Best and Cheapest Home Insurance in Washington State for 2026

Grange has the best home insurance for most people in Washington. A policy with $350,000 in dwelling coverage costs an average of $1,030/yr. | ||

The average rate for home insurance in Washington is $1,560/yr. That's 35% cheaper than the national average. | ||

Homeowners in Seattle pay an average of $1,475/yr for $350,000 in dwelling coverage. |

Find Cheap Home Insurance Quotes in Washington

Who sells the best home insurance in Washington?

What company has the cheapest home insurance in Washington?

Grange has the cheapest home insurance in Washington for most people.

Find Cheap Home Insurance Quotes in Washington

Best cheap home insurance in Washington by dwelling amount

$200,000

$350,000

$500,000

$1 million

Company | Annual rate | ||

|---|---|---|---|

| Grange | 5.0 out of 5 | $627 | |

| Mutual of Enumclaw | 4.5 out of 5 | $647 | |

| Pemco | 3.8 out of 5 | $764 |

| State Farm | 3.5 out of 5 | $874 | |

| Farmers | 3.3 out of 5 | $965 | |

| Nationwide | 4.3 out of 5 | $1,022 | |

| Allstate | 3.5 out of 5 | $1,246 | |

| PURE | 2.3 out of 5 | $1,405 |

| Country Financial | 2.5 out of 5 | $1,944 | |

| USAA | 4.0 out of 5 | $1,080 | |

Key takeaways

-

Home insurance rates in Washington have gone up by about 58% since 2021. That outpaces the national average five-year increase of about 48%.

- Country Financial has had the lowest rate increase, but a policy still costs a third more now than five years ago.

- Mutual of Enumclaw has increased rates the most in recent years. A policy from the company costs more than twice as much now as it did in 2021.

- Homeowners in Washington should make sure their policies cover them for wildfire damage. Getting coverage for earthquakes and flooding is a good idea, too.

Best home insurance in Washington for most people: Grange

-

Annual cost$1,030Average rate for a $350,000 home

-

Monthly cost$86Average rate for a $350,000 home

-

Customer complaints Low

Best home insurance in Washington for new homes: Pemco

-

Annual cost$1,100Average rate for a $350,000 home

-

Monthly cost$92Average rate for a $350,000 home

-

Customer complaints Low

Best home insurance in Washington for bundling: State Farm

-

Annual cost$1,189Average rate for a $350,000 home

-

Monthly cost$99Average rate for a $350,000 home

-

Customer complaints Average

What are the top-rated home insurance companies in Washington?

Grange and Mutual of Enumclaw have the best-rated homeowners insurance in Washington state.

Both companies get very few complaints about their home insurance, according to the National Association of Insurance Commissioners (NAIC). This means people are usually happy with the service they get from Grange and Mutual of Enumclaw.

Both Grange and Mutual of Enumclaw also have cheap rates and good home insurance coverage options.

Company |

Rating

|

Complaints

|

|---|---|---|

| Grange | 5.0 out of 5 | Low |

| Mutual of Enumclaw | 4.5 out of 5 | Low |

| Nationwide | 4.3 out of 5 | Low |

| USAA | 4.0 out of 5 | Low |

| PEMCO | 3.8 out of 5 | Low |

| Allstate | 3.5 out of 5 | Average |

| State Farm | 3.5 out of 5 | Average |

| Chubb | 3.3 out of 5 | Low |

| Farmers | 3.3 out of 5 | Low |

| Country Financial | 2.5 out of 5 | Low |

| PURE | 2.3 out of 5 | Low |

What's the average home insurance cost in Washington?

Home insurance in Washington costs $1,560 per year, on average, for a policy with $350,000 in dwelling coverage.

That's 35% cheaper than the national average home insurance rate of $2,395 per year. Washington has the 12th-cheapest average home insurance rates in the country.

Average cost of home insurance in WA

Dwelling coverage | Average rate |

|---|---|

| $200,000 | $1,057 |

| $350,000 | $1,560 |

| $500,000 | $2,132 |

| $1,000,000 | $3,880 |

Home insurance in Washington is cheaper than it is in Idaho. In Idaho, homeowners pay an average of $1,759 per year for $350,000 in dwelling coverage.

But Oregon's home insurance rates tend to be cheaper, at an average of $1,353 per year for $350,000 in dwelling coverage.

In general, rates in the Pacific Northwest are cheaper than in many other states, especially states in the Plains. Washington and the surrounding areas have a lower risk for home damage than in other areas of the country. The state rarely has tornadoes or hail and usually has a lower risk for wind damage compared to other areas of the country.

Cost of Washington home insurance by city

Home insurance in Seattle, WA, costs $1,475 per year, on average.

