Best and Cheapest Home Insurance in Massachusetts (2026)

Norfolk & Dedham usually has the cheapest home insurance rates in Massachusetts, at $521/yr, on average. | ||

Home insurance in Massachusetts costs an average of $1,635/yr, which is 32% less than the national average. | ||

Cape Cod and the Islands tend to have much more expensive home insurance rates. People living in Chilmark, the most expensive city in the state, pay an average of $3,400/yr. |

Norfolk & Dedham usually has the cheapest home insurance rates in Massachusetts, at $521/yr, on average. | ||

Home insurance in Massachusetts costs an average of $1,635/yr. But rates tend to be much more expensive around Cape Cod and the Islands. |

Find Cheap Home Insurance Quotes in Massachusetts

Who has the best cheap home insurance in Massachusetts?

Who has the cheapest home insurance in MA?

Norfolk & Dedham is the cheapest home insurance company in Massachusetts.

Find Cheap Home Insurance Quotes in Massachusetts

Norfolk & Dedham's home insurance rates are typically 67% to 69% cheaper than the Massachusetts state average, depending on how much coverage you need.

For example, a Norfolk & Dedham policy with $350,000 of dwelling coverage costs $521 per month, on average. That's one-third of the average price statewide. It's also $340 per year less than the second-cheapest company, Quincy Mutual.

Homeowners insurance rates in Massachusetts by dwelling coverage amount

Key takeaways

-

Home insurance rates in Massachusetts went up by less than 3% in 2025, around half the average increase nationwide. And over the past five years, rates have gone up 20 percentage points less in Massachusetts than they have nationally.

That might be partially because Massachusetts hasn't had many major weather events recently, averaging fewer than three billion-dollar weather events per year during the past five years.

- Homeowners in Massachusetts need to make sure they're protected against flood damage. Water causes the most damage to homes across the state, whether it's from burst pipes after a hard freeze or storm surge during a tropical storm.

Best homeowners insurance in Massachusetts for most people: Norfolk & Dedham

-

Annual cost$521Average rate for a $350,000 home

-

Monthly cost$43Average rate for a $350,000 home

-

Customer complaints Average

Cheapest homeowners insurance for 100-year-old homes in MA

Company | Annual rate | |

|---|---|---|

| Norfolk & Dedham | $567 |

| Quincy Mutual | $861 |

| Farmers | $1,252 | |

| Vermont Mutual | $1,364 |

| Narragansett Bay | $1,404 |

Rates are for a home built in 1925 with $350,000 of dwelling coverage.

Best for bundling home and auto insurance in Massachusetts: Arbella

-

Annual cost$1,342Average rate for a $350,000 home

-

Monthly cost$112Average rate for a $350,000 home

-

Customer complaints Low

Best insurance in MA for luxury homes: Chubb

-

Cost for a $500,000 home$3,011/yrAverage rate for a $500,000 home

-

Cost for a $1 million home$5,285/yrAverage rate for a $1 million home

-

Customer complaints Low

Best-rated Massachusetts home insurance companies

Narragansett Bay is the top-rated home insurance company in Massachusetts.

That's because Narragansett Bay offers the best combination of great customer service, affordable rates, useful coverage add-ons and helpful discounts in Massachusetts.

However, Massachusetts has lots of well-rated companies with great customer service and low home insurance rates. You should compare quotes from a handful of our top-rated companies to find the best policy for you.

Best home insurance in Massachusetts

Company |

Rating

|

Complaints

|

|---|---|---|

| Narragansett Bay | 5.0 out of 5 | Low |

| Arbella | 4.5 out of 5 | Low |

| USAA | 4.5 out of 5 | Low |

| Andover | 4.0 out of 5 | Low |

| Farmers | 4.0 out of 5 | Low |

Worst home insurance companies in Massachusetts

Mapfre and Universal have some of the worst home insurance in Massachusetts. Both companies get around twice as many customer complaints as average.

This means that you could face more frustrations if you file a claim or if you call customer service about your policy. Additionally, Mapfre and Universal don't have cheap rates, so they won't help you save money.

How much does home insurance in Massachusetts cost?

