The Best and Cheapest Homeowners Insurance Companies in Maryland (2026)

Brethren Mutual has the cheapest home insurance rates for most homes in Maryland, at an average of $1,297/yr. | ||

Home insurance in Maryland costs an average of $2,124/yr, making it the 23rd least expensive state in the country for home coverage. | ||

Baltimore home insurance is about 24% higher than the state average overall, with average rates higher than $2,600/yr. |

Brethren Mutual has the cheapest home insurance rates for most homes in Maryland, at an average of $1,297/yr. | ||

Home insurance in Maryland costs an average of $2,124/yr. The average in Baltimore is higher, at more than $2,600/yr. |

Find Cheap Home Insurance Quotes in Maryland

Who has the best cheap home insurance in Maryland?

Who has the cheapest MD home insurance?

Brethren Mutual and State Farm have the cheapest homeowners insurance in Maryland.

Find Cheap Home Insurance Quotes in Maryland

-

Brethren Mutual offers Maryland's cheapest home insurance rates for people with moderately priced homes. Average prices for homeowners insurance from Brethren Mutual are typically 39% to 52% less than the statewide average, depending on how much coverage you need.

But as a smaller, local company, you'll have to set up your policy with an agent. That includes learning about discounts and coverage options as well as getting a quote. You also can't file a claim online, so you will have to do that over the phone as well.

- State Farm has the cheapest rates in Maryland for homes that would cost $500,000 or $1 million to rebuild. The company also has the cheapest rates in Baltimore, the state's largest city.

- The biggest concern for Maryland homeowners is water damage and storms. Water causes the most damage to homes in the state, and Maryland has been hit by an increasing number of severe storms in recent years.

Cheap homeowners insurance in Maryland

$200,000

$350,000

$500,000

$1 million

Company | Annual rate | ||

|---|---|---|---|

| Brethren Mutual | 5.0 out of 5 | $733 |

| State Farm | 3.5 out of 5 | $1,024 | |

| Penn National | 5.0 out of 5 | $1,130 |

| Erie | 4.0 out of 5 | $1,193 | |

| Nationwide | 3.3 out of 5 | $1,438 | |

| American Family | 3.3 out of 5 | $1,513 | |

| Allstate | 2.5 out of 5 | $2,514 | |

| Pure | 2.3 out of 5 | $2,807 |

| USAA | 4.0 out of 5 | $1,359 | |

Key takeaways

-

Home insurance rates in Maryland only went up a little in 2025 after big jumps in 2023 and 2024. In those years, home insurance rates went up by more than 12%, on average, but the 2025 increase was just a little more than 3%.

The state has seen an increase in events that caused $1 billion or more in damage, especially severe and winter storms. Those could be contributing to the rise in rates.

- Farmers has raised home insurance rates the most in Maryland across the past five years, more than doubling its prices. Progressive increased costs the second-most, by more than 73%. USAA increased rates the least, by less than 15% from 2021 to 2025.

- Water damage, both from weather and nonweather situations like leaking pipes, causes the most damage to homes in Maryland. Homeowners insurance will pay for most kinds of water damage, unless it's the result of flooding. If you live in a flood-prone area, such as parts of Anne Arundel, Dorchester and Baltimore counties, you should look at options for flood insurance.

Best homeowners insurance in Maryland for most people: Brethren Mutual

-

Annual cost$1,297Average rate for a $350,000 home

-

Monthly cost$108Average rate for a $350,000 home

-

Customer complaints Low

Best homeowners insurance in Maryland for customer service: Erie

-

Annual cost$1,892Average rate for a $350,000 home

-

Monthly cost$158Average rate for a $350,000 home

-

Customer complaints Low

Insurance quotes for new homes in Maryland

[table align="left left right right" max_default_rows="5" footnote="Rates are for a policy with $350,000 of dwelling coverage.] Company | <<< | Annual rate | <<< _ | Erie |

Cheapest home insurance in Baltimore: State Farm

-

Annual cost$1,395Average rate for a $350,000 home

-

Monthly cost$116Average rate for a $350,000 home

-

Customer complaints Average

Cheapest homeowners insurance in Baltimore

Company | Annual rate | ||

|---|---|---|---|

| State Farm | $1,395 | ||

|

| Penn National | $1,929 | |

| Erie | $2,048 | ||

|

| Brethren Mutual | $2,081 | |

| American Family | $2,811 | ||

| Allstate | $3,174 | ||

| Chubb | $3,412 | ||

| Nationwide | $3,740 | ||

|

| Pure | $3,842 | |

| USAA | $1,927 | ||

Rates are for a policy with $350,000 of dwelling coverage.