That's about 5% cheaper than the state average of $1,560 per year. Rates in Spokane are closer to the state average, with a $350,000 policy coming in at $1,573 per year, on average.

Buena, in south central Washington, has the most expensive average rate in the state, at $2,196 per year. Bangor Base has the cheapest average rate, at $1,370 per year. In general, rates tend to be more expensive in the middle of the state, to the east of the Cascade Range.

Find Cheap Home Insurance Quotes in Washington

Cost of WA home insurance by city

City | Average rate | Cheapest company | Cheapest rate |

|---|---|---|---|

| Aberdeen | $1,477 | Grange | $813 |

| Acme | $1,440 | Grange | $813 |

| Addy | $1,684 | Grange | $1,048 |

| Adna | $1,504 | Grange | $813 |

| Ahtanum | $1,911 | Pemco | $1,166 |

| Airway Heights | $1,598 | Mutual of Enumclaw | $995 |

| Albion | $1,630 | Grange | $1,048 |

| Alderton | $1,594 | Grange | $1,026 |

| Alderwood Manor | $1,451 | Grange | $970 |

| Algona | $1,546 | Grange | $1,009 |

| Allyn | $1,476 | Grange | $813 |

| Almira | $1,773 | Mutual of Enumclaw | $997 |

| Amanda Park | $1,509 | Grange | $813 |

| Amboy | $1,571 | Grange | $1,106 |

| Ames Lake | $1,464 | Mutual of Enumclaw | $871 |

| Anacortes | $1,442 | Grange | $813 |

| Anatone | $1,760 | Grange | $1,048 |

| Anderson Island | $1,497 | Mutual of Enumclaw | $952 |

| Appleton | $1,868 | Mutual of Enumclaw | $1,100 |

| Ardenvoir | $1,773 | Mutual of Enumclaw | $1,079 |

| Ariel | $1,493 | Grange | $813 |

| Arlington | $1,537 | Pemco | $1,054 |

| Arlington Heights | $1,537 | Pemco | $1,054 |

| Artondale | $1,480 | Mutual of Enumclaw | $1,021 |

| Ashford | $1,634 | Grange | $1,026 |

| Asotin | $1,708 | Grange | $1,048 |

| Auburn | $1,559 | Grange | $1,009 |

| Bainbridge Island | $1,433 | Grange | $813 |

| Bangor Base | $1,370 | Grange | $813 |

| Barberton | $1,527 | Grange | $1,106 |

| Baring | $1,602 | Mutual of Enumclaw | $954 |

| Battle Ground | $1,524 | Grange | $1,106 |

| Bay Center | $1,494 | Grange | $813 |

| Bay View | $1,449 | State Farm | $977 |

| Beaver | $1,450 | Grange | $813 |

| Belfair | $1,443 | Grange | $813 |

| Bellevue | $1,481 | Mutual of Enumclaw | $966 |

| Bellingham | $1,440 | Grange | $813 |

| Belmont | $1,754 | Mutual of Enumclaw | $1,033 |

| Benge | $1,769 | Grange | $1,048 |

| Benton City | $1,873 | Mutual of Enumclaw | $1,090 |

| Bethel | $1,447 | Grange | $813 |

| Beverly | $1,798 | Pemco | $1,189 |

| Bickleton | $1,741 | Pemco | $1,169 |

| Bingen | $1,657 | Grange | $813 |

| Birch Bay | $1,442 | Grange | $813 |

| Black Diamond | $1,526 | Mutual of Enumclaw | $965 |

| Blaine | $1,442 | Grange | $813 |

| Blakely Island | $1,470 | Grange | $813 |

| Bonney Lake | $1,598 | Mutual of Enumclaw | $990 |

| Bothell | $1,493 | Grange | $1,003 |

| Bothell East | $1,501 | Grange | $1,035 |

Rates are for a policy with $350,000 of dwelling coverage.

What home insurance coverage do you need in Washington?

Common natural disasters in Washington state include wildfires, earthquakes and flooding. Home insurance sometimes covers wildfire and earthquake damage, but you may need to buy a separate policy if you're in a particularly high-risk area. Home insurance almost never covers flood damage.

Does Washington home insurance cover fire damage?

Fortunately, most homeowners insurance policies cover damage from wildfires. However, if you live in a high-risk area, you may have a hard time finding an affordable policy. If that's the case, you may need to buy a more expensive type of home insurance as a last resort, called a FAIR plan policy.

These policies come from insurance companies, but they're backed by the state government. You can get FAIR coverage if you're having a hard time getting regular homeowners insurance.

