hamptons tend to have higher rates. |

Find Cheap Home Insurance Quotes in New York

Best cheap home insurance in New York

The cheapest homeowners insurance companies in New York

NYCM has the best home insurance rates in New York, regardless of how much coverage you need.

Find Cheap Home Insurance Quotes in New York

-

A policy from NYCM costs an average of $588 per year for $350,000 of

dwelling coverage.

That makes it 58% cheaper than the state average.

NYCM also has the lowest rates if you have a more expensive house. An NYCM home policy for $1 million of coverage costs $1,631 per year, 58% below the state average.

-

If you have complicated home insurance needs or want the stability of buying coverage from a major national company, consider Nationwide. Its coverage options and service are both excellent, and its prices are cheaper than average.

Cheap annual home insurance quotes in New York

$200,000

$350,000

$500,000

$1 million

Company | Annual rate | ||

|---|---|---|---|

| NYCM | 3.8 out of 5 | $379 | |

| Preferred Mutual | 3.8 out of 5 | $547 |

| Farmers | 4.0 out of 5 | $596 | |

| Sterling | 3.8 out of 5 | $629 |

| State Farm | 3.0 out of 5 | $678 | |

Key takeaways

- New York home insurance rates went up around 4.3% in 2025, less than the jump nationally of 5.6%. New York home insurance prices have had relatively small increases over the last five years. Rates have increased about half as fast in the Empire State as in the country overall. This may be because major contributors to increasing home insurance costs, like severe hurricanes and wildfires, have not impacted New York much.

- USAA, Travelers and State Farm raised rates the least among major New York insurance companies during the past five years. USAA has only raised NY rates once since 2021, by only 6.7%. Travelers customers pay 14.3% more now than in 2021, and State Farm customers pay 18.0% more.

- New York homeowners may be able to save on home insurance by looking for a local insurer. The three cheapest companies overall, NYCM Insurance, Preferred Mutual and Sterling Insurance, are all smaller regional companies with lower rates.

Best for most people: NYCM

-

Annual cost$588Average rate for a $350,000 home

-

Monthly cost$49Average rate for a $350,000 home

-

Customer complaints Average

Best coverage options: Nationwide

-

Annual cost$1,270Average rate for a $350,000 home

-

Monthly cost$106Average rate for a $350,000 home

-

Customer complaints Low

Best for high-value homes: Chubb

-

Annual cost$5,910Average rate for a $1 million home

-

Monthly cost$493Average rate for a $1 million home

-

Customer complaints Low

What are the top-rated homeowners insurance companies in New York?

Nationwide and Chubb have the best-rated customer service for New York homeowners.

These two companies fared well in J.D. Power's latest customer satisfaction surveys, and they have very few complaints from the NAIC. Chubb has the best rating overall, but it's only available to people with very expensive homes.

Company |

Rating

|

Complaints

|

|---|---|---|

| Nationwide | 4.5 out of 5 | Low |

| Farmers | 4.0 out of 5 | Low |

| Kingstone | 4.0 out of 5 | Low |

| NYCM | 3.8 out of 5 | Average |

| Preferred Mutual | 3.8 out of 5 | Average |

How much does home insurance cost in New York?

Homeowners insurance in New York costs 42% less than the national average.

The Northeast has cheaper homeowners rates compared to the U.S. as a whole. That's likely because this region gets few natural disasters.

You'll pay about the same for homeowners insurance in New York as you would in neighboring states like New Jersey.

Dwelling coverage | Average rate |

|---|---|

| $200,000 | $891 |

| $350,000 | $1,387 |

| $500,000 | $1,943 |

| $1 million | $3,926 |

Cost of homeowners insurance in New York by city

The most expensive city for home insurance in New York is Napeague, on the South Fork of Long Island.

The average price in Napeague is $3,257 per year for $350,000 of dwelling coverage. That's about 135% more than the state average.

Home insurance in New York tends to be most expensive in outer Long Island, as that area is more susceptible to coastal storms. Homes there may also be harder to repair or rebuild, given the area's relatively isolated location.

Who has the cheapest home insurance in NYC?

NYCM has the lowest home insurance rates in NYC, at $1,012 per year for $500,000 of dwelling coverage, or 67% cheaper than average.

Staten Island has the cheapest home insurance in NYC, while Manhattan has the most expensive.

City | Average rate | Cheapest company | Cheapest rate |

|---|---|---|---|

| NYC | $3,061 | NYCM | $1,012 |

| Bronx | $2,974 | NYCM | $901 |

| Brooklyn | $2,954 | NYCM | $754 |

| Manhattan | $3,477 | NYCM | $1,318 |

| Queens | $2,648 | NYCM | $881 |

| Staten Island | $2,307 | NYCM | $510 |

Rates are for a policy with $500,000 of dwelling coverage.

