Average Cost of a Vacation and How Travel Habits are Changing

Editorial Note: The content of this article is based on the author’s opinions and recommendations alone. It may not have been reviewed, approved or otherwise endorsed by the credit card issuer. This site may be compensated through a credit card issuer partnership.

Terms apply to American Express benefits and offers. Visit americanexpress.com to learn more. Citi is an advertising partner.

Vacation spending is equal to about 2% of the total budgets of all U.S. households annually; however, only some households report these costs. When it comes to pleasure trips, it’s a tale of two Americas: those who hardly spend a night away from home; and those who drop an average of $4,700 on vacations each year. Below we'll take a look at how much Americans reported paying in the Consumer Expenditure Survey for their vacations in total and by individual categories.

Average Cost of a Vacation

The cost of traveling for pleasure can vary wildly, depending on if you’re packing up the kids in the minivan for a week at grandma’s over summer vacation; hopping a bus solo to visit an old college buddy for the weekend; or herding your family onto a long-haul flight for a month in Bora Bora. The table below shows the cost of a vacation averaged across all respondents. This average spans a wide range of vacations, from those who make a short and frugal road trip to those who fly across the country to expensive cities.

Average Vacation Expenses per Trip | Domestic Trip (4 nights) | International Trip (12 nights) |

|---|---|---|

|

Transportation | $224 | $1,755 |

|

Lodging | $150 | $683 |

|

Food/Alcohol | $155 | $520 |

|

Entertainment | $52 | $293 |

|

Total | $581 | $3,251 |

|

Cost-per-day | $144 | $271 |

Of course, not all vacationers incurred each expense. For example, someone who stayed with friends on vacation would have a $0 cost for their lodging. Vacation expenditures also vary by age group, with near-retirees spending nearly four times as much on trips, on average, compared to young people under age 25. A family that vacations might travel internationally once a year, and also take a few domestic trips. Or, they might stay within the U.S., but spend a combined total of 30 days away from home, spread over various places to visit.

Costs have also risen in the past decade. For a typical trip within the U.S., people spend an average of about $581 and go away for about four nights (the cost of a domestic vacation was less than $500 back in 2005). Their travel costs per day are now about $144. Across all people who took an international vacation in 2013, the average cost came out to be $3,250 for a typical 12 to 13 night trip abroad. That means spending about $250 to $271 per night. This amount has risen considerably in recent years, from $2,000 in 2005. Rising costs are just one other reason that you might consider travel insurance to reduce the impact of financial losses on the road.

Transportation: Getting There is Half the Budget

The typical vacationing U.S. family spends about 44% of their travel funds getting to, from, and around their destinations. They spend an average of more than $2,100 each year on the transportation costs for their vacations. This figure spans a variety of different modes of transportation, ranging from driving a family's own car to taking cruises. The table below breaks down each type, and provides the average expenditure for households that report incurring them.

Average Annual Transportation Expenses, If Incurred By Vacationing Households | |

|---|---|

|

Airline fares | $3,304 |

|

Buses between cities | $252 |

|

Trains between cities | $521 |

|

Local transportation on out-of-town trips | $202 |

|

Taxis/car service on out-of-town trips | $119 |

|

Ships | $2,456 |

|

Gas for out-of-town trips | $669 |

|

Parking for out-of-town trips | $172 |

|

Tolls for out-of-town trips | $71 |

Flying

These costs are much steeper when a family’s summer vacation involves an airport. Those who fly (only about 10% of Americans buy a plane ticket in a given quarter), spend more than $3,304 on airfare annually on average. Two ways to stretch your vacation dollars further are to utilize frequent flyer miles (which savvy travelers can augment with airline miles credit cards), and to plan ahead. You’re more likely to get cheap flights if you buy them about seven weeks before your trip; although for travel during the busy summer season, you’re better off booking about 11 weeks (almost three months) before your travel dates if you’re hoping for a low cost airfare.