**Nearly 60,000 homes in Washington have a moderate or high risk for wildfire damage, according to Cotality. Homes around the Cascade Mountains and in the northeastern part of the state have the highest risk.

Does Washington home insurance cover earthquakes?

Home insurance sometimes covers earthquake damage but only if you have an add-on to your coverage. Basic policies don't automatically cover earthquakes. And if you live in a high-risk area, you may need a separate policy.

If you live west of the Cascade Mountains or in south central Washington, you're at higher risk for earthquakes compared to the rest of the state. That means you should consider getting earthquake insurance if your own savings wouldn't cover the cost of repairing or rebuilding your house after a major earthquake.

Washington residents who live east of the mountains, such as those in Spokane, have less to worry about, although they're not entirely free from risk.

Does Washington home insurance cover flood damage?

Home insurance almost never covers flood damage. You need to buy a separate flood insurance policy to have coverage for flood damage. You can get a policy from the National Flood Insurance Program (NFIP) or from some private insurance companies.

Many areas of Washington are at a higher risk for flooding, including the Puget Sound area. Since 2015, the NFIP has paid more than $75 million in flood claims in Washington state.

How to save money on home insurance in WA

To find the best and cheapest home insurance policy for you, compare quotes, bundle your policies and think about increasing your deductible.

Every insurance company has its own rates, which means you could save just by switching companies. In Washington, there's an $1,800 difference between the cheapest and most expensive companies for $350,000 in dwelling coverage. | |

Bundling your policies is one of the easiest ways you can save. Most companies offer large discounts when you buy both your auto and home insurance together. Plus, bundling with one company can make your policies easier to manage. | |

Your deductible is the amount you pay when you file a claim. If you're willing to pay more by having a bigger deductible, you can get a lower rate. Just make sure you choose a deductible you can afford to pay. If it's too high, you could struggle to pay it if you file a claim. |