The average cost of homeowners insurance in Massachusetts is $1,635 per year for $350,000 in dwelling coverage.

Dwelling coverage | Average rate |

|---|---|

| $200,000 | $1,068 |

| $350,000 | $1,635 |

| $500,000 | $2,270 |

| $1 million | $4,119 |

Home insurance in Massachusetts is 32% cheaper than the national average, which is $2,395 per year for a $350,000 home.

However, other states in New England have even cheaper rates. Home insurance in New Hampshire, Maine and Vermont costs about $900 to $1,300 per year for a $350,000 home.

How much does homeowners insurance in Boston cost?

Home insurance in Boston costs an average of $1,893 per year.

That's 16% more expensive than the Massachusetts state average. It's also more expensive than many towns in the Boston area, including Cambridge, Quincy and Lynn.

Average cost of Boston home insurance

City | Annual rate |

|---|---|

| Boston | $1,893 |

| Newton | $1,413 |

| Malden | $1,438 |

| Medford | $1,445 |

| Cambridge | $1,453 |

Rates are for a policy with $350,000 of dwelling coverage.

Where is home insurance cheap in Massachusetts?

Massachusetts home insurance is cheapest in the Berkshires and Pioneer Valley and most expensive in Cape Cod.

Lenox Dale, a small village in the Berkshires, is the cheapest city in Massachusetts for home insurance, with average rates of $1,219 per year.

Chilmark in Martha's Vineyard is the most expensive city in Massachusetts for home insurance, at an average of $3,400 per year. That's more than double the state average. The high rates are likely because it's an expensive area, the coastal storms coming off the Atlantic can cause weather damage, and repair materials need to be brought to the island by boat.

Norfolk & Dedham has the cheapest home insurance in the vast majority of cities and towns across Massachusetts. Narragansett Bay has the lowest rates in 12 towns around Martha's Vineyard and the Islands.

Find Cheap Home Insurance Quotes in Massachusetts

Massachusetts home insurance rates by city

City | Average rate | Cheapest company | Cheapest rate |

|---|---|---|---|

| Abington | $1,720 | Norfolk & Dedham | $512 |

| Accord | $1,815 | Norfolk & Dedham | $518 |

| Acton | $1,426 | Norfolk & Dedham | $485 |

| Acushnet | $1,960 | Norfolk & Dedham | $516 |

| Acushnet Center | $1,946 | Norfolk & Dedham | $483 |

Rates are for a policy with $350,000 of dwelling coverage.

What home insurance coverage is important in Massachusetts?

In Massachusetts, it's important to protect your home against floodwater, cold weather and theft.

Flooding causes more damage to Massachusetts homes than any other type of damage.

Home insurance covers some, but not all, types of flooding. For example, your home insurance likely covers water damage caused by a leaky roof or a burst pipe.

However, home insurance doesn't typically cover flooding from heavy rains or storm surge. Massachusetts homeowners should consider buying a separate flood insurance policy for protection from these types of water damage.

Essex County, which includes Gloucester, Rockport and Salem, had the most flood-related damage during this time period, at nearly $7 million.

Cold weather damage, such as frozen pipes and ice dams, can cause widespread and expensive home repairs in Massachusetts.

Home insurance usually protects you from the cost of cold-weather damage, including frozen pipes and ice damage to your roof. That's especially important in Massachusetts, where non-weather-related flooding and freezing-related damage are responsible for about half of all home insurance claims.

Older homes are usually more at risk for cold-weather damage because poor insulation can cause water pipes to freeze, or melting snow can cause ice damage to your roof.

But all homes in MA could potentially have claims related to cold weather. For example, a power outage can mean pipes can freeze even in new homes. Or someone could be injured on icy steps.

Your home insurance company won't pay for damage they believe could have been prevented by regular home maintenance. So it's important to check your attic for ice dams and drip your faucet during freezing temperatures to help prevent damage.

If you live in a part of Massachusetts with high crime, you're more likely to have your home vandalized or something stolen.

Your home insurance policy will cover your costs for theft or vandalism. If something is stolen, the claim would be under the personal property part of your home insurance policy. This is especially useful in cities with high rates of property crime including Springfield, Cambridge and Boston.