Standard home insurance policies in New York only apply to single-family homes, whether they're freestanding or share a wall with their neighbor. If you live in a condo or co-op apartment building, you'll need a different kind of home insurance.

Annual home insurance rates in NY by city

City | Average rate | Cheapest company | Cheapest rate |

|---|---|---|---|

| Accord | $1,242 | Preferred Mutual | $588 |

| Acra | $1,227 | NYCM | $618 |

| Adams | $1,186 | Preferred Mutual | $627 |

| Adams Basin | $1,038 | NYCM | $520 |

| Adams Center | $1,183 | Preferred Mutual | $627 |

Rates are for a policy with $350,000 of dwelling coverage.

What natural disasters should I watch out for in New York?

New York's most common natural disasters are heavy rainstorms, as well as coastal storms like nor'easters and occasional hurricanes.

Home insurance generally covers damage from wind and hail, but if your home is at risk of flooding, you'll likely need a separate policy.

Is wind damage covered by home insurance in New York?

Homeowners insurance almost always covers wind damage.

As a coastal state on the Eastern Seaboard, New York is vulnerable to nor'easters, tropical storms and other large storms that can cause damage to your home. This is especially true if you live on Long Island, in New York City or in the Lower Hudson Valley.

Are snow and hail damage covered by home insurance in New York?

If your roof or other parts of your home are damaged by hail or the weight of snow, you'll usually be covered by home insurance.

Hail damage was the single biggest cause of property damage from natural disasters in New York in 2025, accounting for $20 million of damage to roofs, cars and other property, according to the National Oceanic and Atmospheric Administration (NOAA).

Snow was another serious cause of damage, causing more than $2 million in damage in 2025.

However, you may not be covered for all types of damage. Home insurance policies won't cover hail or snow damage to your car, and may exclude damage to landscaping or trees.

Is flooding covered by home insurance in New York?

Your home insurance policy won't cover flood damage. If you live in a coastal zone or an area with a high risk of flooding, you'll need to buy a separate flood insurance policy.

This is particularly important for people living in low-lying areas, near major rivers or along the coast. The National Flood Insurance Program has paid out more than $300 million in claims in New York between 2015 and 2025, with more than half of the total claim value paid out to people in Westchester and Long Island.

Tips for buying the best home insurance in New York

To save money on your New York home insurance policy, it's a good idea to shop around. If you live in New York City, Buffalo, Rochester or another densely populated part of the state, you should have access to multiple options including large national companies like State Farm and Farmers as well as regional companies like NYCM. | |