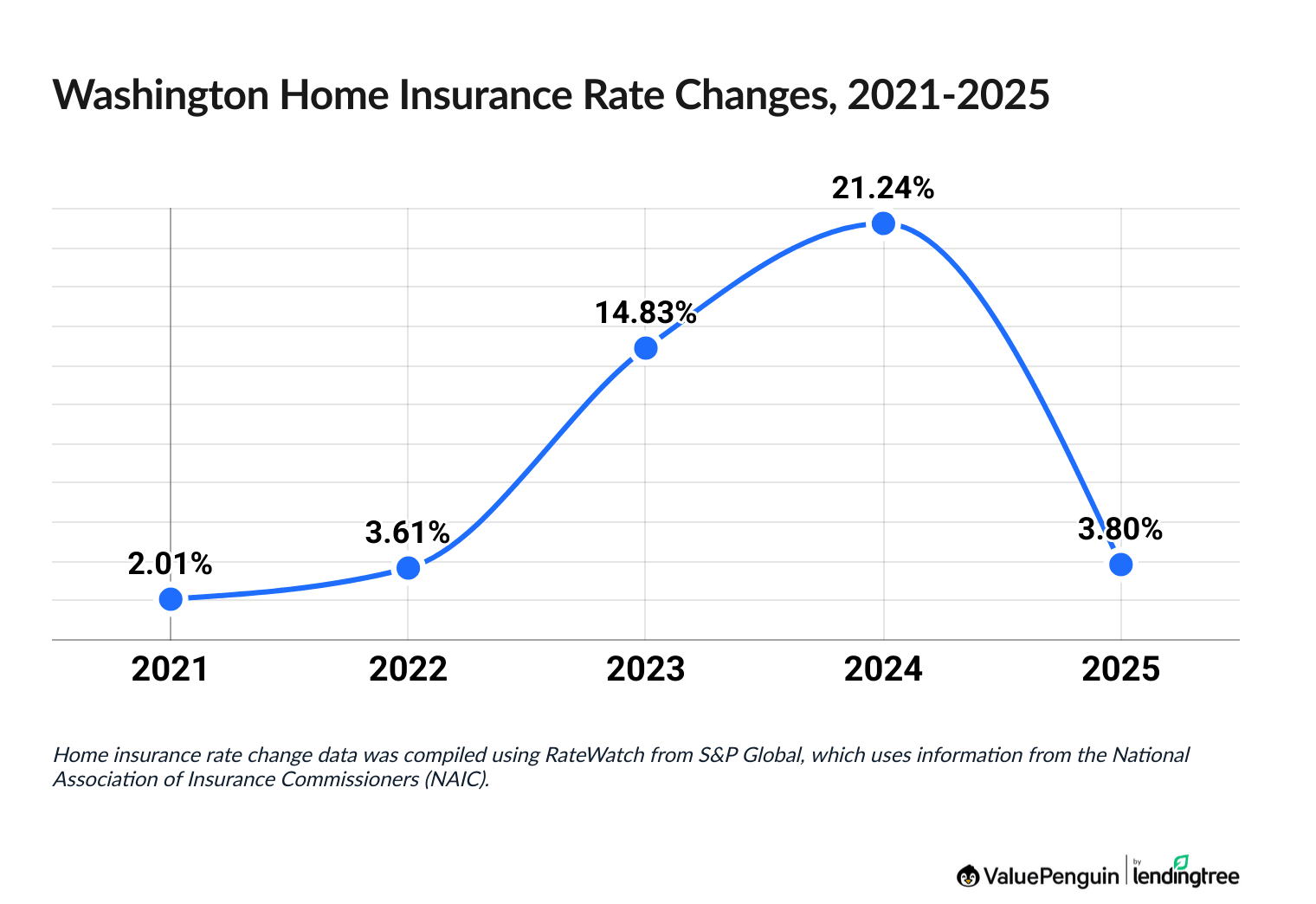

Are Washington home insurance rates going up?

Home insurance rates are up 58% in Washington since 2021.

That's quite a bit higher than the national average increase of about 48% over the last five years. The biggest increase in Washington was in 2024, when rates jumped by more than 21%.

Washington home insurance rate changes between 2021 and 2025

Year | Avg. rate increase |

|---|---|

| 2021 | 2.01% |

| 2022 | 3.61% |

| 2023 | 14.83% |

| 2024 | 21.24% |

| 2025 | 3.80% |

Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

Mutual of Enumclaw has raised its rates more than any other insurance company in recent years, with policy costs now more than double what they were in 2021.

Country Financial has seen the smallest increase, but its policies are still about 34% more expensive than they were five years ago.

Frequently asked questions

Which company has the best home insurance in Washington?

Grange sells the best home insurance policies for most people in Washington because of its cheap rates and excellent customer service. Other good options include Pemco for new homes and State Farm if you want to bundle auto and home insurance policies.

What is the average cost of homeowners insurance in Washington?

On average, home insurance in Washington costs $1,560 per year for a policy with $350,000 in dwelling coverage. That's the 12th-cheapest rate in the country and 35% cheaper than the national average, which is $2,395 per year.

Do I need home insurance in Washington?

You aren't legally required to have home insurance in Washington, but if you have a mortgage, your lender will very likely require that you have a policy. Even if your home is paid in full, you should probably have insurance. That way, if your home is damaged, you're protected from the full cost of repairs.

Methodology

To find the best homeowners insurance in Washington state, ValuePenguin collected quotes from the 11 of the top companies across 617 residential ZIP codes in the state. Rates are for a 45-year-old married man with no home insurance claims. The quotes are for a 44-year-old home with 2,185 square feet, which is a representation of the average home in Washington. New home data is for a home built in 2025.

The quotes are for policies with the following coverage limits:

- Dwelling coverage: $200,000, $350,000, $500,000 or $1 million

- Personal liability: $100,000

- Medical payments: $1,000

- Deductible: $1,000

Insurance rate data came from Quadrant Information Services. Quadrant's rates were taken from public insurance company filings and should only be used for comparative purposes. Your own quotes will be different.

ValuePenguin's company ratings use average rates, coverages, discounts, complaint data from the National Association of Insurance Commissioners (NAIC) and the J.D. Power customer satisfaction and claims satisfaction surveys.

Sources:

About the Author

Senior Writer

Licensed Insurance Agent

Cate Deventer is a Senior Writer who specializes in health insurance, Medicare, auto and home insurance. She's been a licensed insurance agent since 2011.

She started her insurance career working as a customer service agent for State Farm. She later moved to an independent agency, where she worked with several insurance companies and hundreds of clients. She quoted policies, filed claims and answered insurance questions. In 2021, she pivoted her career and began writing about insurance for Bankrate. She moved to ValuePenguin in 2023 and began writing about health insurance and Medicare.

Cate has a passion for helping readers choose insurance to fit their needs. She enjoys knowing that her research and knowledge help people choose insurance products that make a positive difference in their lives.

How insurance helped Cate

Cate used her health insurance knowledge to navigate a surgery in 2023. Understanding how her policy worked let her focus on recovery instead of worrying about bills.

Expertise

- Health insurance

- Medicare & Medicaid

- Auto insurance

- Home insurance

- Life insurance

Credentials

- Licensed Life, Accident & Health Insurance Agent

- Licensed Property & Casualty Insurance Agent

Referenced by

- CBS

- NBC

- Wall Street Journal

Education

- BA, Theatre, Purdue University

- BA, English, Indiana University

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.