The Best and Cheapest Home Insurance in Georgia (2026)

Auto-Owners has the best mix of cheap rates and great service in GA, at $1,954/yr. | ||

Home insurance in Georgia costs an average of $2,640/yr. | ||

People living in rural or coastal areas of Georgia tend to pay the most for home insurance, with average rates that can get as high as $3,239/yr. |

Auto-Owners has the best mix of cheap rates and great service in GA, at $1,954/yr. | ||

Home insurance in Georgia costs an average of $2,640/yr. But some areas have average rates as high as $3,239/yr. |

Find Cheap Home Insurance Quotes in Georgia

Who has the best cheap home insurance in Georgia?

Cheapest home insurance in Georgia

State Farm has the overall cheapest home insurance quotes in Georgia.

Find Cheap Home Insurance Quotes in Georgia

-

A policy from State Farm costs around $1,770 per year for $350,000 of dwelling coverage.

That's $870 per year less than the Georgia average of $2,640.

-

Auto-Owners is 10% more expensive than State Farm, at $1,954 per year. But it has better customer service reviews and coverage options than State Farm. That makes Auto-Owners the best choice for most Georgia homeowners.

-

State Farm also has excellent rates for more expensive homes in Georgia. It's the cheapest option for homes that would cost $500,000 or $1 million to rebuild.

GA home insurance quotes by dwelling coverage

$200,000

$350,000

$500,000

$1 million

Company | Annual rate | ||

|---|---|---|---|

| Alfa | 3.8 out of 5 | $1,214 | |

| Pure | 4.3 out of 5 | $1,274 |

| State Farm | 3.5 out of 5 | $1,317 | |

| Auto-Owners | 4.5 out of 5 | $1,443 | |

| Allstate | 4.0 out of 5 | $1,485 | |

Key takeaways

- Georgia home insurance rates went up around 8.6% in 2025, compared to 5.6% nationally.

- State Farm has raised rates the least among major Georgia insurance companies during the past five years. State Farm customers have seen their rates go up by 16.7% since 2021. While that's not a small increase, it's much lower than the state average increase of 39.7%.

- Georgia homeowners should make sure their homes are protected against wind damage, which caused the most damage to homes across the state in 2024. Most home insurance policies include wind coverage, but if your home is in a high-risk area, you may need to buy separate wind insurance.

Best home insurance in GA for most people: Auto-Owners

-

Annual cost$1,954Average rate for a $350,000 home

-

Monthly cost$163Average rate for a $350,000 home

-

Customer complaints Low

Cheapest homeowners insurance in GA: State Farm

-

Annual cost$1,770Average rate for a $350,000 home

-

Monthly cost$148Average rate for a $350,000 home

-

Customer complaints Average

Best for storm coverage: Nationwide

-

Annual cost$2,926Average rate for a $350,000 home

-

Monthly cost$244Average rate for a $350,000 home

-

Customer complaints Low

What are the top-rated homeowners insurance companies in Georgia?

The best home insurance company in GA is Auto-Owners.

It has a high ValuePenguin editor rating and fewer customer complaints than average, according to the National Association of Insurance Commissioners (NAIC).

Georgia homeowners with military ties could find the best customer service at USAA. However, only military members, veterans and some of their family members can buy home insurance from USAA.

Best home insurance in Georgia

Company |

Rating

|

Complaints

|

|---|---|---|

| Auto-Owners | 4.5 out of 5 | Low |

| USAA | 4.5 out of 5 | Low |

| Pure | 4.3 out of 5 | Low |

| Allstate | 4.0 out of 5 | Average |

| Alfa | 3.8 out of 5 | Average |

Average cost of homeowners insurance in Georgia

The average home insurance cost in Georgia is $2,640 per year for a policy with $350,000 of dwelling coverage.

That's about 10% more than the average cost of coverage in the U.S., which is $2,395 per year.

Annual cost of home insurance in GA by dwelling coverage amount

Dwelling coverage | Average rate |

|---|---|

| $200,000 | $1,813 |

| $350,000 | $2,640 |

| $500,000 | $3,562 |

| $1 million | $6,317 |

Although the Georgia coast is prone to hurricanes, it has slightly cheaper home insurance quotes than neighboring Florida. The average cost of homeowners insurance in Florida is around $51 per year more expensive, at $2,691 per year.

