The Best and Cheapest Home Insurance Companies in Vermont (2026)

Vermont Mutual has the cheapest home insurance rates in Vermont, at $533 per year.

Find Cheap Home Insurance Quotes in Vermont

Best Cheap Home Insurance in Vermont

To help Vermont homeowners find the best cheap homeowners insurance, ValuePenguin editors analyzed thousands of quotes and evaluated customer service ratings from the largest home insurance companies in the state.

Cheapest VT home insurance companies

Vermont Mutual offers the cheapest homeowners insurance quotes in Vermont.

A policy from Vermont Mutual costs $533 per year for $350,000 of dwelling coverage. That's $396 per year less than the state average.

Cheapest insurance companies

Find Cheap Home Insurance Quotes in Vermont

Concord also offers cheap insurance, at $558 per year for $350,000 of dwelling coverage. That's $370 less per year than the Vermont average.

Cheap Vermont home insurance quotes

$200,000

$350,000

$500,000

$1 million

Company | Annual rate | ||

|---|---|---|---|

| Vermont Mutual | 4.0 out of 5 | $367 |

| Allstate | 2.5 out of 5 | $477 | |

| Concord | 4.5 out of 5 | $485 |

| Frankenmuth | 4.5 out of 5 | $500 | |

| State Farm | 4.5 out of 5 | $586 | |

| Travelers | 3.0 out of 5 | $636 | |

| Union Mutual | 2.0 out of 5 | $751 |

| MMG | 2.0 out of 5 | $791 |

| Farmers | 2.5 out of 5 | $972 | |

Stars in this table represent ratings specific to home insurance.

What home insurance do I need in VT?

Vermont winters can be very cold, with average temperatures ranging from 20 to 30 degrees.

These cold temperatures can lead to heavy snowfall and ice, which can damage homes and other structures. Fortunately, homeowners insurance typically covers damage from snow and ice as well as frozen pipes.

Best Vermont home insurance for most people: Vermont Mutual

-

Cost$533/yrThis analysis used home insurance quotes for hundreds of ZIP codes across Vermont. Read our methodology.

Best for extra protection in VT: Concord

-

Cost$558/yrThis analysis used home insurance quotes for hundreds of ZIP codes across Vermont. Read our methodology.

Best for bundling home in Vermont: State Farm

-

Cost$828/yrThis analysis used home insurance quotes for hundreds of ZIP codes across Vermont. Read our methodology.

Average cost of Vermont homeowners insurance

The average cost of homeowners insurance in Vermont is $929 per year.

That makes Vermont the second-cheapest state in the country for homeowners insurance.

Dwelling coverage | Annual cost |

|---|---|

| $200,000 | $618 |

| $350,000 | $929 |

| $500,000 | $1,262 |

| $1,000,000 | $2,191 |

Vermont homeowners insurance is fairly similar to its neighboring states. Maine is the third-cheapest state in the country, with an average rate of $977 per year. In New Hampshire, homeowners insurance costs an average of $1,002 per year.

Vermont insurance rates by city

Winooski, a suburb of Burlington, is the cheapest city for home insurance in Vermont.

Home insurance in Winooski costs an average of $831 per year.

East Poultney, a village just east of the New York border, is the most expensive city for home insurance in Vermont. A policy in East Poultney costs around $994 per year, which is $163 per year more than coverage in Winooski.

