Best and Cheapest Home Insurance in California (2026)

Travelers has the cheapest home insurance in California, at $730/yr. | ||

Home insurance in California costs an average of $1,413/yr, or 41% cheaper than the national average. | ||

Homes in the mountains near Los Angeles tend to pay the most for home insurance, with rates about $750/yr more than the state average. |

Find Cheap Home Insurance Quotes in California

Best cheap home insurance in CA

Who has the best cheap home insurance in California?

Travelers has the cheapest home insurance rates in California.

Find Cheap Homeowners Insurance Quotes in Your Area

Cheap home insurance quotes in California

$200,000

$350,000

$500,000

$1 million

Company | Annual rate | ||

|---|---|---|---|

| Travelers | 2.5 out of 5 | $494 | |

| AAA SoCal | 3.0 out of 5 | $575 | |

| Pacific Specialty | 3.8 out of 5 | $578 |

| AAA NorCal | 3.0 out of 5 | $683 | |

| Mercury | 2.0 out of 5 | $861 | |

| Nationwide | 4.0 out of 5 | $875 | |

| Cincinnati | 3.3 out of 5 | $1,060 | |

| Farmers | 3.0 out of 5 | $1,264 | |

| Progressive | 2.5 out of 5 | $1,282 | |

| California Casualty | 0.8 out of 5 | $1,882 |

| USAA | 4.5 out of 5 | $929 | |

-

Travelers offers rates averaging $730 per year for $350,000 of coverage. That's about half the state average and $101 less than the second-cheapest option, Pacific Specialty.

-

Home insurance has been hard to get in California over the last few years due to wildfires, inflation and regulatory issues. But that may start to change in 2026.

-

On average, home insurance in California costs $1,413 per year for $350,000 of coverage.

What's happening with the California home insurance crisis?

Over the last several years, home insurance has gotten both more expensive and harder to get for many Californians. But that may start to change in 2026.

The two key things affecting home insurance prices are the increasing risk of wildfires in the state and the limits the California Department of Insurance puts on how much insurance companies can charge for coverage.

Wildfires have gotten both more destructive and unpredictable in recent years, including the 2025 fires around Los Angeles, which killed at least 31 people and caused more than $40 billion of insured property damage, according to industry experts.

Meanwhile, insurance companies are strictly limited in how much they're allowed to raise prices, and the reasons they can use for those rate hikes. That means it's more difficult for insurance companies to be profitable in California.

In 2023, several major companies, including State Farm and Allstate, stopped selling new policies in California, while others sold fewer policies in higher-risk areas.

That led to a big jump in people being forced to buy a policy from California's FAIR Plan, a state-run insurer of last resort that offers limited coverage for high-risk homes.

Starting in 2025, California's new plan for home insurance gave insurance companies more leeway when setting prices in exchange for promising to cover more homes in high-risk areas.

The number of people who have signed up for the California FAIR Plan has slowed in recent months, suggesting that the changes may be helping.

But so far, Allstate and State Farm have still not agreed to start selling new home insurance policies again in California.

Best for most people: Nationwide

-

Annual cost$1,249Average rate for a $350,000 home

-

Monthly cost$104Average rate for a $350,000 home

-

Customer complaints High

Best home insurance in CA for cheap rates: Travelers

-

Annual cost$730Average rate for a $350,000 home

-

Monthly cost$61Average rate for a $350,000 home

-

Customer complaints Average

Best for high-value homes: Chubb

-

Annual cost$4,909Average rate for a $1 million home

-

Monthly cost$409Average rate for a $1 million home

-

Customer complaints Low

Best-rated California home insurance companies

USAA and Nationwide have the best home insurance in California.

USAA earned top marks from our editors for combining cheap quotes, good coverage options and highly rated customer support. However, USAA is only available to military members, veterans and their families.

Nationwide is the best overall choice if you're not eligible for coverage from USAA. It has great coverage options and low rates. For example, it offers earthquake insurance, which isn't usually available from home insurance companies.

California home insurance company reviews

Company |

Rating

|

Complaints

|

|---|---|---|

| USAA | 4.5 out of 5 | Low |

| Nationwide | 4.0 out of 5 | High |

| Chubb | 3.8 out of 5 | Low |

| Pacific Specialty | 3.8 out of 5 | High |

| Cincinnati | 3.3 out of 5 | Low |

| AAA NorCal | 3.0 out of 5 | High |

| AAA SoCal | 3.0 out of 5 | High |

| Farmers | 3.0 out of 5 | Average |

| Progressive | 2.5 out of 5 | High |

| Travelers | 2.5 out of 5 | Average |

| Mercury | 2.0 out of 5 | High |

| California Casualty | 0.8 out of 5 | High |

Average home insurance cost in California

The average cost of homeowners insurance in California is $1,413 per year.

