Obamacare / ACA Subsidy Calculator

Health Insurance Subsidy Calculator

Calculate your ACA health insurance savings for your income and state.

Your health insurance estimated subsidy

Per person

Income vs. federal poverty level

0%

Your cost for a Silver plan

$0/month

Your cost without the subsidy

$0/month

- Estimate your ACA subsidy to see how much health insurance could cost you every month.

- After you enter your ZIP code and income, you'll see your estimated subsidy for this year and how much you'll potentially pay for health insurance from HealthCare.gov or a state marketplace.

Find Cheap Health Insurance in Your Area

What are ACA subsidies?

As part of the Affordable Care Act (ACA), ACA subsidies (also called "Obamacare" subsidies) give you tax credits that help you pay less for a health insurance plan you buy from an ACA marketplace.

- How it works: Subsidies lower the cost of private health insurance based on the size of your family and your household income. You can use them to lower your monthly bill or your taxes at the end of the year.

- Who can sign up: If you make too much to qualify for Medicaid, but your income is still low, you can sign up on HealthCare.gov or your state’s health insurance marketplace and potentially get subsidies.

- Which insurance plans qualify: ACA subsidies can lower the cost of any company’s Bronze, Silver, Gold or Platinum plans. But you can’t use them on Catastrophic plans, Medicaid, the Children's Health Insurance Program (CHIP) or coverage from a job.

Find Cheap Health Insurance in Your Area

What is the income limit for marketplace insurance?

In 2026, you're eligible for ACA subsidies if you earn between $15,650 and $62,600 as a single person.

A family of four is eligible with a household income between $32,150 and $128,600.