The best home insurance companies in Maryland

Brethren Mutual, Penn National, Erie and USAA have the best combination of cheap rates and strong customer service across Maryland.

Brethren Mutual and Penn National are smaller regional companies, but they're affordable and get very few complaints. USAA has a strong historical reputation for service, but you can only get coverage if you're a member of the military or a veteran, or if you have certain relatives who were members.

Erie isn't the cheapest option, but its rates are lower than average, and it has a great reputation for service.

Company |

Rating

|

Complaints

|

|---|---|---|

| Brethren Mutual | 5.0 out of 5 | Low |

| Penn National | 5.0 out of 5 | Low |

| Erie | 4.0 out of 5 | Low |

| USAA | 4.0 out of 5 | Low |

| State Farm | 3.5 out of 5 | Average |

| American Family | 3.3 out of 5 | Average |

| Nationwide | 3.3 out of 5 | High |

| Allstate | 2.5 out of 5 | Average |

| Chubb | 2.5 out of 5 | Average |

| Pure | 2.3 out of 5 | Low |

How much does home insurance cost in Maryland?

Homeowners insurance in Maryland costs $2,124 per year for $350,000 of dwelling coverage on average.

That comes in at 11% cheaper than the national average, which is $2,395 per year.

Average cost of home insurance in MD

Dwelling coverage | Average rate |

|---|---|

| $200,000 | $1,523 |

| $350,000 | $2,124 |

| $500,000 | $3,010 |

| $1 million | $5,563 |

Maryland has slightly more expensive rates than most of its neighboring states. Average home insurance prices in Maryland are between 11% and 82% higher than in Delaware, Pennsylvania and West Virginia. But Maryland quotes are about 14% cheaper than in Virginia.

Maryland homeowners insurance quotes by city

Ocean City, a resort town on a narrow barrier island on the Atlantic coast, has the most expensive home insurance rates in Maryland.

Average rates in Ocean City are $3,574 per year. The 15 most expensive cities or towns in the state for home insurance are on the eastern shore, usually near the ocean or on islands and peninsulas in the Chesapeake Bay.

Chevy Chase Village has the cheapest homeowners coverage in Maryland at $1,860 per year, on average. Many of the cheapest places in the state for home insurance are in the Washington, D.C., suburbs.

Brethren Mutual has the cheapest rates in about three-fourths of the state. State Farm is usually the cheapest option in the rest of Maryland.

