Best & Cheapest Home Insurance in Rhode Island (2026)

Amica typically has the cheapest home insurance in Rhode Island, at $1,366/yr, on average. | ||

Home insurance in Rhode Island costs an average of $2,096/yr, 12% less than the national average. | ||

Homes along Rhode Island’s southern coast and bayfront areas tend to have the most expensive insurance. Average rates can reach over $2,600/yr. |

Find Cheap Home Insurance Quotes in Rhode Island

Who has the best cheap home insurance in RI?

Who has the cheapest homeowners insurance in RI?

Amica has the cheapest homeowners insurance in Rhode Island.

Find Cheap Home Insurance Quotes in Rhode Island

- Amica's home insurance tends to cost 35% to 47% less than the Rhode Island state average, depending on how much coverage you need. Amica also has exceptional customer service, so it's the best choice for most people.

- NLC Insurance also has very affordable home insurance rates ranging from 30% to 36% cheaper than the statewide average. NLC has lots of insurance agents throughout the Rhode Island area, so it's a great choice if you prefer having a personal relationship with your agent.

Homeowners insurance quotes in Rhode Island by dwelling coverage

Key takeaways

- Home insurance rates in Rhode Island went up by just 3% in 2025. That's about half the national average. It's also an improvement from double-digit increases in 2023 and 2024, when rates went up by around 13% and 11%, respectively.

-

Amica has the cheapest home insurance in Rhode Island and is among the companies that raised rates the least over the past five years.

Between 2021 and 2025, Amica's rates went up by 13%. That's significantly less than the average increase statewide, which was 39% over those five years.

- Water causes the most damage to Rhode Island homes. Most of that is likely caused by pipe leaks, old roofs or overflowing appliances, as Rhode Island hasn't experienced many serious floods in the past few years.

Best home insurance in RI for most people: Amica

-

Annual cost$1,366Average rate for a $350,000 home

-

Monthly cost$114Average rate for a $350,000 home

-

Customer complaints Low

Best for local agents: NLC Insurance

-

Annual cost$1,458Average rate for a $350,000 home

-

Monthly cost$121Average rate for a $350,000 home

-

Customer complaints Low

Best for coastal homes: Allstate

-

Annual cost$1,943Average rate for a $350,000 home

-

Monthly cost$162Average rate for a $350,000 home

-

Customer complaints Average

Best homeowners insurance in RI

Amica is the best-rated home insurance company in Rhode Island.

Amica offers the best combination of excellent customer service, affordable rates and useful coverage options.

Top-rated home insurance in RI

Company |

Rating

|

Complaints

|

|---|---|---|

| Amica | 5.0 out of 5 | Low |

| AIG | 4.3 out of 5 | Low |

| NLC Insurance | 3.8 out of 5 | Low |

| Nationwide | 3.5 out of 5 | Low |

| Allstate | 3.3 out of 5 | Average |

Stars in this table represent ratings specific to home insurance.

What is the average cost of RI homeowners insurance?

The average cost of home insurance in Rhode Island is $2,096 per year.

That's $299 less per year than the national average, which is $2,395 per year.

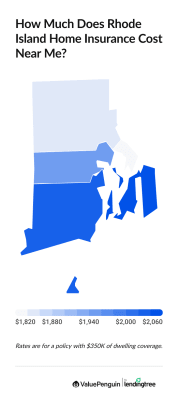

Dwelling coverage | Average rate |

|---|---|

| $200,000 | $1,402 |

| $350,000 | $2,096 |

| $500,000 | $2,816 |

| $1 million | $5,371 |

Home insurance rates in Rhode Island are fairly average compared to neighboring states. Homeowners insurance in Massachusetts costs around $1,635 per year, while Connecticut homeowners pay an average of $2,346 per year.

How much is home insurance in Providence, RI?

Homeowners insurance in Providence costs an average of $2,118 per year. That's $22 per year more than the Rhode Island average.

Providence homeowners can find the cheapest insurance at Amica, where a policy costs around $1,409 per year.