Home insurance coverage also includes vandalism. So if someone breaks your mailbox or spray-paints your fence, your insurance should pay for the repairs.

How to save money on Massachusetts home insurance

The best way to save on home insurance is to compare home insurance quotes from multiple companies.

In Massachusetts, there's a difference of $2,264 per year between the most and least expensive companies. By shopping around, you'll find out which company offers you the best deal for your home.

Even cheap home insurance companies are not cheap for everyone. That's because each company uses its own calculations in how it determines rates. Factors like your credit rating, the age of your home and where you live could be used in the calculations.

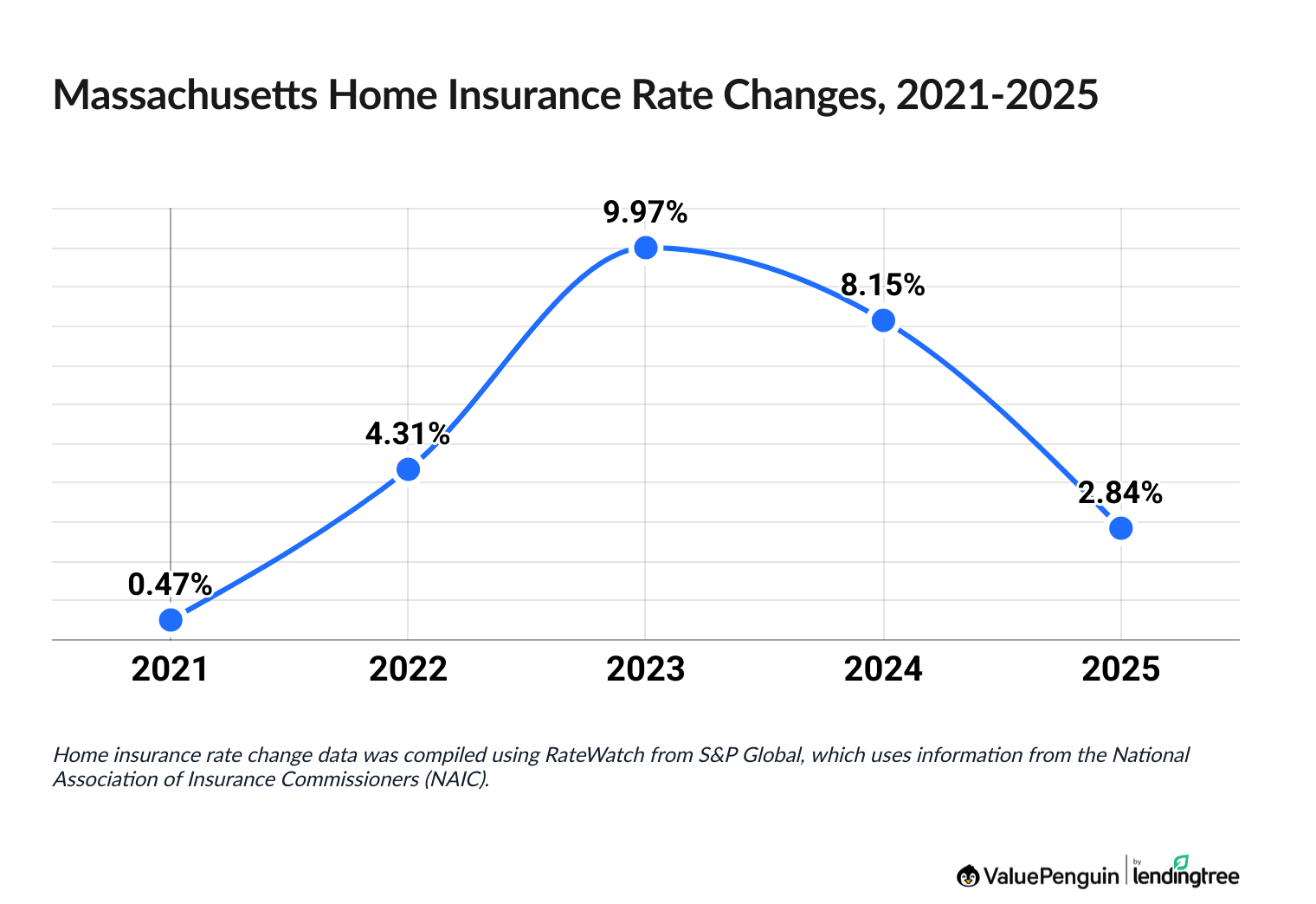

Trends in Massachusetts home insurance costs

Home insurance prices have increased by around 28% in Massachusetts over the last five years.