That's 41% cheaper than the national average of $2,395 per year.

Average cost of home insurance in CA by dwelling coverage amount

Dwelling coverage | Average rate |

|---|---|

| $200,000 | $953 |

| $350,000 | $1,413 |

| $500,000 | $2,041 |

| $1 million | $3,737 |

Despite recent big shifts in the California home insurance market, the cost of coverage in California is cheaper than in neighboring Arizona and Nevada, where policies cost $2,225 and $1,633 per year, respectively.

But rates in Oregon are a little cheaper, at $1,353 per year. That's 4% less expensive than the California average.

Cost of insurance by city in California

The most expensive city in California for homeowners insurance is Beverly Hills.

There, an average policy costs $2,120 per year. The cheapest city for homeowners insurance is Santa Clara, where home insurance costs around $1,124 per year.

The most expensive cities for home insurance in California are mostly in the mountains surrounding Los Angeles.

The cheapest company varies by city, but AAA, Travelers and Pacific Specialty tend to offer comparatively low rates in high-risk areas.

Cost of California home insurance by city

City | Average rate | Cheapest company | Cheapest rate |

|---|---|---|---|

| Acalanes Ridge | $1,389 | Travelers | $545 |

| Acampo | $1,346 | Travelers | $725 |

| Acton | $2,104 | Travelers | $929 |

| Adelanto | $1,758 | Travelers | $928 |

| Adin | $1,840 | Pacific Specialty | $882 |

| Agoura Hills | $1,749 | AAA SoCal | $865 |

| Agua Dulce | $1,885 | Travelers | $882 |

| Aguanga | $1,835 | Pacific Specialty | $797 |

| Ahwahnee | $1,685 | Travelers | $580 |

| Airport | $1,353 | Travelers | $793 |

| Alameda | $1,305 | Travelers | $555 |

| Alamo | $1,401 | Travelers | $616 |

| Albany | $1,316 | Travelers | $508 |

| Albion | $1,390 | Travelers | $688 |

| Alderpoint | $1,368 | Pacific Specialty | $752 |

| Alhambra | $1,335 | Pacific Specialty | $694 |

| Aliso Viejo | $1,898 | Travelers | $886 |

| Alleghany | $1,719 | Travelers | $660 |

| Allendale | $1,364 | Travelers | $645 |

| Alondra Park | $1,657 | AAA SoCal | $736 |

| Alpaugh | $1,489 | Travelers | $636 |

| Alpine | $1,644 | Travelers | $687 |

| Alta | $1,758 | Travelers | $661 |

| Alta Sierra | $1,704 | Travelers | $670 |

| Altadena | $1,459 | Travelers | $597 |

| Altaville | $1,632 | Travelers | $845 |

| Alturas | $1,696 | Travelers | $849 |

| Alum Rock | $1,238 | Travelers | $585 |

| Alviso | $1,236 | Travelers | $454 |

| Amador City | $1,606 | Pacific Specialty | $889 |

| Amboy | $1,983 | Travelers | $862 |

| American Canyon | $1,290 | Travelers | $556 |

| Amesti | $1,313 | Pacific Specialty | $658 |

| Anaheim | $1,527 | Travelers | $730 |

| Anderson | $1,729 | Travelers | $779 |

| Angels | $1,666 | Travelers | $845 |

| Angels Camp | $1,667 | Travelers | $845 |

| Angelus Oaks | $1,967 | Pacific Specialty | $974 |

| Angwin | $1,384 | Travelers | $586 |

| Annapolis | $1,251 | Pacific Specialty | $667 |

| Antelope | $1,394 | Travelers | $747 |

| Antioch | $1,398 | Travelers | $627 |

| Anza | $1,931 | Pacific Specialty | $992 |

| Apple Valley | $1,686 | Travelers | $883 |

| Applegate | $1,649 | Travelers | $810 |

| Aptos | $1,314 | Travelers | $544 |

| Aptos Hills-Larkin Valley | $1,312 | Pacific Specialty | $667 |

| Arbuckle | $1,499 | Pacific Specialty | $889 |

| Arcadia | $1,383 | Travelers | $646 |

| Arcata | $1,301 | Travelers | $680 |

| Arden-Arcade | $1,344 | Travelers | $669 |

| Armona | $1,310 | Travelers | $646 |

Rates are for a policy with $350,000 of dwelling coverage.

What are the most common natural disasters in California?