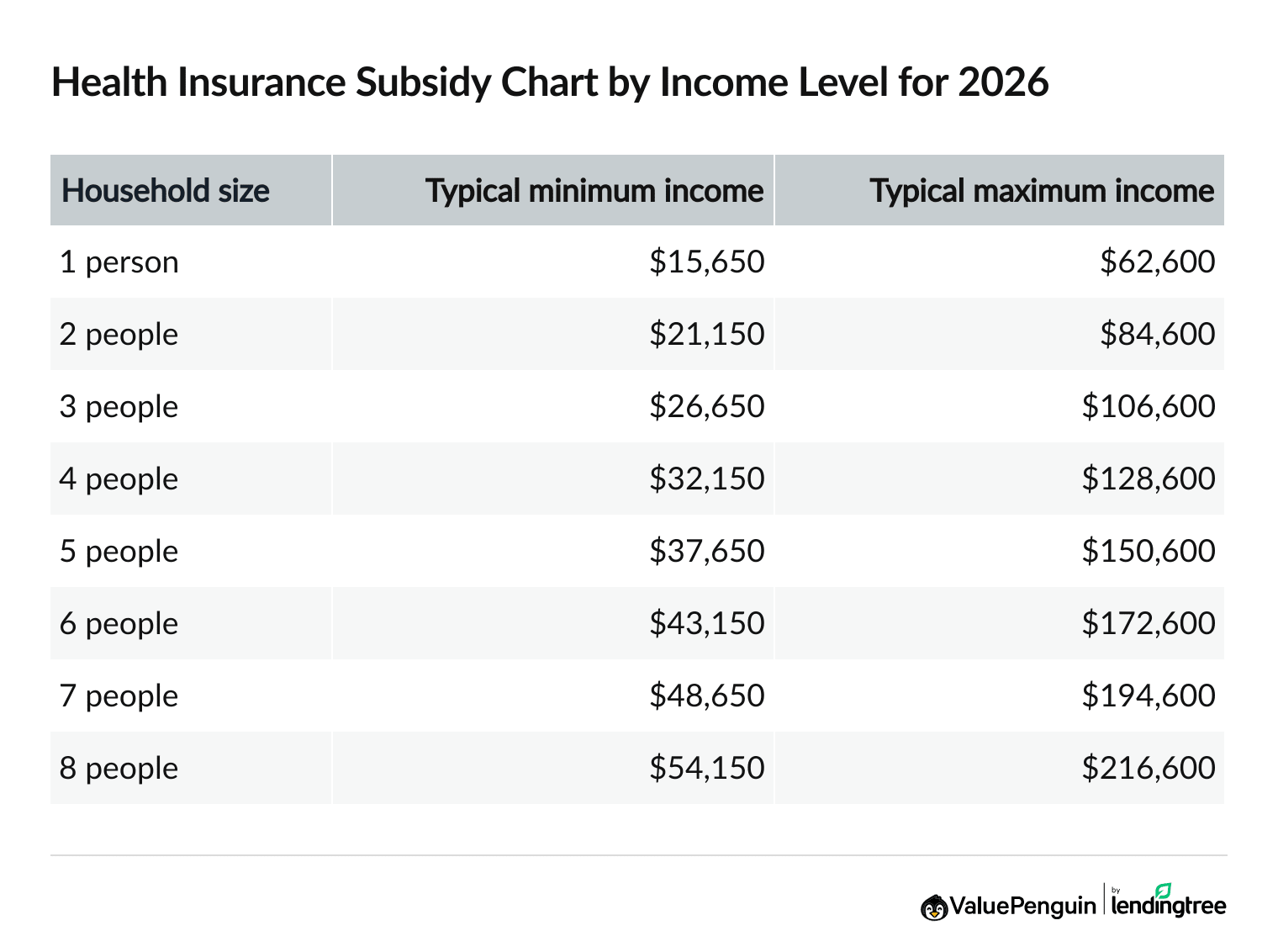

For most people, health insurance subsidies are available if your income is between one and four times the federal poverty level (FPL). The table below shows the income range based on household size that you have to fall into to qualify for ACA health insurance subsidies in 2026.

Obamacare subsidy income limits for 2026

Household size |

Typical min. income

|

Typical max. income

|

|---|---|---|

| 1 person | $15,650 | $62,600 |

| 2 people | $21,150 | $84,600 |

| 3 people | $26,650 | $106,600 |

| 4 people | $32,150 | $128,600 |

| 5 people | $37,650 | $150,600 |

| 6 people | $43,150 | $172,600 |

| 7 people | $48,650 | $194,600 |

| 8 people | $54,150 | $216,600 |

What counts as income for ACA subsidies?

What counts as income

- Wages from your job

- Investment income

- Rental income

- Royalties

- Self-employment income

- Capital gains

- Retirement income

- Unemployment income

- Social Security payments

- Social Security Disability Insurance (SSDI)

What doesn't count as income

- Child support

- Child tax credits from the IRS

- Gifts

- Money from loans

- Supplemental Security Income (SSI)

- Disability payments for veterans

- Workers' compensation

Medicaid and subsidies

If you can get Medicaid because of your income, you can't get marketplace subsidies.

In most states, there's an overlap between Medicaid and subsidy qualifications.

- You can usually get Medicaid if you make less than about $22,025 per year as a single person ($45,540 per year for a family of four).

- The typical minimum income for subsidies is $15,650 per year for an individual ($32,150 per year for a family of four).

- If you're in the gap between $15,650 and $22,025 ($32,150 to $45,540 per year for a family of four), and you can get Medicaid, then you can't get subsidies. You can still buy a marketplace plan if you don't want Medicaid, but you'll have to pay full price.

Medicaid is harder to get in 10 states. In these states, you usually have to have a very low income and meet another requirement, like having a disability or being pregnant. You can probably get marketplace subsidies at the lower end of the income spectrum in these states.

Calculating your ACA subsidies

Before shopping for an ACA health insurance plan, you can estimate your health insurance costs by using the subsidy calculator or doing the math yourself. Knowing if you can get a subsidy and how much it will be can help you choose a plan that best fits your needs.

How much you might save depends on your income, your family size and the cost of what's called a Benchmark Silver plan where you live. When it comes to the amount of the subsidy you can get, the less you earn, the larger your subsidy.

1. Compare your income to the federal poverty level

- Start by figuring out how much you earn compared to the federal poverty level.

- For 2026 health insurance plans, you'll use your estimated 2026 income and compare that to the 2025 federal poverty level amounts.

- For example, if you're single with an income of $31,300 per year, you're earning twice the federal poverty level.

Alaska and Hawaii have different limits because they have higher costs of living.

Federal poverty level (FPL) for the continental U.S.

Alaska

Hawaii

Household size | Federal poverty level |

|---|---|

| 1 person | $15,650 |

| 2 people | $21,150 |

| 3 people | $26,650 |

| 4 people | $32,150 |

| 5 people | $37,650 |

| 6 people | $43,150 |

| 7 people | $48,650 |

| 8 people | $54,150 |

For a family of nine or more, add $5,500 for each extra person.

2. Determine the most you'll pay for insurance

The ACA limits the monthly price you pay for health insurance if you earn less than $62,600 per year as an individual ($128,600 per year for a family of four) in most states.

The highest amount you'll spend on a plan is a percentage of your income.