Average cost of Vermont homeowners insurance by city

City | Annual rate | % from avg |

|---|---|---|

| Adamant | $905 | -2% |

| Albany | $927 | 0% |

| Alburgh | $939 | 1% |

| Arlington | $940 | 1% |

| Ascutney | $970 | 5% |

| Averill | $957 | 3% |

| Bakersfield | $932 | 0% |

| Barnet | $908 | -2% |

| Barre | $889 | -4% |

| Barton | $927 | 0% |

| Beebe Plain | $964 | 4% |

| Beecher Falls | $918 | -1% |

| Bellows Falls | $963 | 4% |

| Belmont | $970 | 4% |

| Belvidere Center | $947 | 2% |

| Bennington | $963 | 4% |

| Benson | $951 | 2% |

| Bethel | $932 | 0% |

| Bomoseen | $958 | 3% |

| Bondville | $956 | 3% |

| Bradford | $913 | -2% |

| Brandon | $942 | 1% |

| Brattleboro | $963 | 4% |

| Bridgewater | $938 | 1% |

| Bridgewater Corners | $941 | 1% |

| Bridport | $925 | 0% |

| Bristol | $900 | -3% |

| Brookfield | $914 | -2% |

| Brownsville | $964 | 4% |

| Burlington | $882 | -5% |

| Cabot | $911 | -2% |

| Calais | $925 | 0% |

| Cambridge | $867 | -7% |

| Cambridgeport | $958 | 3% |

| Canaan | $921 | -1% |

| Castleton | $958 | 3% |

| Cavendish | $960 | 3% |

| Center Rutland | $955 | 3% |

| Charlotte | $837 | -10% |

| Chelsea | $916 | -1% |

| Chester | $970 | 5% |

| Chittenden | $957 | 3% |

| Colchester | $871 | -6% |

| Concord | $907 | -2% |

| Corinth | $909 | -2% |

| Craftsbury | $910 | -2% |

| Craftsbury Common | $921 | -1% |

| Cuttingsville | $967 | 4% |

| Danby | $979 | 5% |

| Danville | $905 | -3% |

| Derby | $939 | 1% |

| Derby Line | $937 | 1% |

Rates are for a policy with $350,000 of dwelling coverage.

Top home insurance companies in Vermont

Concord is the best-rated home insurance company in Vermont.

Concord has great customer service reviews, lots of policy add-ons and affordable quotes.

Best Vermont insurance companies

Company |

Rating

|

Complaints

|

|---|---|---|

| Concord | 4.5 out of 5 | Low |

| Frankenmuth | 4.5 out of 5 | Low |

| State Farm | 4.5 out of 5 | Average |

| Vermont Mutual | 4.0 out of 5 | Low |

| Travelers | 3.0 out of 5 | Average |

| Allstate | 2.5 out of 5 | Average |

| Farmers | 2.5 out of 5 | Average |

| Union Mutual | 2.0 out of 5 | Low |

| MMG | 2.0 out of 5 | Low |

Stars in this table represent ratings specific to home insurance.

It's important to choose a home insurance company that will take great care of you if you ever have an emergency.

Companies with great customer service ratings do this by hiring helpful employees and having a quick claims process. Companies with poor customer service reviews likely take longer to pay your claim and you may have to pay more for repairs.

What homeowners insurance do I need in Vermont?

Because of its location in the Northeast, the most frequent risks to Vermont homes are snow, ice and freezing temperatures. Most home insurance policies cover winter damage, whether it's due to heavy snow that caves in your roof or falling ice that damages your deck.

Does homeowners insurance in Vermont cover snow and ice damage?

Home insurance typically covers snow and ice damage.

However, your insurance company may deny your claim if you didn't try to prevent the damage.

For example, if you left heavy snow on your roof for days or weeks, your insurance company may claim that you neglected your home. In this case, they may not pay for repairs.

To avoid this, it’s best to clear snow and ice off your home right after a snowfall.

Does home insurance in Vermont cover burst frozen pipes?

Home insurance typically covers damage caused by frozen pipes that leak or burst.

Your homeowners insurance policy typically requires you to try to prevent this.

For example, if you turn down your heat before leaving on vacation and the pipes freeze, your insurance company may deny your claim. In this case, you'll have to pay to repair them.

And if you neglect a damaged pipe and the problem gets worse, you'll have to pay for any damage it causes, too.

How to find the best home insurance in Vermont

The best homeowners insurance companies have great customer service and helpful coverage at an affordable rate. To find the best insurance for you, start by figuring out how much coverage you need. Then, shop around for multiple quotes and compare customer service ratings.

Decide how much home insurance you need. Most basic homeowners insurance policies come with the same standard coverages. This includes protection for your home and belongings. However, some homeowners may need more protection than a basic policy can offer.