Find Cheap Home Insurance Quotes in Maryland

Annual home insurance rates in MD by city

City | Average rate | Cheapest company | Cheapest rate |

|---|---|---|---|

| Abell | $2,467 | Brethren Mutual | $1,238 |

| Aberdeen | $2,087 | Brethren Mutual | $928 |

| Aberdeen Proving Ground | $2,090 | Brethren Mutual | $928 |

| Abingdon | $2,052 | Brethren Mutual | $928 |

| Accident | $2,196 | State Farm | $1,242 |

| Accokeek | $2,395 | State Farm | $1,495 |

| Adamstown | $2,117 | State Farm | $1,225 |

| Adelphi | $2,225 | State Farm | $1,247 |

| Algonquin | $2,362 | Brethren Mutual | $1,304 |

| Allen | $2,479 | Brethren Mutual | $1,304 |

| Andrews Air Force Base | $2,326 | Brethren Mutual | $1,616 |

| Annapolis | $2,046 | Brethren Mutual | $1,065 |

| Annapolis Junction | $1,959 | Brethren Mutual | $928 |

| Annapolis Neck | $2,045 | Brethren Mutual | $1,065 |

| Aquasco | $2,469 | State Farm | $1,393 |

| Arbutus | $2,224 | Brethren Mutual | $1,355 |

| Arden on the Severn | $1,985 | Brethren Mutual | $1,065 |

| Arnold | $2,035 | Brethren Mutual | $1,065 |

| Ashton | $1,914 | Brethren Mutual | $1,009 |

| Aspen Hill | $1,925 | Brethren Mutual | $1,009 |

| Avenue | $2,445 | Brethren Mutual | $1,238 |

| Baden | $2,401 | State Farm | $1,416 |

| Baldwin | $2,124 | Brethren Mutual | $1,355 |

| Ballenger Creek | $2,099 | State Farm | $1,242 |

| Baltimore | $2,636 | State Farm | $1,395 |

| Barclay | $2,249 | Brethren Mutual | $1,304 |

| Barnesville | $1,932 | Brethren Mutual | $1,009 |

| Barstow | $2,379 | Brethren Mutual | $1,238 |

| Barton | $2,172 | State Farm | $1,271 |

| Beallsville | $1,989 | Brethren Mutual | $1,009 |

| Bel Air | $2,045 | Brethren Mutual | $928 |

| Bel Air North | $2,044 | Brethren Mutual | $928 |

| Bel Air South | $2,045 | Brethren Mutual | $928 |

| Bel Alton | $2,460 | Brethren Mutual | $1,238 |

| Belcamp | $2,069 | Brethren Mutual | $928 |

| Beltsville | $2,260 | State Farm | $1,263 |

| Benedict | $2,414 | Brethren Mutual | $1,238 |

| Benson | $2,052 | Brethren Mutual | $928 |

| Bensville | $2,281 | Brethren Mutual | $1,238 |

| Berlin | $3,319 | State Farm | $1,668 |

| Berwyn Heights | $2,237 | State Farm | $1,308 |

| Bethesda | $1,896 | Brethren Mutual | $1,009 |

| Bethlehem | $2,213 | Brethren Mutual | $1,304 |

| Betterton | $2,192 | Brethren Mutual | $1,304 |

| Big Pool | $2,177 | Brethren Mutual | $1,278 |

| Bishopville | $3,332 | State Farm | $1,712 |

| Bittinger | $2,283 | Brethren Mutual | $1,278 |

| Bivalve | $2,394 | Brethren Mutual | $1,304 |

| Bladensburg | $2,454 | State Farm | $1,418 |

| Bloomington | $2,256 | Brethren Mutual | $1,278 |

| Boonsboro | $2,167 | State Farm | $1,256 |

| Boring | $2,095 | Brethren Mutual | $1,355 |

Rates are for a policy with $350,000 of dwelling coverage.

What home insurance coverage do I need in Maryland?

Severe storms and water damage are two of the biggest risks Maryland homeowners need coverage for. Snowstorms can also be a concern if you live in the state.

Does homeowners insurance cover water damage in Maryland?

Home insurance covers some types of water damage, but it usually won't cover damage caused by flooding.

Water does the most damage to homes in Maryland. Home insurance will usually pay for repairs after a pipe breaks or a washing machine overflows. If an event like that also floods your basement, most policies will cover that too.

Regular home insurance almost never pays for damage after a large-scale flood, so if you want coverage, you'll have to get a separate flood policy. Your mortgage company may require that you get flood coverage if you live in an area deemed high risk by the Federal Emergency Management Agency (FEMA). In a coastal state such as Maryland, that could include a large number of homes.

Flooding caused more than $31 million in damage in Maryland between 2020 and 2025, based on National Flood Insurance Program (NFIP) claim payouts. The damage was heaviest in Dorchester and Anne Arundel counties.Does homeowners insurance cover wind damage in Maryland?

Your home insurance will cover normal wind damage, but policies may limit coverage for powerful windstorms, tropical storms or hurricanes.

Although Maryland isn't traditionally thought of as a state that experiences hurricanes, the remnants of storms that hit farther south can reach up to its coast. It could be a good idea to look into extra coverage, called hurricane coverage, to protect against these storms.

Severe storm damage has been on the rise in recent years in Maryland. The state experienced 19 storms that did more than $1 billion in damage between 2020 and 2024 alone.

Does homeowners insurance cover snow damage in Maryland?

Most standard home insurance plans will cover damage caused by snow and ice.

Maryland commonly experiences freezing temperatures and snowstorms in the winter. Between 2018 and 2024, four winter storms caused at least $1 billion in damage.