Cost of home insurance in Atlanta, GA

The average cost of homeowners insurance in Atlanta is $2,772 per year.

That's 5% more expensive than the Georgia average of $2,640 per year.

Home insurance in Atlanta is more expensive than in its surrounding cities. For example, rates in Athens are only $2,407 per year, on average.

City | Annual rate |

|---|---|

| Atlanta | $2,772 |

| Athens | $2,407 |

| Johns Creek | $2,523 |

| Roswell | $2,515 |

| Alpharetta | $2,482 |

Rates are for a policy with $350,000 of dwelling coverage.

Home insurance quotes in GA by city

The most expensive city in Georgia for homeowners insurance is Glenn, a Census-designated place near the Alabama border.

Glenn homeowners pay an average of $3,239 per year. This is possibly because Glenn is very rural and isolated from fire protection, leading to a greater risk of damage from wildfires.

Homeowners in Bethlehem, a small town between Atlanta and Athens, have the cheapest home insurance costs in Georgia at $2,379 per year.

Find Cheap Homeowners Insurance Quotes in Your Area

Cost of Georgia homeowners insurance by city

City | Average rate | Cheapest company | Cheapest rate |

|---|---|---|---|

| Abbeville | $2,743 | Pure | $1,729 |

| Acworth | $2,541 | Farmers | $1,809 |

| Adairsville | $2,644 | Pure | $1,713 |

| Adel | $2,683 | State Farm | $1,520 |

| Adrian | $2,757 | Pure | $1,729 |

Rates are for a policy with $350,000 of dwelling coverage.

Most common natural disasters in Georgia

Many of Georgia's homes are at risk from hurricanes because of their proximity to the Atlantic Ocean and the Gulf of Mexico. That means homeowners are more likely to experience flooding, even in inland areas.

Tornadoes also come through Dixie Alley and affect the state. There were about 54 tornadoes in Georgia in 2025, according to the National Oceanic and Atmospheric Administration (NOAA).

Does Georgia property insurance cover hurricanes?

Homeowners insurance typically covers damage caused by hurricane winds, but not flood damage.

However, if you live near the coast, your home insurance policy may have a separate hurricane or wind deductible. This deductible is typically between 1% and 10% of your dwelling coverage limit.

If the insurance company considers your home very high-risk for wind damage, it may not offer you wind protection. In this case, you may have to buy a separate wind insurance policy. If you live near the coast, check with your insurance agent to make sure your home has wind damage protection.

Does GA homeowners insurance cover flooding?

Homeowners insurance doesn't cover weather-related flooding.

You should consider buying flood insurance if your home is near the coast or a large body of water, or at a lower elevation than the surrounding areas. If your home is in a designated flood zone, your mortgage lender will typically require you to have a flood insurance policy.

Georgia homeowners can buy flood insurance from the National Flood Insurance Program (NFIP) or a private insurance company.

An NFIP flood insurance policy costs an average of $872 per year in Georgia. There are more than 73,000 NFIP policies in effect in Georgia. The average policy includes around $285,000 of combined dwelling and personal property coverage.

Does home insurance in GA cover tornadoes?

Most homeowners insurance policies protect against damage caused by tornadoes. That's because home insurance typically covers wind damage, which includes damage from both tornadoes and hurricanes.

If you live in an area with frequent tornadoes, your home insurance may have a separate deductible for wind damage. This is usually higher than your main deductible and is generally a percentage of your dwelling coverage limit.

How to find the best cheap homeowners insurance in GA

To find the best home insurance in Georgia, you should shop around for the cheapest rates, look for discounts and consider customer service reviews.

Compare home insurance quotes from multiple companies. There's a difference of $2,217 per year between the most and least expensive home insurance companies in Georgia.

Home insurance companies consider the location of your home, its building materials, your insurance history and many other factors to determine your rate. The cheapest company for you may not be the same as the best choice for your friends or neighbors. That's why it's important to shop around to find the cheapest quote for your home.

