The Best Cheap Home Insurance Companies in Utah (2026)

State Farm has the cheapest home insurance in Utah. It charges $787 per year on average for $350,000 of dwelling coverage.

Find Cheap Home Insurance Quotes in Utah

Best cheap home insurance in Utah

Our experts compared cost, coverage and customer service to find the best companies in Utah.

ValuePenguin collected thousands of quotes for top home insurance companies across hundreds of Utah ZIP codes.

Cheapest home insurance quotes in UT

State Farm has the cheapest homeowners insurance quotes in Utah at $787 per year for $350,000 of coverage to repair or rebuild your home, called dwelling coverage. That's 31% less than the Utah state average.

Cheapest homeowners insurance companies in UT

Find Cheap Homeowners Insurance Quotes in Your Area

Mutual of Enumclaw is a good choice if you own a more affordable home. At $545 per year, it has the cheapest rates in Utah for $200,000 of dwelling coverage.

Best cheap home insurance in Utah

$200,000

$350,000

$500,000

$1 million

Company | Annual rate | ||

|---|---|---|---|

| Mutual Of Enumclaw | 4.5 out of 5 | $545 | |

| Farm Bureau | 4.5 out of 5 | $564 | |

| State Farm | 4.5 out of 5 | $613 | |

| Travelers | 3.0 out of 5 | $633 | |

| Farmers | 2.0 out of 5 | $662 | |

Stars in this table represent ratings specific to home insurance.

Natural disasters in Utah

Utah homeowners should protect themselves against common natural disasters like floods, earthquakes and wildfires.

Fortunately, most standard home insurance policies cover wildfires. However, it's always a good idea to double-check your policy because some companies don't offer coverage in high-risk areas.

You need to buy separate coverage for earthquakes and floods.

Best home insurance in Utah for most people: State Farm

-

Cost$787/yrQuote is for $350,000 of dwelling coverage. This analysis used home insurance quotes for hundreds of ZIP codes across UT. Read our methodology.

Best home insurance in Utah for wildfire protection: Mutual of Enumclaw

-

Cost$807/yrQuote is for $350,000 of dwelling coverage. This analysis used home insurance quotes for hundreds of ZIP codes across UT. Read our methodology.

Best home insurance company for customer service in Utah: Farm Bureau

-

Cost$790/yrQuote is for $350,000 of dwelling coverage. This analysis used home insurance quotes for hundreds of ZIP codes across UT. Read our methodology.

Average home insurance cost in Utah

Homeowners insurance costs $1,137 per year in Utah for $350,000 of coverage. That's roughly half the national average of $2,151 per year.

Dwelling coverage | Annual cost |

|---|---|

| $200,000 | $803 |

| $350,000 | $1,137 |

| $500,000 | $1,497 |

| $1,000,000 | $2,607 |

Utah residents pay less for home insurance than in neighboring states. Home insurance in Utah is cheaper than in nearby Nevada and Idaho. You'll pay significantly more for homeowners insurance in Colorado, New Mexico and Arizona .

Utah insurance rates by city

Vernon, a small town West of Salt Lake City, has the most expensive homeowners insurance rates in Utah, at $1,431 per year on average.

Washington, a city in Southwestern Utah near Zion National Park, has the cheapest rates in Utah, at $1,045 per year on average.

Where you live will influence how much you pay for home insurance. Factors like crime, labor and materials costs and how often they experience natural disasters like powerful storms and wildfires can all influence homeowners insurance rates.

City | Annual rate | % from avg |

|---|---|---|

| Alpine | $1,213 | 7% |

| Altamont | $1,155 | 2% |

| Alton | $1,136 | 0% |

| Altonah | $1,165 | 2% |

| American Fork | $1,105 | -3% |

Rates are for a policy with $350,000 of dwelling coverage.

The best homeowners insurance companies in UT

State Farm, Mutual of Enumclaw, Farm Bureau and Auto-Owners have the best-rated homeowners insurance in Utah.

All four companies offer quality coverage and get few complaints.

State Farm, Mutual of Enumclaw and Farm Bureau also have cheap rates, but Auto-Owners has some of the most expensive home insurance quotes in Utah. However, the company balances its high rates with strong customer service.

Company |

Rating

|

Complaints

|

|---|---|---|

| State Farm | 4.5 out of 5 | Average |

| Farm Bureau | 4.5 out of 5 | Low |

| Mutual Of Enumclaw | 4.5 out of 5 | Low |

| Auto-Owners | 4.5 out of 5 | Low |

| American Family | 4.0 out of 5 | Low |

Stars in this table represent ratings specific to home insurance.