It's a good idea to take standard precautions to protect your home. For example, your home insurance policy typically won't pay for damage caused by snow that blew in through an open window.

Tips to save money on your Maryland home insurance policy

You could save hundreds or thousands of dollars a year on homeowners insurance by comparing quotes, finding discounts and making improvements to your home.

Get quotes and check rates from multiple companies. Companies use different ways to calculate home insurance rates, so shopping around can help you find the lowest rate for the same coverage.

For example, the cheapest company in Maryland, Brethren Mutual, costs 60% less than the most expensive company, Allstate. That's an average savings of more than $1,900 per year.

Search for discounts. Most home insurance companies offer at least a few discounts. Common discounts include price breaks for bundling different kinds of insurance, switching companies or going a certain amount of time without filing a claim.

Improve your home. If you can make changes to your home that lower the chance you'll file a claim, you'll very likely be able to save on insurance in the long run.

Those changes might include installing a better drainage system to avoid basement flooding or building more sturdy walls to stand up better to wind. It can also be properly maintaining your home, particularly your windows, siding, doors and roof, to make sure water or other elements don't get in.

One of the biggest improvements can be updating your roof. Weather such as rain, wind, hail and snow can do more damage to an older roof. Repairing or replacing an old roof with a new one can often save you money on your annual bill and in the long run.

If your roof has been damaged or hasn't been replaced in more than 15 years, it's a good idea to have a professional look at it.