For example, some companies offer water backup coverage as an optional add-on. This coverage pays for damage caused by backed up drains and sewers or a broken sump pump. It could be an important addition to a policy for homeowners with sump pumps who worry about a flooded basement.

As you ask for quotes, make sure that any companies you're comparing offer the coverage you need.

Compare quotes from multiple companies. This could save you a lot of money. In Vermont, there's a difference of more than $1,000 per year between the most and least expensive companies. But make sure your coverage limits are the same on each quote so you're making an apples-to-apples comparison.

In addition, each insurance company calculates home insurance rates differently. Companies typically consider things like your age, credit score, your home's location, style and building materials. For that reason, the cheapest company for you may be different from the best choice for your friends, family or neighbors.

Consider customer service reviews. The best home insurance companies have a stress-free claims process and helpful customer service representatives. Poor customer service can lead to a lot of back and forth with the insurance company before you can fix your home.

When researching customer service, start with our ValuePenguin editor's ratings. ValuePenguin ratings consider customer service scores, coverage availability and cost. You can also consider J.D. Power home insurance satisfaction scores and the National Association of Insurance Commissioners (NAIC) complaint index.

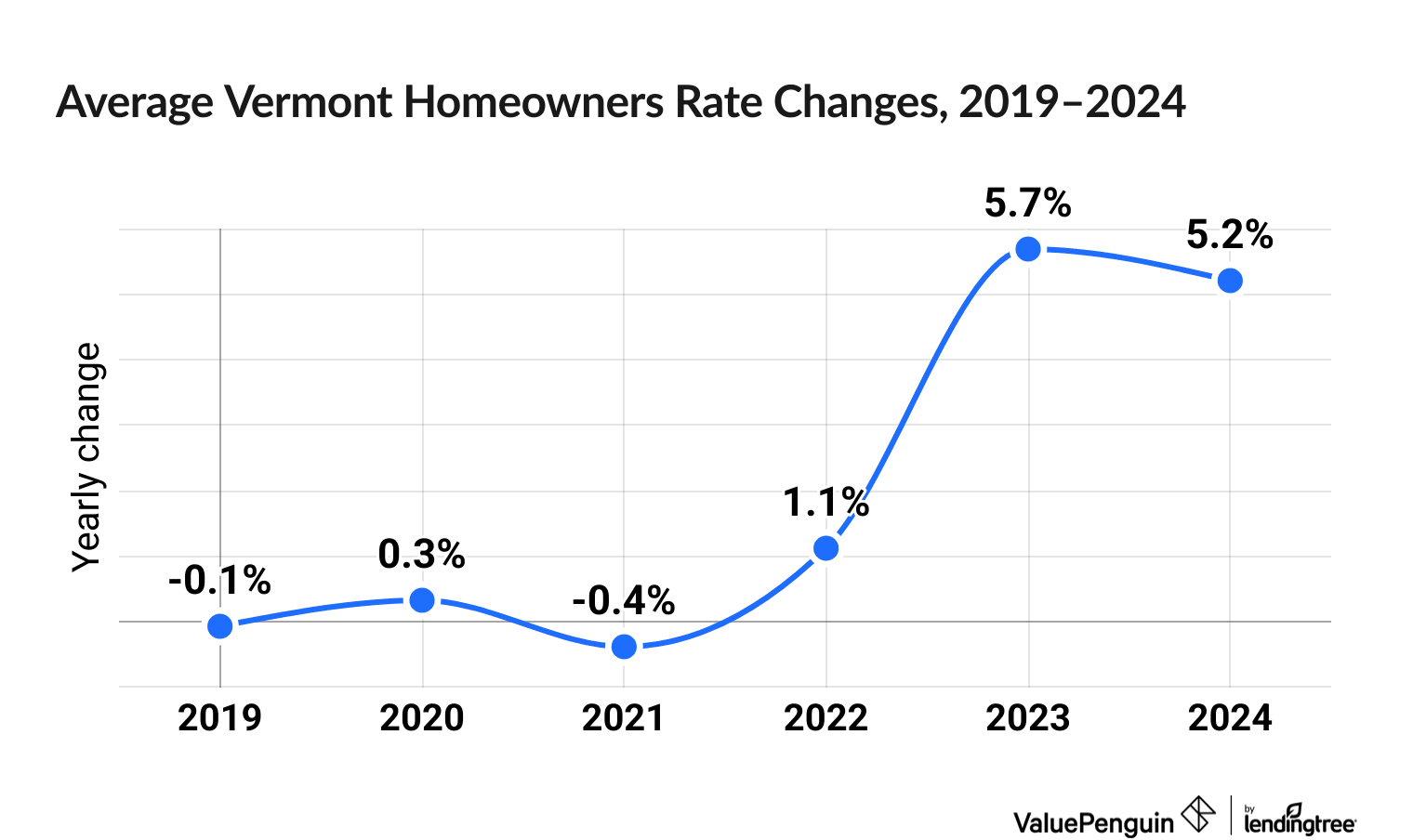

Change in Vermont home insurance cost over time

Home insurance prices are up 12.2% in Vermont over the last six years.

That's good news for Vermont homeowners, as that's the smallest change of any state during that time.

The biggest increase among companies over the period belonged to Progressive, increasing 41.8%. Liberty Mutual followed at 32.7%.

Two companies actually experienced rate decreases over the last five years: USAA (down 5.2%) and State Farm (down 5.4%).

Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

Frequently asked questions

What is the average cost of homeowners insurance in Vermont?

The average cost of homeowners insurance in Vermont is $929 per year, or $77 per month. That’s 57% cheaper than the national annual average of $2,151.

Which company has the cheapest home insurance in Vermont?

Vermont Mutual offers the cheapest home insurance for most people in Vermont, at $533 per year, on average. This is 43% cheaper than the state average.

Which company has the best home insurance in Vermont?