California has great weather most of the year, but it's very susceptible to wildfires and earthquakes, plus occasional flooding.

Fire insurance in California

Fire damage is typically always covered by a standard homeowners insurance policy, unless your home insurance company has specifically told you otherwise.

Wildfires in California are unpredictable but can be wildly destructive.

In a given year, wildfires might burn only a few hundred thousand acres, or they might burn millions. But irrespective of size, the cost of fires can reach tens of billions of dollars, as was the case in the 2025 Los Angeles wildfires.

If your home is especially high-risk for wildfires, you may have trouble getting coverage or only be offered a policy that won't cover wildfire damage.

-

If the area where you live is currently experiencing a wildfire, you likely won't be able to buy a new policy or switch insurance companies until the fire dies out.

-

Many companies won't sell new policies in areas where fires continue to burn. Others may have a 30-to-60-day waiting period before your coverage starts.

-

The California FAIR Plan may still sell policies in areas with ongoing wildfires. However, it may take longer for FAIR to approve your application and start coverage.

Wildfires are a major threat to homes throughout California. Nine of the 10 largest wildfires in California's history have occurred in the last 10 years.

Top 10 most destructive California wildfires

Fire name | Year | Acres burned |

|---|---|---|

| August Complex (includes Doe Fire) | 2020 | 1,032,648 |

| Dixie Fire | 2021 | 963,309 |

| Park Fire | 2024 | 429,603 |

| Ranch Fire (Mendocino Complex) | 2018 | 410,203 |

| SCU Lightning Complex | 2020 | 396,624 |

| Creek Fire | 2020 | 379,895 |

| LNU Lightning Complex | 2020 | 363,220 |

| Thomas Fire | 2017 | 281,893 |

| Rim Fire | 2013 | 257,314 |

| Carr Fire | 2018 | 229,651 |

How to insure a home at high risk of wildfires

If you're unable to get a homeowners insurance quote from a typical insurance company because you're located in an area at high risk for fires, then you can try the following:

- Talk to an independent insurance agent who can help you find specialized insurance companies that provide coverage in high-risk zones.

- Consider the California FAIR Plan Association for fire insurance coverage, which is usually a last resort for coverage because it is more expensive than private home insurance.

California FAIR Plan insurance

The California FAIR Plan offers property insurance to homeowners and renters who have trouble getting insurance through a private company.California's FAIR Plan only covers a few types of damage, like fire and smoke. You can add coverage for windstorms, vandalism and other common types of damage.

But CA FAIR doesn't offer protection against water damage, and you can only insure your home and personal property for a combined maximum of $3 million. That may not be enough coverage if you have an expensive home.

How to protect your home from wildfires

Homeowners insurance can be expensive in wildfire-prone areas. However, many homeowners can earn a discount for fire prevention home improvements, such as:

- Installing a Class-A fire-rated roof

- Maintaining a 5-foot ember-resistant zone around your home

- Upgrading to double-pane windows or adding shutters

- Enclosing eaves

- Clearing vegetation and debris

- Removing flammable sheds and other outbuildings

Many home insurance companies in California also offer discounts to people living in areas with community-wide fire mitigation techniques, such as adequate fire hydrants and water availability.

Do I need earthquake insurance in California?

Earthquake damage generally won't be covered by basic homeowners insurance in California. You will need a separate insurance policy.

Homeowners can get earthquake insurance through the California Earthquake Authority (CEA). It sells publicly supported earthquake policies and insurance through private companies. There are a couple of requirements to get CEA earthquake coverage:

- You must already have a residential property insurance policy (homeowners, renters or condo insurance).

- If your current insurance provider participates in the CEA, then you must get your CEA earthquake insurance from that same company.

California sees a fair amount of earthquake activity, and while major earthquakes aren't a very frequent occurrence, the damage can be severe.

The 2019 Ridgequest earthquakes were the most recent major earthquakes in the state, and they caused about $5 billion in damage to a military base.

But the peak intensity was in a relatively sparsely populated area, and damage could be drastically worse if an earthquake hit a more populous area like Los Angeles or the Bay Area.

Earthquake insurance is not required by mortgage companies, and it can be expensive. But homeowners in California who do not have coverage will have to pay the full cost of home repairs after an earthquake.

Earthquake insurance in California costs an average of $1,770 per year for a single-family home with $500,000 of replacement cost coverage. To make earthquake insurance more affordable, use a cheap company like Cincinnati. You should also look for discounts for your home's structure, which can save you up to 25%.

Flood and mudslide insurance in California

Flooding is a smaller risk in California compared to other states, but floods still cause millions of dollars of damage per year.

