Best Cheap Home Insurance Companies in Colorado (2026)

Allstate typically has the cheapest home insurance in Colorado, at $2,487/yr, on average. | ||

Homeowners insurance in Colorado costs an average of $4,310/yr, which makes it the third-most expensive state for home insurance in the U.S. | ||

People living in rural towns throughout Colorado's hail-prone eastern plains tend to pay much more for home insurance, with average rates as high as $5,800/yr. |

Find Cheap Home Insurance Quotes in Colorado

Who has the best cheap home insurance in CO?

Who has the cheapest homeowners insurance in Colorado?

Allstate and Auto-Owners have the most affordable homeowners insurance in Colorado.

Find Cheap Home Insurance Quotes in Colorado

- Allstate has the cheapest home insurance for most Colorado homeowners. Allstate typically costs 29% to 61% less than the Colorado average, depending on how much coverage you need.

- However, Auto-Owners has the cheapest rates for affordable homes. A policy from Auto-Owners with $200,000 of dwelling coverage is 43% cheaper than average.

Best cheap homeowners insurance in CO

$200,000

$350,000

$500,000

$1 million

Company | Annual rate | ||

|---|---|---|---|

| Auto-Owners | 4.5 out of 5 | $1,705 | |

| State Farm | 3.5 out of 5 | $1,821 | |

| Allstate | 4.0 out of 5 | $2,131 | |

| Shelter | 3.8 out of 5 | $2,156 | |

| Farm Bureau | 2.8 out of 5 | $3,267 | |

| Country Financial | 2.5 out of 5 | $3,488 | |

| Travelers | 1.0 out of 5 | $3,544 | |

| Nationwide | 2.5 out of 5 | $3,595 | |

| American Family | 3.0 out of 5 | $3,613 | |

| Farmers | 2.0 out of 5 | $4,192 | |

| USAA | 3.0 out of 5 | $3,327 | |

Key takeaways

Best home insurance in CO for most people: Allstate

-

Annual cost$2,487Average rate for a $350,000 home

-

Monthly cost$207Average rate for a $350,000 home

-

Customer complaints Average

Cheapest home insurance companies in Colorado Springs

Company | Annual rate | |

|---|---|---|

| Allstate | $2,441 | |

| State Farm | $2,563 | |

| Auto-Owners | $2,857 | |

| Farm Bureau | $3,401 | |

| Shelter | $4,342 | |

| American Family | $5,956 | |

| Travelers | $6,003 | |

| Nationwide | $6,400 | |

| Country Financial | $6,786 | |

| Farmers | $8,150 | |

| USAA | $5,692 | |

Rates are for a policy with $350,000 of dwelling coverage.

Best for bundling home and auto insurance in Colorado: State Farm

-

Annual cost$2,568Average rate for a $350,000 home

-

Monthly cost$214Average rate for a $350,000 home

-

Customer complaints Average

Cheapest home insurance in Denver

Company | Annual rate | |

|---|---|---|

| State Farm | $2,726 | |

| Auto-Owners | $2,744 | |

| Allstate | $2,816 | |

| Farm Bureau | $3,399 | |

| Shelter | $4,659 | |

| American Family | $5,341 | |

| Travelers | $5,904 | |

| Country Financial | $6,015 | |

| Nationwide | $6,251 | |

| Farmers | $7,133 | |

| USAA | $5,508 | |

Rates are for a policy with $350,000 of dwelling coverage.

Best CO homeowners insurance for customer satisfaction: Auto-Owners

-

Annual cost$2,587Average rate for a $350,000 home

-

Monthly cost$216Average rate for a $350,000 home

-

Customer complaints Average

Auto-Owners customers are typically happy with the company's claims process. This is important because making a home insurance claim can be really stressful. So knowing your insurance company will take great care of you if your home is damaged or destroyed in the future is crucial.

- Auto-Owners gets less than half as many customer complaints as a typical company its size, according to the NAIC.

- Auto-Owners also earned a high score on J.D. Power's claims satisfaction survey.

- Auto-Owners didn't score as well on J.D. Power's overall customer satisfaction survey. However, this survey also includes things like pricing and shopping experience. So its score could be influenced by the fact that Auto-Owners doesn't offer online quotes.