Concord offers the best home insurance in Vermont, along with cheap quotes and great customer service scores. But if you're looking for better bundling discounts or online features, State Farm might be the best company for you.

How much is home insurance in Burlington, VT?

Homeowners insurance in Burlington costs an average of $882 per year. That's 5% cheaper than the Vermont state average.

Methodology

To find the best cheap home insurance in VT, ValuePenguin collected insurance quotes for homes in every ZIP code in Vermont from the state's largest insurance companies. Rates are for a 45-year-old married man with a good credit score and no prior insurance claims. Quotes include the following coverage limits:

- Dwelling coverage: $200,000, $350,000, $500,000 or $1 million

- Personal liability: $100,000

- Medical payments: $5,000

- Deductible: $1,000

ValuePenguin's analysis used insurance rate data from Quadrant Information Services. These rates were publicly sourced from insurance company filings and should be used for comparative purposes only. Your own quotes may be different.

ValuePenguin ranked each company's customer service scores by comparing the National Association of Insurance Commissioners (NAIC) complaint index, J.D. Power's home insurance customer satisfaction rankings and our ValuePenguin editor's ratings.

About the Author

Senior Writer

Lindsay Bishop is a Senior Writer at ValuePenguin, where she educates readers about home, auto, renters, flood and motorcycle insurance.

Lindsay began her career in the insurance and financial industry in 2010. She was a licensed auto, home, life and health insurance agent and held Series 6 and 63 financial licenses.

After a hiatus from the financial sector, Lindsay returned to the industry as a content writer for ValuePenguin in 2021. She enjoys having the opportunity to help readers make smart decisions about their insurance so they can be prepared for anything life throws their way.

When Lindsay isn't writing about insurance, you can find her spending time with family, enjoying the outdoors on Sunday long runs or riding her Peloton.

How insurance helped Lindsay

As a homeowner for 15 years located in South Carolina, Lindsay has plenty of experience navigating the coastal insurance market and managing the claims process. That includes successfully negotiating a full roof replacement claim.

Expertise

- Home insurance

- Car insurance

- Flood insurance

- Renters insurance

- Motorcycle insurance

Referenced by

- CNBC

- Yahoo Finance

- Miami Herald

Education

- BS/BA Economics, University of Nevada Las Vegas

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.