Single income

Income for a family of four

Income (single) | % of income you'll pay for health insurance |

|---|---|

| $15,650 | 2.10% |

| $23,475 | 4.19% |

| $31,300 | 6.60% |

| $39,125 | 8.44% |

| $46,950 | 9.96% |

| $62,600 | 9.96% |

For example, if you earn $23,475 per year and you're single, you won't pay more than about $984 per year, or $82 per month, for health insurance.

In some states, you might be able to get discounts with a higher income. For example, in New Jersey, you can get financial help from the state if you earn less than $93,900 per year ($192,900 for a family of four).

3. Find out the cost of a "Benchmark" Silver plan

- Your health insurance discount is tied to the cost of a "Benchmark Silver plan," which is the second-cheapest Silver plan in your area.

- You can view available quotes in the federal or state insurance exchange to find the Benchmark plan, or you can call the marketplace.

- HealthCare.gov can be reached at 800-318-2596. If your state uses a state marketplace site, check the website for a phone number.

4. Subtract how much you're expected to pay from the Benchmark rate

- If the amount you should pay for insurance is less than the cost of a Benchmark plan, your subsidy will be the difference between the two.

- For example, if the Benchmark Silver plan costs $3,000 a year and your income calculation means you should pay $1,000 for a plan, then you will get a subsidy of $2,000.

If your expected contribution for health insurance is more than the cost of a Benchmark plan, you won't get any health insurance subsidies. However, you can still enroll in full-priced plans.

Example: Income is twice the federal poverty level

A person earning $31,300 (twice the federal poverty level) is expected to spend 6.6% of their income toward a typical health insurance plan. That amounts to about $172 per month.

If the Benchmark Silver plan in the area costs $500 per month, that person would get a subsidy of $328 per month to cover the difference. The $328 subsidy can be used for any Bronze, Silver, Gold or Platinum plan.

When can you sign up for ACA subsidies?

You can sign up for an ACA subsidized health insurance plan each year during the annual open enrollment period between Nov. 1 and Jan. 15. But if you have a qualifying life event, you may be eligible for a special enrollment period, which would give you access to get coverage midyear.

Examples of qualifying events include:

- Loss of health care coverage

- Changes in household

- Changes in residence

How much does health insurance cost after ACA subsidies?

The average cost of a subsidized health insurance policy in the U.S. is an estimated $175 per month.

- How much you'll pay for health insurance is based on your income, your family size and where you live.

- You'll probably get smaller subsidies in 2026 because pandemic-era "enhanced subsidies" expired at the end of 2025.

However, many states have state-level discounts and programs that can make your health insurance even cheaper.

- For example, in New York, the average cost of health insurance after federal subsidies is $534 per month.

- But New York has what's called the "Essentials Plan," which gives you free health insurance coverage if you're single and make less than $39,900 per year in 2026.

Find Cheap Health Insurance in Your Area

Average cost of health insurance after subsidies

Location | Monthly rate |

|---|---|

| United States | $175 |

| Alabama | $121 |

| Alaska | $474 |

| Arizona | $190 |

| Arkansas | $208 |

| California | $261 |

| Colorado | $311 |

| Connecticut | $348 |

| Delaware | $265 |

| Florida | $118 |

| Georgia | $111 |

| Hawaii | $287 |

| Idaho | $252 |

| Illinois | $228 |

| Indiana | $174 |

| Iowa | $241 |

| Kansas | $166 |

| Kentucky | $228 |

| Louisiana | $159 |

| Maine | $337 |

| Maryland | $200 |

| Massachusetts | $239 |

| Michigan | $199 |

| Minnesota | $356 |

| Mississippi | $85 |

| Missouri | $173 |

| Montana | $307 |

| Nebraska | $270 |

| Nevada | $202 |

| New Hampshire | $254 |

| New Jersey | $229 |

| New Mexico | $269 |

| New York | $534 |

| North Carolina | $182 |

| North Dakota | $299 |

| Ohio | $182 |

| Oklahoma | $156 |

| Oregon | $359 |

| Pennsylvania | $235 |

| Rhode Island | $238 |

| South Carolina | $150 |

| South Dakota | $302 |

| Tennessee | $141 |

| Texas | $124 |

| Utah | $203 |

| Vermont | $461 |

| Virginia | $199 |

| Washington | $275 |

| Washington, D.C. | $346 |

| West Virginia | $252 |

| Wisconsin | $262 |

| Wyoming | $378 |

Rates after subsidies are estimates for a 40-year-old buying a Benchmark Silver plan. Only federal subsidies are represented. Many states have state subsidies that can lower the cost even more.