That's significantly less than the average increase nationally, which was nearly 48% over that time period.

Massachusetts homeowners saw a spike in their rates in 2023, when insurance companies raised rates by nearly 10% statewide. But rate increases slowed significantly in 2025, with an average increase of under 3%.

Home insurance rate hikes in Massachusetts, 2021-2025

Year | Rate increase |

|---|---|

| 2021 | 0.47% |

| 2022 | 4.31% |

| 2023 | 9.97% |

| 2024 | 8.15% |

| 2025 | 2.84% |

Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

USAA had the lowest rate hike in Massachusetts over the last five years, at just 4.8%. Plymouth Rock customers saw the biggest increase in their home insurance rates, at over 59%, on average.

Frequently asked questions

Why is home insurance so high in Massachusetts?

Massachusetts is actually the 14th-cheapest state for home insurance in the U.S. With an average rate of $1,635 per year, Massachusetts homeowners pay 32% less than the national average.

However, your homeowners insurance may feel very expensive if you're insured with a company that has raised rates significantly in recent years. For example, Auto-Owners, Plymouth Rock and Mapfre have all raised rates by over 43% over the last five years.

What's the best home insurance company in Boston?

Norfolk and Dedham is the best home insurance company in Boston. It has extremely cheap rates at $527 per year, which is less than one-third of the average price in Boston. It also has affordable rates for older homes and very few customer complaints.

What's the best home insurance company in Cape Cod?

The best home insurance companies in Cape Cod are Norfolk and Dedham and Narragansett Bay. While both companies have very affordable rates, Narragansett Bay is a better choice for most people because it offers flood insurance as an add-on to your home insurance policy. That means you don't have to buy a separate flood insurance policy, which could make your life much easier if you ever have to file a claim.

Methodology

The average cost of home insurance in Massachusetts is based on quotes from the top companies across every residential ZIP code in the state. Rates are for a 45-year-old married man with no prior insurance claims. Quotes are for a 1,800 square foot home built 51 years ago, based on the average home age and size in Massachusetts.

Quotes include the following coverage limits:

- Dwelling coverage: $200,000, $350,000, $500,000 or $1 million

- Personal liability: $100,000

- Medical payments: $1,000

- Deductible: $1,000

ValuePenguin used insurance rate data from Quadrant Information Services. Quadrant's rates were publicly sourced from insurer filings and should only be used for comparative purposes.

Home insurance ratings are based on complaint data from the National Association of Insurance Commissioners (NAIC), the J.D. Power customer satisfaction survey and ValuePenguin's ratings.

Sources:

About the Author

Senior Writer

Lindsay Bishop is a Senior Writer at ValuePenguin, where she educates readers about home, auto, renters, flood and motorcycle insurance.

Lindsay began her career in the insurance and financial industry in 2010. She was a licensed auto, home, life and health insurance agent and held Series 6 and 63 financial licenses.

After a hiatus from the financial sector, Lindsay returned to the industry as a content writer for ValuePenguin in 2021. She enjoys having the opportunity to help readers make smart decisions about their insurance so they can be prepared for anything life throws their way.

When Lindsay isn't writing about insurance, you can find her spending time with family, enjoying the outdoors on Sunday long runs or riding her Peloton.

How insurance helped Lindsay

As a homeowner for 15 years located in South Carolina, Lindsay has plenty of experience navigating the coastal insurance market and managing the claims process. That includes successfully negotiating a full roof replacement claim.

Expertise

- Home insurance

- Car insurance

- Flood insurance

- Renters insurance

- Motorcycle insurance

Referenced by

- CNBC

- Yahoo Finance

- Miami Herald

Education

- BS/BA Economics, University of Nevada Las Vegas

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.