Common natural disasters in UT

You may need coverage for earthquakes, wildfires and flooding if you live in Utah.

A standard home insurance policy will cover fire damage. However, insurance companies may drop coverage if your home is in an area with frequent wildfires.

If you can't buy wildfire coverage through a private company, you can get coverage through the government, called a FAIR plan policy. Keep in mind that these plans tend to be expensive.

Flood insurance in Utah

Floods are the most common and destructive natural disaster in Utah.

Mortgage lenders often require that you buy flood insurance if you live in a high-risk area. Even if you own your home outright, you should still consider flood coverage. A single inch of floodwater in your home can cause $25,000 of damage.

The type of floods you should prepare for will depend on where you live in Utah. For example, Southern Utah is at a greater risk of flash floods. Areas closer to the mountains may experience seasonal flooding related to mountain snowmelt.

Earthquake risks in Utah

Utah has had 17 large earthquakes since settlers arrived in 1847.

In addition to earthquakes caused by regular movements of the earth, the eastern and central parts of the state get frequent earthquakes because of coal mining. You can get standalone earthquake coverage if you live in an earthquake-prone part of the state.

Tips for saving money on home insurance in Utah

Comparing quotes can save you more than a thousand dollars per year on your home insurance.

The difference between the most and least expensive home insurance companies in Utah is $1,037 per year for $350,000 of coverage to repair or rebuild your house.

It's important to remember that paying more for home insurance won't necessarily get you better customer service or coverage. For example, State Farm has the cheapest home insurance in Utah and a strong customer service reputation.

Take advantage of home insurance discounts

Most home insurance companies offer multiple discounts. You can lower your monthly rate by taking advantage of common discounts like bundling your home and renters insurance and having a burglar and fire alarm.

It's a good idea to check for discounts when comparing home insurance quotes. The cheapest home insurance for you will depend on which discounts you qualify for.

Raise your home insurance deductible

You can lower your home insurance rate by increasing the amount of money you pay for home repairs before your home insurance starts working, called a deductible. You should never raise your deductible beyond what you can easily cover from your savings.