Home insurance trends in Maryland

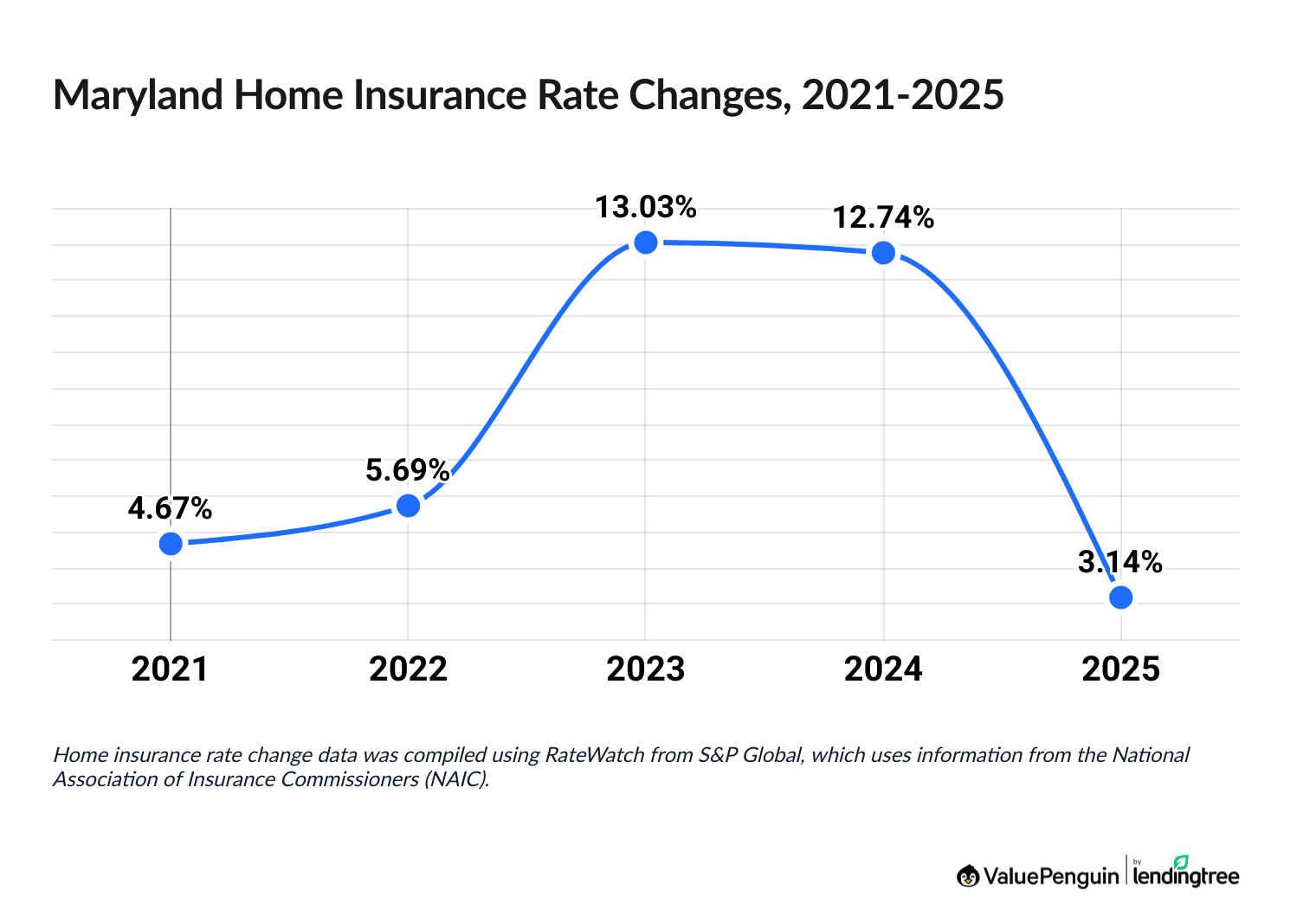

Home insurance rates increased by 45.5% in Maryland from 2021 through 2025.

That's a little less than the national average of almost 48%. Rates didn't go up much in 2025, only 3.1% after double-digit jumps the previous two years.

Home insurance rate hikes in Maryland, 2021-2025

Year | Rate increase |

|---|---|

| 2021 | 4.67% |

| 2022 | 5.69% |

| 2023 | 13.03% |

| 2024 | 12.74% |

| 2025 | 3.14% |

Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

Farmers raised rates the most in the past five years, more than doubling them, even after lowering rates in 2025. USAA raised rates the least, around 15%, and State Farm, American Family and Chubb also had relatively smaller increases, between 30% and 37%.

Frequently asked questions

How much is home insurance in Maryland?

The average cost of homeowners insurance in Maryland is $2,124 per year for $350,000 of dwelling coverage. That's about 11% or $271 per year less than the national average of $2,395 per year.

How much is flood insurance in Maryland?

Flood insurance in Maryland costs $498 per year, on average. That's 48% cheaper than the national average.

What's the best homeowners insurance in Maryland?

Brethren Mutual has the best homeowners insurance in Maryland. It has extremely low rates and receives few customer complaints. Erie, USAA and State Farm are also good options in the state.

Methodology

ValuePenguin collected quotes from the top companies across every residential ZIP code in Maryland to find the best homeowners insurance in the state. Rates are for a 45-year-old married man with no previous insurance claims. Quotes are for a 2,207 square foot home built 45 years ago, matching the average home age and size in Maryland.

Quotes include the following coverage limits:

- Dwelling coverage: $200,000, $350,000, $500,000 or $1 million

- Personal liability: $100,000

- Medical payments: $1,000

- Deductible: $1,000

ValuePenguin's analysis used insurance rate data from Quadrant Information Services. Quadrant's rates were publicly sourced from insurer filings and should only be used for comparative purposes.

Home insurance ratings are based on complaint data from the National Association of Insurance Commissioners (NAIC), the J.D. Power customer satisfaction and claims satisfaction surveies and ValuePenguin's ratings.

Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

Sources:

About the Author

Managing Editor

Ben Breiner is the Managing Editor of ValuePenguin/LendingTree's insurance vertical. He oversees a team of writers who focus on guiding readers through the rigors of home and auto coverage. He still loves that moment when the words fall together and he can translate an intimidating topic so a reader can make the best choice.

Ben got involved in insurance in 2021 when he joined ValuePenguin. He moved up from writer to editor and watched the team grow to expand the ways it helps consumers. Before that, he spent a decade as a sportswriter for newspapers in the Southeast and Midwest.

Ben had to put off buying his first car because of high insurance rates, so he's keenly aware how the wrong policy can get in the way of your goals. He should've shopped around and looked to the experts.

Insurance tip

Always keep an eye out for insurance you can load up on at a low price. A lot more liability coverage won't break the bank and protects your hard-earned assets.

Expertise

- Car insurance

- Home insurance

- Renters insurance

Education

- BA, Economics and Journalism, University of Wisconsin-Madison

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.