Rhode Island homeowners insurance rates by city

Cumberland, a suburban town outside of Providence, has the cheapest home insurance quotes in Rhode Island.

The average cost of home insurance in Cumberland is $1,866 per year, 11% less than the state average.

Block Island is the most expensive place for home insurance in Rhode Island. At an average rate of $2,632 per year, Block Island home insurance costs 26% more than the state average.

Block Island is south of Rhode Island off the eastern tip of Long Island, NY. As an island, it's more prone to damage from tropical storms, hurricanes and nor'easters. That's partially why insurance is more expensive on Block Island than in the rest of the state.

Find Cheap Home Insurance Quotes in Rhode Island

Cheapest home insurance quotes by RI city

City | Average rate | Cheapest company | Cheapest rate |

|---|---|---|---|

| Adamsville | $2,245 | NLC Insurance | $1,268 |

| Albion | $1,910 | Amica | $1,438 |

| Ashaway | $2,047 | Amica | $1,030 |

| Barrington | $1,923 | Amica | $1,154 |

| Block Island | $2,632 | Amica | $1,030 |

Rates are for a policy with $350,000 of dwelling coverage.

What homeowners insurance do I need in Rhode Island?

As a coastal New England state, Rhode Island is at risk of damage from tropical storms and nor’easters.

Water causes the most damage to Rhode Island homes. This can be from weather-related flooding, leaky roofs, burst pipes or overflowing appliances.

Does Rhode Island home insurance cover tropical storms?

Homeowners insurance covers some, but not all, types of tropical storm and hurricane damage.

It typically pays for damage from wind, hail and lightning, but not from floods.

However, coastal homes may have a separate wind or hurricane deductible. This is typically higher than your regular deductible. So be prepared to pay extra if a tropical storm damages your home.

Does Rhode Island homeowners insurance cover water damage?

Homeowners insurance covers some types of water damage, such as burst pipes or roof leaks.

However, you typically have to buy extra coverage to protect against overflowing sump pumps, backed-up sewers or weather-related floods, such as storm surge or rising rainwater.

From 2020 through 2025, the National Flood Insurance Program paid over $17 million to fix flood damage across Rhode Island, with the average claim costing about $57,000.

The majority of claim damage was in Providence County, which had nearly $9.6 million in damage over that period. Providence County is home to about 60% of Rhode Island residents.

Where can Rhode Island homeowners get flood insurance?

Rhode Island homeowners can get flood insurance through the National Flood Insurance Program (NFIP) or a private insurance company.

You can buy a National Flood Insurance Program (NFIP) policy from many home insurance companies, including Amica. The government backs NFIP policies, and they cost the same no matter which company you buy them from. The average cost of an NFIP policy in Rhode Island is $1,094 per year.

You may want to consider private flood insurance if your home would cost more than $250,000 to rebuild, you have valuable belongings or you want a policy that pays your expenses if your home becomes uninhabitable due to flood damage. Allstate and Narragansett Bay both offer private flood insurance options.

Does Rhode Island home insurance cover winter storms?

Rhode Island has winters that bring potentially damaging levels of snowfall and ice. Homeowners insurance usually covers any damage from the weight of falling snow.

However, most insurance companies won’t cover damage caused by lack of maintenance, also called negligence. It’s important to shovel heavy snow off your roof and chip away the ice to help prevent damage to your home.

How to find the best homeowners insurance in Rhode Island

Before you begin shopping for home insurance in Rhode Island, you should understand how much coverage you need. Then, you can compare quotes from multiple companies and read customer service reviews.

Decide how much coverage you need. Most standard home insurance policies include similar coverage. However, some homes may need more protection.

For example, Allstate and Narragansett Bay offer flood protection. This is an important add-on if you live near the coast.

Shop for quotes from multiple companies. The most expensive company in Rhode Island costs twice as much as the cheapest option. That's a difference of over $1,500 per year for a policy with $350,000 of dwelling coverage.