Look for home insurance discounts. Homeowners could save 20% or more on their insurance by taking advantage of discounts.

Bundling your home and auto insurance will typically get you the largest discount. You can also save by signing up for automatic payments, installing an alarm system or upgrading your home with certain safety features, like hurricane shutters.

Consider customer service reviews. The best home insurance in Georgia offers a combination of cheap rates and excellent customer service.

Service can be extremely important if something happens to your home and you have to file a claim. You want to be sure you can count on your insurance company to get your life back to normal quickly in an emergency situation.

Start by reviewing ValuePenguin's editor ratings, which consider customer complaints and reviews, cost, coverage options and availability. You can also research J.D. Power customer satisfaction scores and complaint data with the National Association of Insurance Commissioners (NAIC).

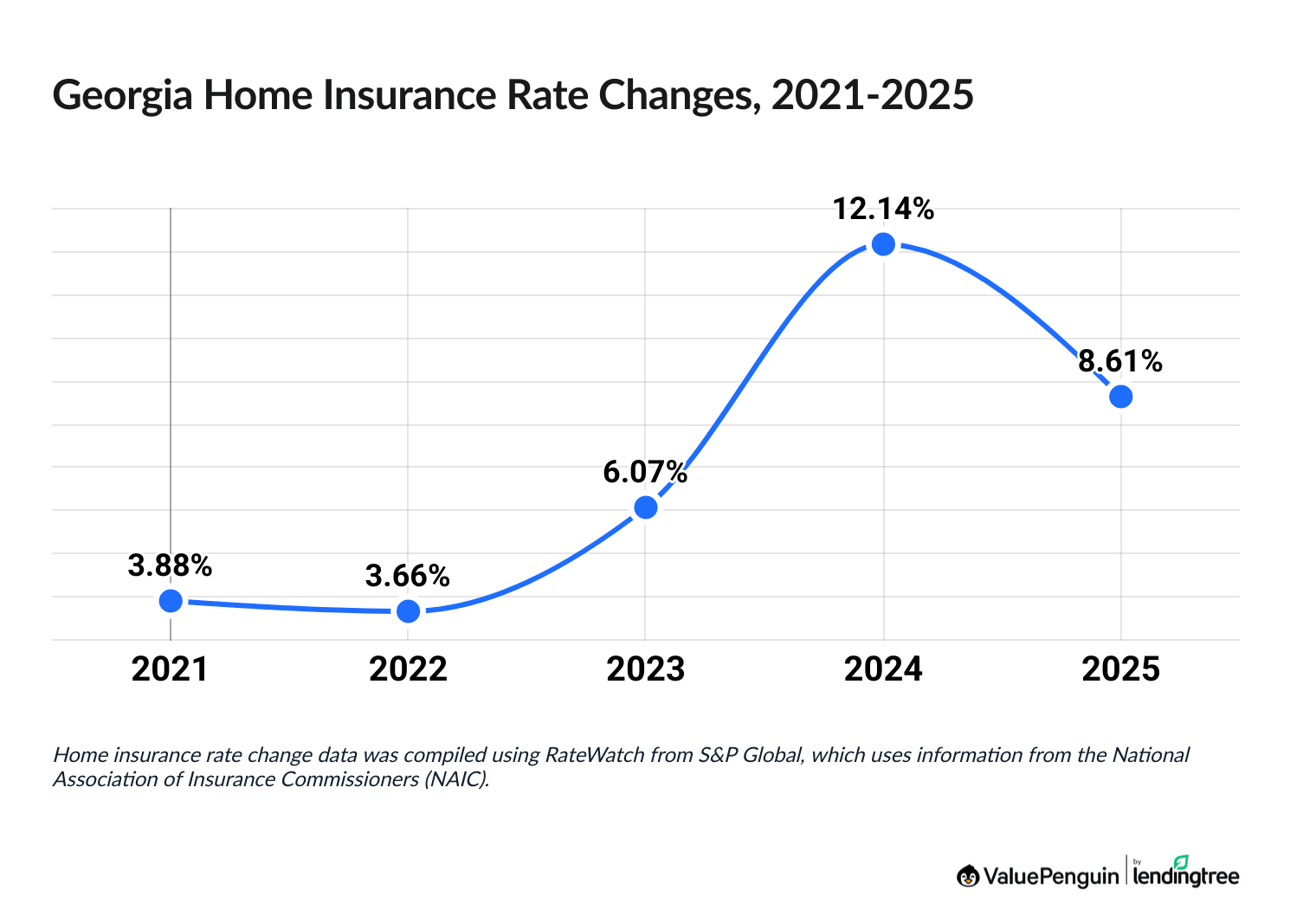

Georgia home insurance trends

Home insurance costs have gone up 39.7% in Georgia over the last five years.

Georgia homeowners have seen an especially large increase in the last three years, with a 12% increase in 2024 and 9% in 2025.

Year | Rate increase |

|---|---|

| 2021 | 3.88% |

| 2022 | 3.66% |

| 2023 | 6.07% |

| 2024 | 12.14% |

| 2025 | 8.61% |

Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

Among large companies, State Farm had the smallest rate hike, with an increase of just 16.7% since 2021. Nationwide had the second-smallest rate hike, at 23.3%.

Frequently asked questions

What is the average cost of homeowners insurance in Georgia?

Homeowners insurance in Georgia costs an average of $2,640 per year, or $220 per month. However, average rates can fluctuate by up to $860 per year depending on where you live.

What's the best homeowners insurance in Georgia?

Auto-Owners has the best home insurance in Georgia for most people. A policy from Auto-Owners costs around $1,954 per year, and the company has excellent customer service reviews.

What is the cheapest Atlanta home insurance?

State Farm has the cheapest home insurance in Atlanta, at $1,774 per year. State Farm also has good customer service and lots of ways to customize your home insurance coverage.

Are you required to have homeowners insurance in Georgia?

The state of Georgia doesn't require homeowners to have insurance coverage. However, if you have a mortgage, your lender typically requires you to buy a home insurance policy.