Between 2021 and 2025, you wouldn't have to pay more than 8.5% of your income for your monthly rate with a marketplace plan, regardless of how much you earned. Starting in 2026, you can't get federal subsidies if you make more than $62,600 per year as a single person ($128,600 for a family of four), even if the plan costs more than 8.5% of your income.

States with their own health insurance subsidies and programs

State | Type of assistance | Free or cheap? | Annual income limits |

|---|---|---|---|

| California | State subsidy | Cheaper rates | Between $23,475 and $25,823 as a single person |

| Colorado | State subsidy | Cheaper rates | Below $62,600 as a single person |

| Connecticut | State subsidy | Free Silver plan | Up to $27,388 as a single person |

| Maryland | State subsidy | Cheaper rates | Between $15,650 and $62,600 as a single person |

| Massachusetts | State subsidy | Free or cheaper rates | Between $15,650 and $62,600 as a single person |

| Minnesota | Basic Health Program | Free or cheaper plan | Between $21,597 and $31,300 as a single person |

| New Jersey | State subsidy | Cheaper rates | Up to $93,900 as a single person |

| New Mexico | State subsidy | Free or cheaper rates | Up to $62,600 as a single person |

| New York | Basic Health Program | Free plan | Below $39,900 as a single person |

| Oregon | Basic Health Program | Free plan | Between $21,597 and $31,300 as a single person |

| Vermont | State subsidy | Cheaper plan | Up to $46,960 as a single person |

| Washington | State subsidies | Cheaper rates | Up to $39,125 as a single person |

| Washington, D.C. | Basic Health Program | Free plan | Between $21,597 and $31,300 as a single person |

Income limits are rounded to the nearest dollar.

If you qualify for a rate subsidy, you may also be eligible for another type of health insurance discount that helps you pay for doctor visits and prescription drugs, called a cost-sharing reduction. You can only get cost-sharing reductions if you qualify and choose a Silver health plan.

Do I have to pay back subsidies?

No, you don't have to pay back health insurance subsidies that you qualify for.

But there may be an adjustment at tax time, when your actual income for the year is used to determine if you got subsidies that were too large or too small.

Most people get subsidies every month in the form of what are called "advance premium tax credits." Because these discounts are based on your estimated income for the year, the actual subsidy amount you are eligible for might be different once you know your actual income when you file your taxes.

- If you qualify for more subsidies than you got, you'll get the extra amount as a tax credit when you file income taxes.

- If you got higher subsidies than you were ultimately eligible for, then you will have to repay some or all of the money you got as a subsidy when you file your taxes.

If your actual income doesn't match your estimated income at tax time, you will have to repay the entire difference in your subsidy amount.

- Previously, if you had a lower income, you didn't always have to repay the full amount if you made more than you thought you would. There was a limit on the amount you had to pay back.

- However, a recent rule change means you have to pay back the full amount no matter how much you got.

- Starting with your 2026 income, if you make more than you thought you would, you have to repay the full difference between the subsidy you should have gotten and the amount you actually got.

How many people get subsidies?

In 2025, about 22.4 million people got subsidized plans from HealthCare.gov or state marketplaces.

The number of people with marketplace coverage grew steadily between 2020 and 2025. But so far, fewer people are getting Obamacare health insurance in 2026.

That's largely because the bigger "enhanced subsidies" expired at the end of 2025. The discounts on the marketplace in 2026 aren't as high, so some people are choosing to go without health insurance entirely to save money.

Obamacare enrollment with and without subsidies

Year | People with subsidized plans | People with unsubsidized plans |

|---|---|---|

| 2025 | 22.4 million | 1.9 million |

| 2024 | 19.7 million | 1.7 million |

| 2023 | 14.8 million | 1.6 million |

| 2022 | 13 million | 1.6 million |

| 2021 | 10.2 million | 1.9 million |

| 2020 | 9.6 million | 1.8 million |

Are $6,400 subsidies for health insurance real?

Health insurance subsidies are real, but the advertisements for $6,400 subsidies are scams.

These ads are scams to get you to share your personal info. They are also misleading about how the subsidy program works. Health insurance subsidy amounts vary by household, and you have to shop through the government marketplace to be eligible.

- Subsidy amounts change based on your income and location. The average health insurance subsidy is $550 per month, which is $6,600 per year. You may qualify for more or less. After subsidies, many people get free or cheap health insurance.

- You have to shop in the government-run marketplace to get subsidies. Health insurance subsidies are a government program, and you can only get them if you shop on a government website or with an insurance agent who's associated with the government.