Since most international trips from the U.S. - except a portion to Canada and Mexico - require a plane ticket, transportation costs eat up an even larger proportion of the budget, about 54%. Transportation is about 39% of the overall cost of domestic vacation trips.

Cars & Other

About 6% of families travel by train, bus or ship on vacation. Some 11 million Americans take a cruise each year. 6% of travelers end up paying for local transportation, like taxis, as part of their yearly vacation budget.

Of course, the U.S. is car country, and with the average cost of gas below $3 per gallon in 2015, American families will keep taking road trips. About 21% of households leave their towns on four wheels in a typical quarter. Most families own or lease the vehicles they use for these trips, but about 2% rent a car or truck on vacation and spend an average of $1,223. Despite their cultural prominence, only 0.5% of Americans travel via RV (recreational vehicle). For road warriors of all sorts, parking fees and tolls may take another bite out of the travel budget.

Lodging: The Cost of A Good Night’s Sleep, Away from Home

When Americans travel domestically, they often stay with family and friends. Just 42% of those who take trips report lodging costs. Meanwhile, for those who travel internationally, more than 60% pay for accommodations. Those who do pay for lodging when they travel spend an average of $2,158 on it over the course of a year. Lodging costs are about 26% of total travel expenditures for domestic trips, and 21% for international trips.

Within the U.S., the average hotel room costs $141 per night, according to an analysis of data from hotels.com. Other studies show that renting a room in someone else’s home with a service like Airbnb is generally cheaper than staying at a hotel. IN some cases, renting an entire home may be less or more than a hotel, depending on the city. Some credit card rewards can be applied towards hotel stays and other travel perks to squeeze more out of a vacation.

Many U.S. families have found other ways to sleep cheaper, including things like RVs, campsites or longer term rental homes. They report paying an average of about $87 per night for lodging on their domestic trips, and just a dollar or two more per night when traveling abroad.

The Cost of Food on Vacation

Overall, Americans spend an average of $33 per day on food when on a vacation within the U.S. In aggregate, more than 80% of that amount is spent in restaurants. Each trip day, vacationers spend about $27 at restaurants, and about $6 on food they prepare themselves. On international trips, people spend just a little bit more on average, about $35 per day; with nearly 90% of those funds devoted to restaurant meals.

Average Food Costs Per Vacation | Domestic Trip (4 nights) | International Trip (12 nights) |

|---|---|---|

|

Food prepared at restaurants | $108 | $378 |

|

Food prepared by vacationer | $24 | $42 |

Many people look forward to vacation as a time to kick back and drink alcohol with abandon. Those who indulge while travelling spend about $380 on the beer, wine and liquor they consume. Only 12% of Americans report purchasing alcohol while on trips, though 18% pay for drinks at restaurants and bars, either in their hometowns or while they’re away. Food plus alcohol take up about 16% of the budget for an American’s international trips; and about 27% of their domestic trips.

Entertainment Costs While On Vacation

Many people use vacation days for cultural experiences or special activities. People who travel end up spending about 9% of their budget on entertainment--that’s about $52, on average, for a domestic trip, and $293 while abroad. Movies and sporting events are popular diversions when people are away from home. Those who get tickets to watch athletic events while on vacation pay about $180 annually. Those who play sports, like golf, while on vacation, spend about $640 per year for the privilege.

Average Entertainment Costs, If Incurred by Vacationing Households | |

|---|---|

|

Participant Sports | $640 |

|

Movies & other admissions | $541 |

|

Tickets to Sporting events | $180 |

|

Other Recreation Expenses | $250 |

|

Other entertainment services | $250 |

Different destinations can require a wide range of entertainment fees. Some beaches are absolutely free for families who want to sit, sun and swim all day long, making them great summer vacation spots. Museum tickets can cost from zero to upwards of twenty-five dollars. A one-day ticket to Disney World’s Magic Kingdom can cost an adult $105 plus tax.