Why is home insurance so high in GA?

Georgia home insurance costs an average of $2,640 per year, which is about 10% higher than the national average. However, rates can be much higher for homes located along the coast and in areas with frequent tornadoes. That's because homeowners in these areas are more likely to file an insurance claim due to weather-related damage.

Methodology

To find the best homeowners insurance in Georgia, ValuePenguin gathered quotes in every ZIP code in the state from the largest homeowners insurance companies. Rates are for a 2,262 square foot home built 41 years ago, based on the average home age and size in Georgia.

ValuePenguin sourced quotes for properties at four levels of dwelling coverage to understand the cost of coverage for a variety of homes.

- Dwelling coverage: $200,000, $350,000, $500,000 or $1 million

- Personal liability: $100,000

- Medical payments: $1,000

- Deductible: $1,000

ValuePenguin's analysis used insurance rate data from Quadrant Information Services. These rates were publicly sourced from insurer filings and should be used for comparative purposes only — your own quotes will be different.

Each company's customer service was ranked by comparing the National Association of Insurance Commissioners (NAIC) complaint index, J.D. Power's home insurance customer satisfaction and claims satisfaction rankings and ValuePenguin editor's ratings.

Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

About the Author

Lead Writer

Matt Timmons is a Lead Writer on the insurance team at ValuePenguin, where he writes in-depth and timely pieces helping find the right coverage for them.

He's covered insurance at ValuePenguin since 2018, specializing in auto and home insurance, as well as life insurance. He's paid special attention to the EV insurance market, where prices are much higher than for gas cars.

Before he started writing about personal finance, Matt wrote about professional skills and online tools at an e-learning company.

How insurance helped Matt

During freshman orientation in college, Matt's iPod was stolen off his table while he was eating lunch. Luckily, he'd bought a college insurance plan the day before and he had money to buy a replacement before classes started.

Expertise

- Auto insurance

- Home insurance

- Insurance rate analysis

- Life insurance

Referenced by

- CNBC

- Miami Herald

- Yahoo! Finance

Education

- BA, Wesleyan University

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.