- You'll never get a gift card or cash as a subsidy. Subsidies are applied to your monthly insurance bill, which could mean you'd only have to pay $25 per month for a $600 health insurance plan. You can also choose to get the lump sum of the subsidy as a discount when you file your taxes the following year.

- Claims that you must 'act now' are exaggerated. The subsidies won't expire or run out. The only dates you need to worry about are the open enrollment deadlines. You'll usually need to sign up for insurance by Jan. 15 to get subsidies for the year. You may also be able to sign up after that if you have special circumstances, such as moving or a change in family size.

- It will probably take longer than the 30 seconds advertised. You'll find out right away how much you'll qualify for in subsidies. But plan for about 10 to 30 minutes to complete the forms and choose a health insurance plan.

How to use ValuePenguin's ACA subsidy calculator

Step 1. Enter your ZIP code.

The ZIP in the example is for Austin, TX.

Step 2. Enter your estimated annual income.

The income in the example is $30,000.

Step 3. Click "Calculate."

Your subsidy amount displays in blue text.

In this example, the subsidy amount is $506 per month.

The calculator also shows your income as a percentage of the federal poverty level, the cost for a Silver plan after your subsidy and the full-price cost of a Silver plan.

In the example, the income is 192% of the federal poverty level. A Silver plan costs $661 per month at full price or $155 per month after the subsidy.

Frequently asked questions

Is Obamacare free?

Obamacare health insurance usually isn't free, and those who get subsidies typically pay an estimated average of $175 per month. Obamacare might be free if you don't earn much, as costs are on a sliding scale based on your income. And those with very low incomes might be eligible for free insurance through Medicaid instead.

What are the income limits for health insurance subsidies?

To qualify for health insurance subsidies, you'll typically need to earn between $15,650 and $62,600 as a single person or between $32,150 and $128,600 as a family of four.

Who is eligible for Obamacare?

Most people who don't have health insurance through their job can buy an insurance plan through HealthCare.gov or their state health insurance marketplace. Your income determines if you can get health insurance subsidies. Use a subsidy calculator to estimate your final cost for health insurance.

How much is Obamacare insurance?

The average cost of health insurance through Obamacare is $752 per month for a single person. For those with low to moderate incomes, subsidies can reduce the cost of health insurance, and those who qualify could pay an estimated average of $175 per month.

Methodology and sources

Costs and calculations are based on data from public use files (PUFs) on the Centers for Medicare & Medicaid Services (CMS) government website.

Subsidies

Rates after subsidies are estimates for a 40-year-old with a Benchmark Silver plan and are based on how subsidies were structured before 2021. Prices are calculated using KFF's rates for full-price Benchmark plans, federal poverty levels (FPLs), IRS rules about premium tax credits and Congressional reports about expanded tax credits. The total cost in the state uses calculated rates by income, which are weighted using CMS data on the incomes of those who purchased plans during 2024-2025 open enrollment. The median was used for each income range. Unknown incomes were excluded from the calculations. Incomes of 100% of the federal poverty line and 500% of the federal poverty line were assumed for enrollees who earn less than 100% FPL and more than 500% FPL, respectively. State subsidy info was excluded from the table about rates after subsidies.

Information about state subsidies, when available, was sourced from state marketplaces.

Other sources

Other sources include HealthCare.gov, CMS.gov, KFF and the U.S. Department of Health & Human Services.

About the Author

Senior Writer

Licensed Insurance Agent

Cate Deventer is a Senior Writer who specializes in health insurance, Medicare, auto and home insurance. She's been a licensed insurance agent since 2011.

She started her insurance career working as a customer service agent for State Farm. She later moved to an independent agency, where she worked with several insurance companies and hundreds of clients. She quoted policies, filed claims and answered insurance questions. In 2021, she pivoted her career and began writing about insurance for Bankrate. She moved to ValuePenguin in 2023 and began writing about health insurance and Medicare.

Cate has a passion for helping readers choose insurance to fit their needs. She enjoys knowing that her research and knowledge help people choose insurance products that make a positive difference in their lives.

How insurance helped Cate

Cate used her health insurance knowledge to navigate a surgery in 2023. Understanding how her policy worked let her focus on recovery instead of worrying about bills.

Expertise

- Health insurance

- Medicare & Medicaid

- Auto insurance

- Home insurance

- Life insurance

Credentials

- Licensed Life, Accident & Health Insurance Agent

- Licensed Property & Casualty Insurance Agent

Referenced by

- CBS

- NBC

- Wall Street Journal

Education

- BA, Theatre, Purdue University

- BA, English, Indiana University

Editorial note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.