Over the last 10 years, flooding has caused more than $200 million of insured losses in California, according to the National Flood Insurance Program.

Standard homeowners insurance policies do not cover flood damage. You'll need a separate flood insurance policy.

Though California is a coastal state, most flood damage is caused by rainfall, not the ocean. So homeowners closer to rivers are at the highest risk.

Homeowners looking for flood insurance in California can get it from the National Flood Insurance Program, which is sponsored by the federal government, or a private flood insurance company, which may offer higher coverage limits.

Mudslide damage is typically not covered by home insurance. But homeowners may be covered if the mudslide was caused by a covered event.

This was the case in the Montecito mudslides of 2018. Wildfires destroyed vegetation in the area, making it more susceptible to flooding and mudslides. Since fires are covered by homeowners insurance, and the mudslide was ultimately attributed to the fires, insurance companies agreed to cover the damage.

Following this incident, the California legislature passed a law requiring home insurance companies to pay for damage if the initial cause of an event is covered.

How to get cheaper home insurance in California

The three simplest ways to get cheaper home insurance in California are to shop around for quotes, look for discounts and adjust your coverage.

The cheapest home insurance in California will save you more than $2,000 per year compared to the most expensive option. That's why it's important to shop around for quotes every year or two. | |

One of the best discounts is for bundling your home insurance with a cheap auto insurance policy in California, which can save you 10%-15% on your insurance. Some companies also offer discounts for military members, government employees or retirees. If you live in a part of the state prone to wildfires, you can get discounts by fireproofing your property. For example, you can clear away vegetation near your home or have extra sprinklers installed. | |

A higher deductible means the insurance company will pay you less money to fix your damaged home. It's important to choose a deductible you can easily pay in an emergency. You can also lower your coverage limits and get rid of any coverage extras you may not need. However, make sure your limits are high enough to cover the cost of rebuilding your home and replacing your belongings if you have a major accident. |