In addition, each insurance company calculates rates differently. Companies consider your insurance history and credit score, your home's location and building materials, and other factors. So the best company for you may differ from your neighbors, family and friends.

Consider customer service ratings. It's important to choose a company you can rely on in an emergency. Companies with excellent service reviews typically get your life back on track quickly after your home is damaged. On the other hand, companies with poor service might take longer to send you a check.

ValuePenguin editor's ratings consider customer service reviews from multiple sources, along with coverage availability and overall value. If you want to do more research, look up J.D. Power customer service scores and the National Association of Insurance Commissioners (NAIC) complaint index.

Change in Rhode Island home insurance cost over time

Home insurance prices are up 39% in Rhode Island over the last five years.

Home insurance rates were much more stable across Rhode Island in 2025, after double-digit increases in 2023 and 2024.

Year | Rate increase |

|---|---|

| 2021 | 2.82% |

| 2022 | 4.57% |

| 2023 | 12.58% |

| 2024 | 11.23% |

| 2025 | 2.93% |

Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

Travelers and State Farm had the lowest rate increases over the last five years, at 3.6% and 4.9%, respectively. However, State Farm isn't currently selling new home insurance policies in Rhode Island.

Vermont Mutual had the biggest rate increase over this period, at 87.6%. That's more than double the Rhode Island average.

Frequently asked questions

What is the average cost of homeowners insurance in Rhode Island?

The average cost of homeowners insurance in Rhode Island is $2,096 per year, or $175 per month. That’s 12% cheaper than the national annual average of $2,395.

What is the best home insurance in Rhode Island?

Amica has the best home insurance in Rhode Island for most people. It has the cheapest rates in the state, along with excellent customer service reviews.

How much is home insurance in Warwick, RI?

Home insurance in Warwick costs an average of $2,128 per year. That's $32 per year more than the Rhode Island average. Homeowners in Warwick can find the cheapest rates at NLC Insurance, where a policy costs an average of $1,251 per year.

Methodology

To find the best cheap RI insurance company, ValuePenguin collected home insurance quotes for every ZIP code across Rhode Island from the state’s largest home insurance companies. Rates are for a 45-year-old married man with a good credit score and no history of insurance claims. Quotes are for a 1,913 square foot home built 48 years ago, based on the average home age and size in Rhode Island.

Rates include the following coverage limits:

- Dwelling coverage: $200,000, $350,000, $500,000 or $1 million

- Personal liability: $100,000

- Medical payments: $1,000

- Deductible: $1,000

ValuePenguin's analysis used insurance rate data from Quadrant Information Services. These rates were publicly sourced from insurance company filings and should be used for comparative purposes only. Your own quotes may be different.

Our experts ranked each company's customer service scores by comparing the National Association of Insurance Commissioners (NAIC) complaint index, J.D. Power's home insurance customer satisfaction rankings and our ValuePenguin editor's ratings.

About the Author

Senior Writer

Lindsay Bishop is a Senior Writer at ValuePenguin, where she educates readers about home, auto, renters, flood and motorcycle insurance.

Lindsay began her career in the insurance and financial industry in 2010. She was a licensed auto, home, life and health insurance agent and held Series 6 and 63 financial licenses.

After a hiatus from the financial sector, Lindsay returned to the industry as a content writer for ValuePenguin in 2021. She enjoys having the opportunity to help readers make smart decisions about their insurance so they can be prepared for anything life throws their way.

When Lindsay isn't writing about insurance, you can find her spending time with family, enjoying the outdoors on Sunday long runs or riding her Peloton.

How insurance helped Lindsay

As a homeowner for 15 years located in South Carolina, Lindsay has plenty of experience navigating the coastal insurance market and managing the claims process. That includes successfully negotiating a full roof replacement claim.

Expertise

- Home insurance

- Car insurance

- Flood insurance

- Renters insurance

- Motorcycle insurance

Referenced by

- CNBC

- Yahoo Finance

- Miami Herald

Education

- BS/BA Economics, University of Nevada Las Vegas

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.