Research your destination in advance and look for package deals for the top vacation spots in the U.S. and abroad. A family may be able to get a cheap trip to Disney by buying a package including food and resort costs. They can also purchase multi-day passes to all of Disney’s theme parks to get the per-day cost down to about $63 a day for adults (even less for children.)

A museum pass in Paris lets you bop in and out of more than 50 of the city’s museums and monuments, including the Louvre, the Château de Versailles and the Musée D’Orsay for less than 12 to 21 euro per day (depending on how many days it covers). City passes bundle the attractions of many popular vacation destinations for an appreciable discount. For example, in San Francisco, you can use a City Pass to travel on the muni or cable car, visit the California Academy of Sciences, an aquarium, the art museum, and take a bay cruise for about $94, saving about $74 over having paid all the separate entrance fees.

Have Americans lost their love of adventure? Do they no longer have the discretionary income for vacations, given the rise in costs of housing, education and healthcare? Whatever the explanation, the drop off can’t be good for the travel and tourism industry, which employs nearly 6% of American workers.

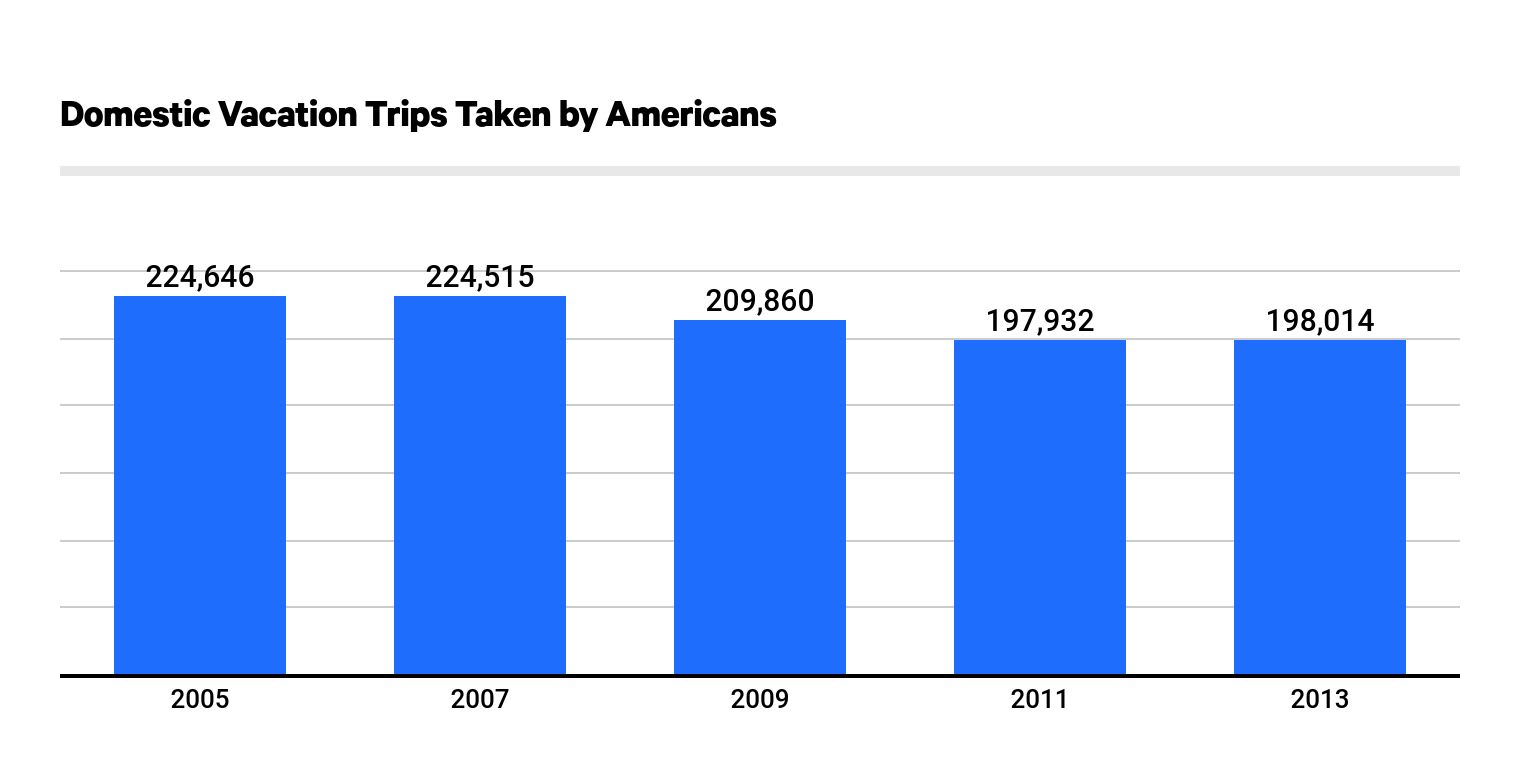

Americans are Taking Fewer Trips

Between 2005 and 2013, the most recent year for which data is available from the Consumer Expenditure Survey, the number of pleasure trips taken by members of U.S. households dropped dramatically. In 2013, there were 30% fewer vacation trips taken domestically, compared to 2005.