New York home insurance trends

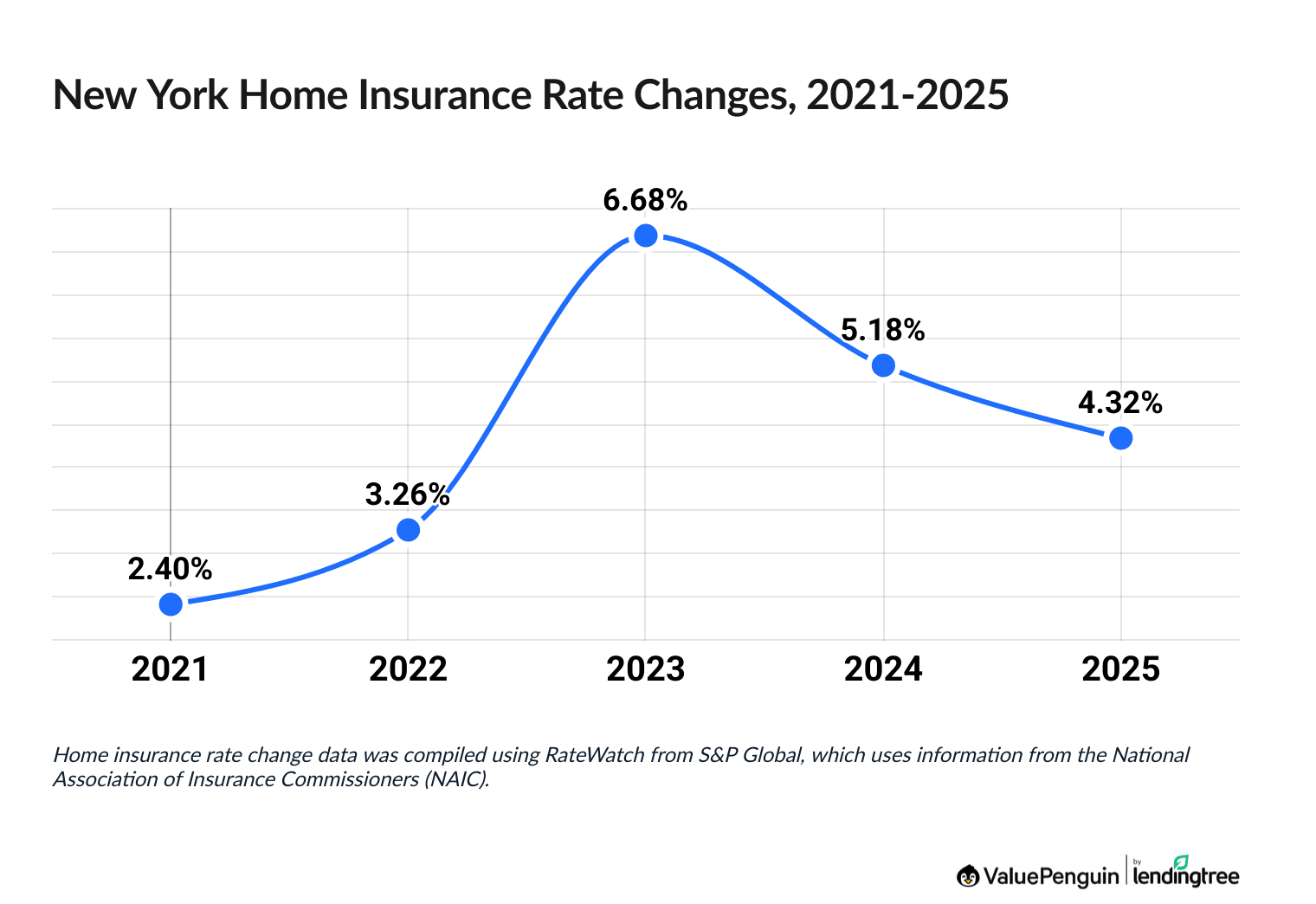

Home insurance prices are up 24.4% in New York over the last five years.

New York homeowners have seen mild increases in their home insurance prices in recent years, with an average increase of 5.2% in 2024, followed by a 4.3% increase in 2025.

New York's rate increases have been lower than the country overall. Nationally, home insurance prices have jumped 47.9% since 2021, and 5.6% in 2025.

Home insurance rate hikes in New York, 2021-2025

Year | Rate increase |

|---|---|

| 2021 | 2.4% |

| 2022 | 3.3% |

| 2023 | 6.7% |

| 2024 | 5.2% |

| 2025 | 4.3% |

Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

Heritage Insurance saw the biggest increase among larger NY companies, with a jump of 68.3% over the last five years.

USAA, Travelers and State Farm customers experienced the smallest rate increases, at just 6.7%, 14.3% and 18.0%, respectively.

Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

Frequently asked questions

How much is homeowners insurance in New York?

The average cost of home insurance in New York is $1,387 per year, or $116 per month for $350,000 of dwelling coverage.

Who has the cheapest homeowners insurance in New York?

NYCM, New York Central Mutual Insurance Co., offers the best home insurance rates in the state. A typical policy costs $588 per year, which is 58% cheaper than the statewide average.

Methodology

To find the best homeowners insurance in New York, ValuePenguin gathered quotes in every ZIP code in the state from the largest homeowners insurance companies. Rates are for a 1,490 square foot home built 52 years ago, based on the average home age and size in New York.

ValuePenguin sourced quotes for properties at four levels of dwelling coverage to understand the cost of coverage for a variety of homes.

- Dwelling coverage: $200,000, $350,000, $500,000 or $1 million

- Personal liability: $100,000

- Medical payments: $1,000

- Deductible: $1,000

ValuePenguin's analysis used insurance rate data from Quadrant Information Services. These rates were publicly sourced from insurer filings and should be used for comparative purposes only — your own quotes will be different.

Each company's customer service was ranked by comparing the National Association of Insurance Commissioners (NAIC) complaint index, J.D. Power's home insurance customer satisfaction and claims satisfaction rankings, and ValuePenguin editor's ratings.

Cost information for disasters was gathered from the National Oceanic and Atmospheric Administration (NOAA) and the National Flood Insurance Program (NFIP).

About the Author

Lead Writer

Matt Timmons is a Lead Writer on the insurance team at ValuePenguin, where he writes in-depth and timely pieces helping find the right coverage for them.

He's covered insurance at ValuePenguin since 2018, specializing in auto and home insurance, as well as life insurance. He's paid special attention to the EV insurance market, where prices are much higher than for gas cars.

Before he started writing about personal finance, Matt wrote about professional skills and online tools at an e-learning company.

How insurance helped Matt

During freshman orientation in college, Matt's iPod was stolen off his table while he was eating lunch. Luckily, he'd bought a college insurance plan the day before and he had money to buy a replacement before classes started.

Expertise

- Auto insurance

- Home insurance

- Insurance rate analysis

- Life insurance

Referenced by

- CNBC

- Miami Herald

- Yahoo! Finance

Education

- BA, Wesleyan University

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.