Surging Utah home insurance costs

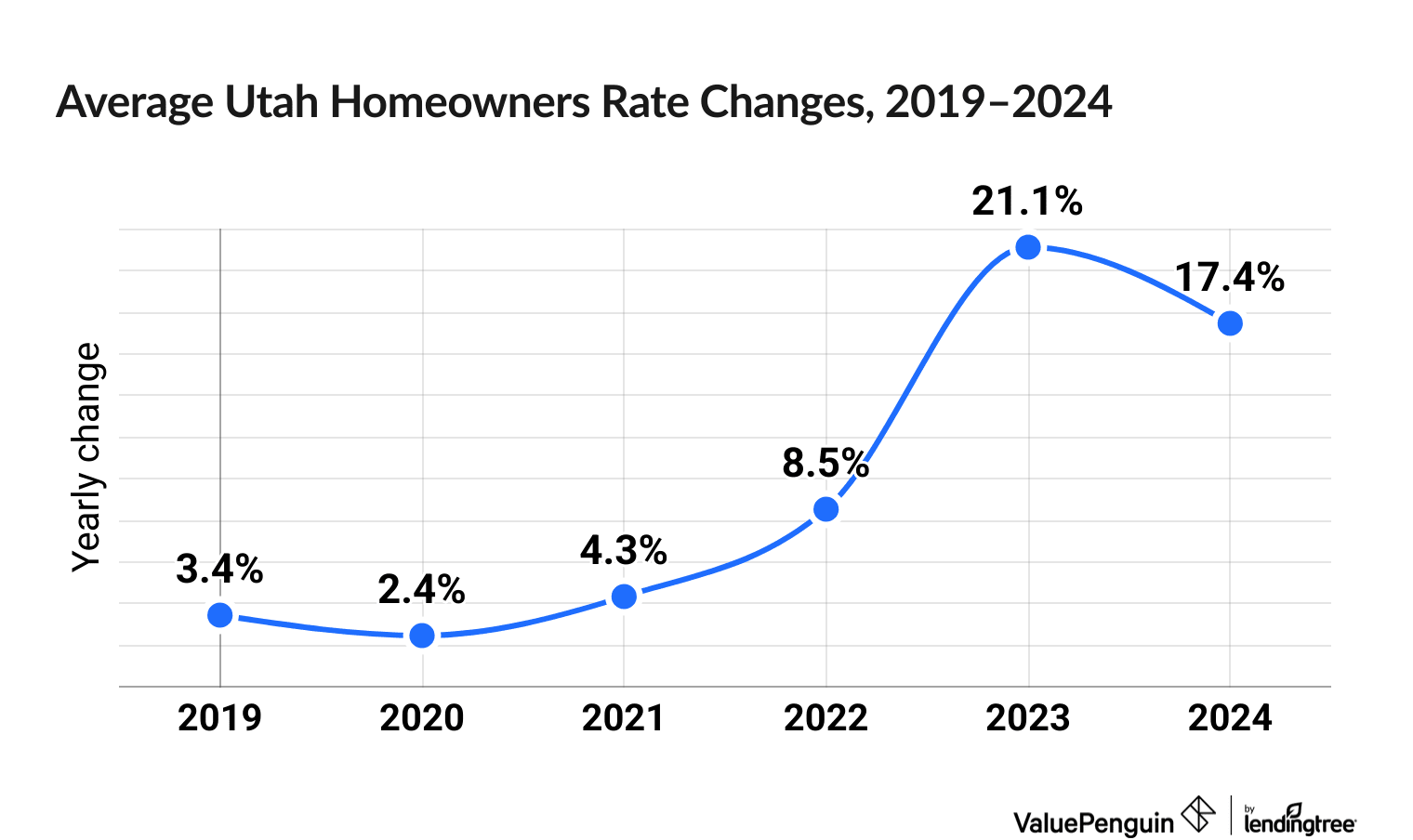

Home insurance prices are up 70.6% in Utah over the last six years.

Utah homeowners have been experiencing steep increases in their home insurance prices, with increases of 21.1% and 17.4% in 2023 and 2024, respectively.

Utah has seen such a sharp rise in its home insurance costs due to inflation, increased wildfire risk, and the rise in associated costs of these weather events.

In Utah, two insurance companies experienced their home insurance prices more than double over the last six years: Auto-Owners (146.6%) and Progressive (115.0%). The state average was just 70.6.%

The smallest increase belonged to State Farm, at just 24.0%. Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

Frequently asked questions

What's the best cheap home insurance in Utah?

State Farm has the best cheap home insurance in Utah because of its cheap rates and strong customer service. Mutual of Enumclaw is a good choice if you'd like to take advantage of its private firefighting service.

What is the average cost of home insurance in Utah?

Home insurance in Utah costs $1,137 for $350,000 on average for coverage to repair or rebuild your home, called dwelling coverage. That's around half the national average for homeowners insurance.

Does Utah require homeowners insurance?

No, Utah does not require homeowners to buy insurance. But, lenders often require you to buy home insurance to get a mortgage.

Methodology

To find the best homeowners insurance in Utah, ValuePenguin collected quotes from the top home insurance companies across all of Utah's residential ZIP codes. Rates are for a 45-year-old married man who has never had an insurance claim.

Quotes include the following coverage limits:

- Dwelling coverage: $200,000, $350,000, $500,000 or $1 million

- Personal liability: $100,000

- Medical payments: $5,000

- Deductible: $1,000

Insurance rate data came from Quadrant Information Services. Quadrant's rates are from public insurance company filings and should only be used for comparative purposes. Your rates will likely be different.

Complaint data from the National Association of Insurance Commissioners (NAIC), the J.D. Power customer satisfaction survey and ValuePenguin's ratings were used to create home insurance ratings.

About the Author

Former Senior Writer

Talon Abernathy is a former ValuePenguin Senior Writer who specialized in health insurance, Medicare and Medicaid. He also contributed to other insurance verticals including home, renters, auto, motorcycle and flood insurance.

Talon came to ValuePenguin in 2023. Since his arrival, he's helped to expand the site's health insurance-related content offerings. He enjoys helping readers understand the ins and outs of America's all too complicated health insurance landscape.

Before coming to ValuePenguin, Talon worked as a freelance writer. His prior work has touched on a broad range of personal finance-related topics including credit-building strategies, small business incorporation tactics and creative ways to save for retirement.

Insurance tip

In many parts of the country, you can qualify for a free Silver health insurance plan if you meet certain income requirements. Government subsidies in the form of premium tax credits and cost-sharing reductions may mean you'll pay nothing for coverage.

Expertise

- Health insurance

- Medicare and Medicaid

- Flood insurance

- Homeowners insurance

- Renters insurance

- Auto and motorcycle insurance

Referenced by

- The Miami Herald

- Money.com

- MSN

- Nasdaq

- The Sacramento Bee

- Yahoo! Finance

Education

- BA, University of Washington

- Certificate in Copyediting, UC San Diego

Credentials

- Licensed Life & Disability Insurance Agent

- Licensed Property & Casualty Insurance Agent

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.