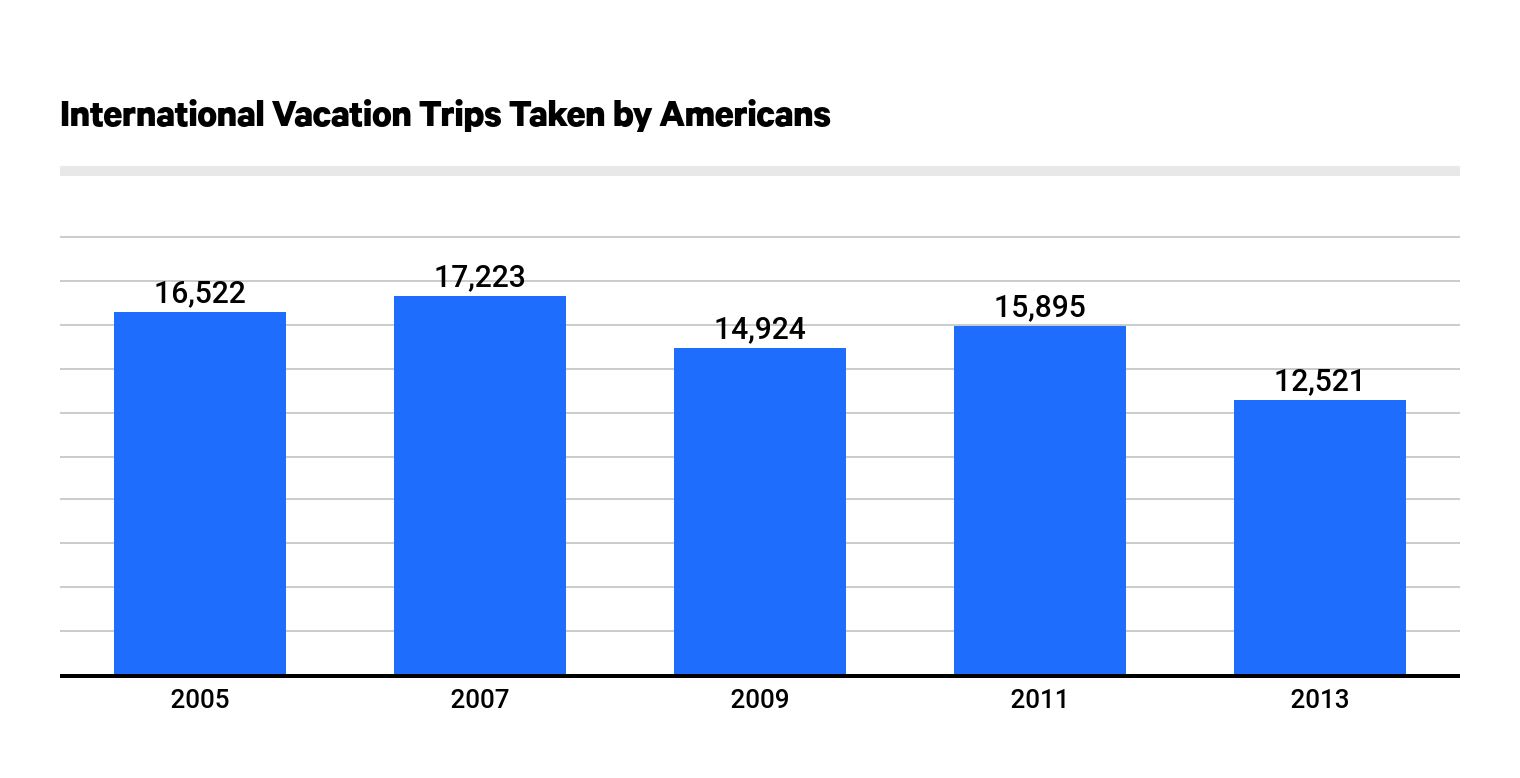

While domestic numbers have declined more gradually, international trip trends have fluctuated in the past eight years. Nevertheless, overall trip numbers abroad still registered a drop, with 36% fewer international trips in 2013 compared to 2005.

Have Americans lost their love of adventure? Do they no longer have the discretionary income for vacations, given the rise in costs of housing, education and healthcare? Whatever the explanation, the drop off can’t be good for the travel and tourism industry, which employs nearly 6% of American workers.