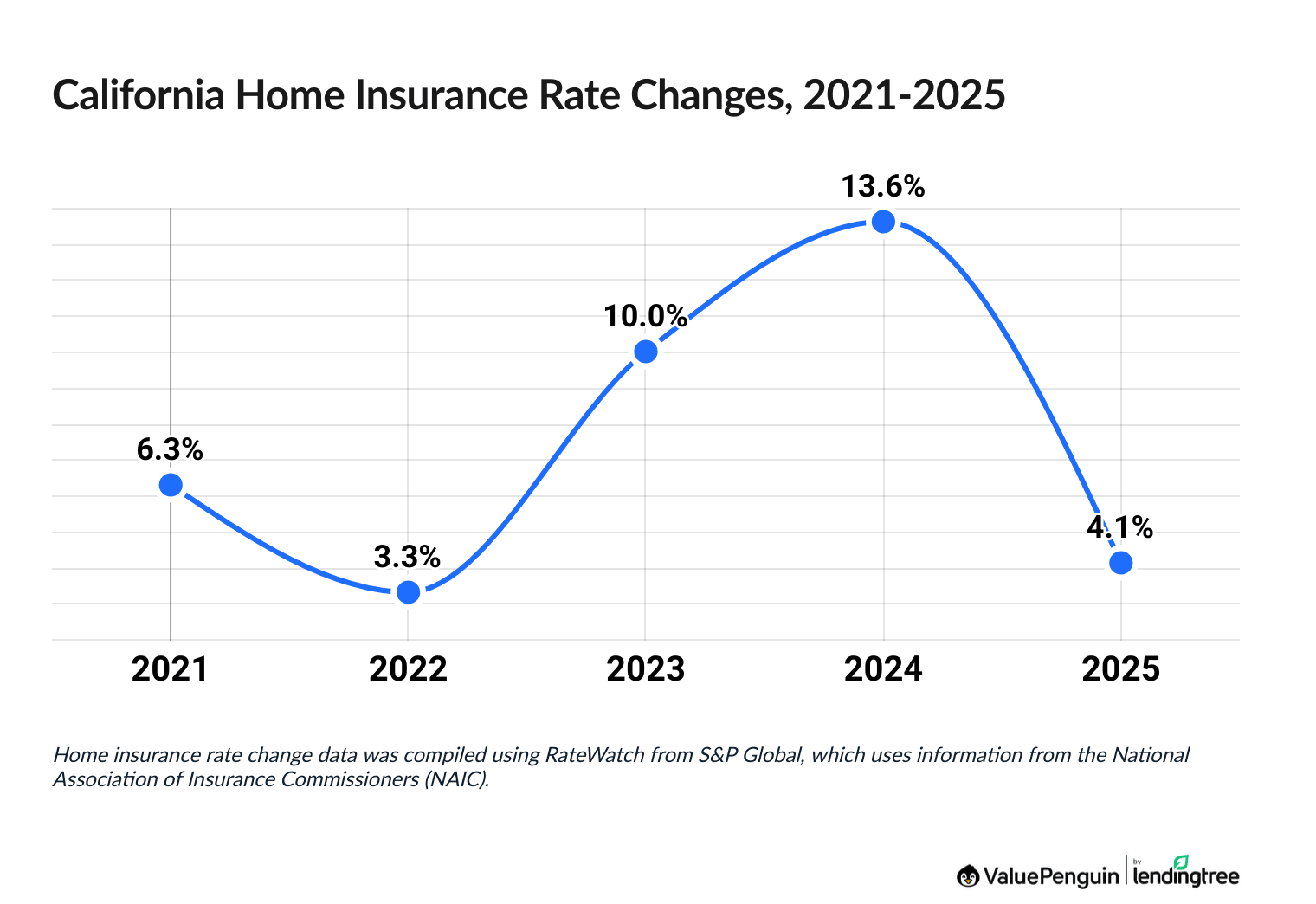

Cost of California home insurance over time

Home insurance costs have increased by 45% in California over the last five years.

That's about typical compared to the national average of 48% overall.

Year | Rate increase |

|---|---|

| 2021 | 6.3% |

| 2022 | 3.3% |

| 2023 | 10.0% |

| 2024 | 13.6% |

| 2025 | 4.1% |

Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

California's Department of Insurance sets strict limits on when and why home insurance companies can raise insurance rates, but recent changes to insurance in California have started to give insurance companies more leeway.

Insurance companies have struggled to match prices to the overall risk of covering a home in California, especially when it comes to predicting how costly future wildfires will be. Regulators were wary of allowing big price increases coming out of the pandemic, but it's likely rates will continue to jump in 2026 and beyond.

Among top insurers, the biggest increases over the last five years have been at AAA NorCal (71%), Mercury (55%) and Travelers (54%).

The smallest increases over that time have been at Chubb (20%) and Nationwide (25%).

Frequently asked questions

How much is home insurance in California?

Homeowners insurance in California costs $1,413 per year, on average, for $350,000 of dwelling coverage. However, average rates can fluctuate between $1,124 and $2,169 depending on where you live in the state.

Is State Farm selling home insurance in California?

No. State Farm is not selling new policies right now, even though it's the largest home insurance company in California. Instead, homeowners looking to buy a policy should look at companies like Travelers or Nationwide.

How much is homeowners insurance in San Diego?

Home insurance in San Diego costs an average of .crvAGR{position:relative

Methodology

To find the best homeowners insurance in California, ValuePenguin gathered quotes in every ZIP code in the state from the largest homeowners insurance companies. Rates are for a 1,860 square foot home built 47 years ago, based on the average home age and size in California.

ValuePenguin sourced quotes for properties at four levels of dwelling coverage to understand the cost of coverage for a variety of homes.

- Dwelling coverage: $200,000, $350,000, $500,000 or $1 million

- Personal liability: $100,000

- Medical payments: $1,000

- Deductible: $1,000

ValuePenguin's analysis used insurance rate data from Quadrant Information Services. These rates were publicly sourced from insurer filings and should be used for comparative purposes only — your own quotes will be different.

Each company's customer service was ranked by comparing the National Association of Insurance Commissioners (NAIC) complaint index, J.D. Power's home insurance customer satisfaction and claims satisfaction rankings and ValuePenguin editor's ratings.

Disaster data is from Cal Fire, the National Flood Insurance Program and KTLA.

About the Author

Lead Writer

Matt Timmons is a Lead Writer on the insurance team at ValuePenguin, where he writes in-depth and timely pieces helping find the right coverage for them.

He's covered insurance at ValuePenguin since 2018, specializing in auto and home insurance, as well as life insurance. He's paid special attention to the EV insurance market, where prices are much higher than for gas cars.

Before he started writing about personal finance, Matt wrote about professional skills and online tools at an e-learning company.

How insurance helped Matt

During freshman orientation in college, Matt's iPod was stolen off his table while he was eating lunch. Luckily, he'd bought a college insurance plan the day before and he had money to buy a replacement before classes started.

Expertise

- Auto insurance

- Home insurance

- Insurance rate analysis

- Life insurance

Referenced by

- CNBC

- Miami Herald

- Yahoo! Finance

Education

- BA, Wesleyan University

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.