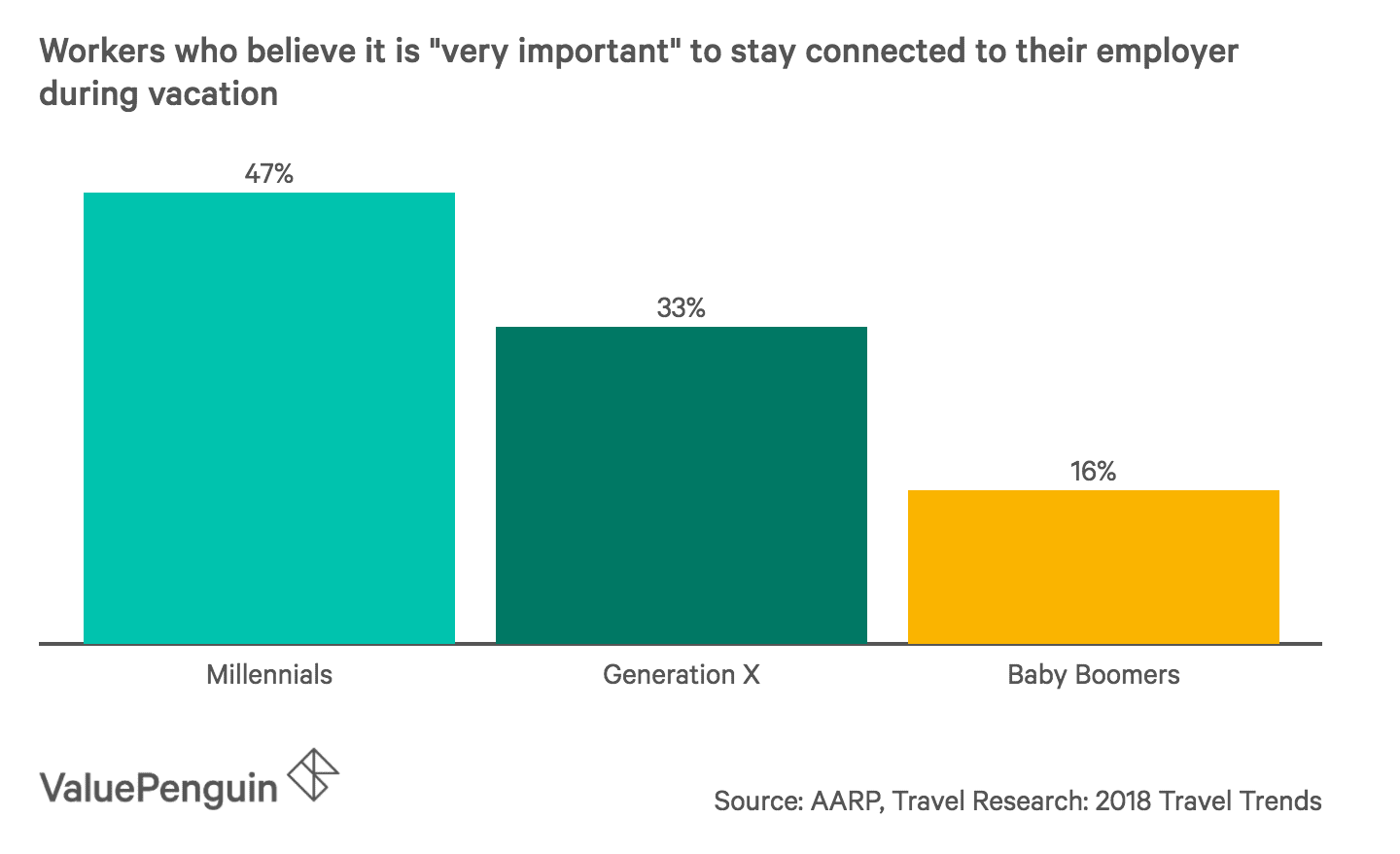

Millennials finding a way to go on vacation and work

A 2018 report by the AARP on Baby Boomer travel trends revealed a Millennials have a bit of a different mindset: they won't stop working, even when on vacation.

According to the study, which polled 1,728 individuals 20-years-old or older, 47% of Millennials (ages 20–36) believe it is "extremely" or "very important" to stay connected to work while on vacation, compared to just 33% of Generation X and 16% of Baby Boomers.

The study suggests that even those who don't believe staying connected is important may feel pressured into being on-call. Nearly three-quarters of Millennials expect to bring work along with them on a trip, compared to 65% of Gen Xers and just 56% of Baby Boomers. Another study, conducted by Wrike, the project management platform used by such companies as Airbnb, revealed similar findings. In their survey of 1,137 adults (between the ages of 18-64), 42% of Millennial respondents said they intended to work on vacation, while just 28% of Gen-Xers and Boomers did, collectively. So even when Millennials do make use of their vacation days, they feel more chained to their desks than other generations—even if that chain reaches all the way to Bali.

About the Author

Senior Insurance Analyst

Sterling Price is a former senior research analyst at ValuePenguin specializing in health and life insurance. He graduated from Syracuse University with a bachelors degree in Finance and Accounting and has previous experience as a licensed life insurance representative.

These responses are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser's responsibility to ensure all posts and/or questions are answered.

Advertiser Disclosure: The products that appear on this site may be from companies from which ValuePenguin receives compensation. This compensation may impact how and where products appear on this site (including, for example, the order in which they appear). ValuePenguin does not include all financial institutions or all products offered available in the marketplace.

How We Calculate Rewards: ValuePenguin calculates the value of rewards by estimating the dollar value of any points, miles or bonuses earned using the card less any associated annual fees. These estimates here are ValuePenguin's alone, not those of the card issuer, and have not been reviewed, approved or otherwise endorsed by the credit card issuer.

Example of how we calculate the rewards rates: When redeemed for travel through Ultimate Rewards, Chase Sapphire Preferred points are worth $0.0125 each. The card awards 2 points on travel and dining and 1 point on everything else. Therefore, we say the card has a 2.5% rewards rate on dining and travel (2 x $0.0125) and a 1.25% rewards rate on everything else (1 x $0.0125).