Although Auto-Owners isn't always the cheapest option in Colorado, it offers lots of discounts to help lower your insurance bill. For instance, you can save money if you pay your annual bill upfront or install an automatic backup generator.

Best home insurance if you can't find coverage: Colorado FAIR Plan

Top-rated Colorado home insurance companies

Auto-Owners has the best-rated home insurance in Colorado.

Auto-Owners earned a high rating from ValuePenguin editors for combining affordable rates, great customer service and quality coverage.

Colorado home insurance company reviews

Company |

Rating

|

Complaints

|

|---|---|---|

| Auto-Owners | 4.5 out of 5 | Low |

| Allstate | 4.0 out of 5 | Average |

| Chubb | 3.8 out of 5 | Low |

| Shelter | 3.8 out of 5 | Low |

| State Farm | 3.5 out of 5 | Average |

| American Family | 3.0 out of 5 | Average |

| USAA | 3.0 out of 5 | Low |

| Farm Bureau | 2.8 out of 5 | High |

| Country Financial | 2.5 out of 5 | Low |

| Nationwide | 2.5 out of 5 | High |

| Farmers | 2.0 out of 5 | Average |

| Travelers | 1.0 out of 5 | Average |

How much does home insurance cost in Colorado?

Homeowners insurance costs an average of $4,310 per year in Colorado.

That makes Colorado the third-most expensive state in the U.S. for home insurance.

Average cost of home insurance in CO

Dwelling coverage | Average rate |

|---|---|

| $200,000 | $2,985 |

| $350,000 | $4,310 |

| $500,000 | $5,553 |

| $1,000,000 | $8,939 |

Colorado has higher home insurance rates than most of its neighboring states. Home insurance is much cheaper in Arizona, where it costs $2,225, and Nevada, where coverage costs $1,633 per year. However, rates in nearby Nebraska are more expensive, at $4,956 per year.

Homeowners insurance quotes in Colorado by city

Where you live in Colorado has a big impact on how much you pay for home insurance.

- Burlington, a small city on Colorado's Eastern Plains, has the most expensive home insurance rates in the state, at $5,794 per year.

- Fruitvale, a community just northwest of Grand Junction, has the cheapest home insurance in Colorado, at $1,783 per year. That's $4,011 less per year than the same policy in Burlington.

- Allstate has the cheapest home insurance rates in 37% of cities and towns across Colorado, including Colorado Springs and Aurora. Allstate also tends to be the most affordable option in many of Colorado's most expensive cities throughout the Eastern Plains.

- State Farm has the lowest rates in 34% of cities, including Denver. Auto-Owners is the cheapest company in 16% of cities and towns, while Shelter has the best rates in 13%.

Find Cheap Home Insurance Quotes in Colorado

Cheapest CO home insurance by city

City | Average rate | Cheapest company | Cheapest rate |

|---|---|---|---|

| Acres Green | $4,868 | Auto-Owners | $2,705 |

| Agate | $5,218 | Allstate | $2,430 |

| Aguilar | $3,889 | Allstate | $2,223 |

| Air Force Academy | $4,800 | Allstate | $2,542 |

| Akron | $5,474 | Allstate | $2,692 |

| Alamosa | $2,177 | Allstate | $1,378 |

| Alamosa East | $2,171 | Allstate | $1,378 |

| Allenspark | $4,123 | Auto-Owners | $2,409 |

| Alma | $2,930 | Auto-Owners | $1,858 |

| Almont | $2,063 | State Farm | $1,321 |

| Amherst | $5,619 | State Farm | $2,521 |

| Anton | $5,338 | State Farm | $2,522 |

| Antonito | $2,194 | Shelter | $1,398 |

| Applewood | $4,531 | State Farm | $2,543 |

| Arapahoe | $5,475 | State Farm | $2,522 |

| Arlington | $5,149 | Allstate | $2,448 |

| Arriba | $5,133 | State Farm | $2,512 |

| Arvada | $4,519 | State Farm | $2,579 |

| Aspen | $2,014 | State Farm | $1,101 |

| Atwood | $5,208 | State Farm | $2,521 |

| Ault | $4,305 | Allstate | $2,547 |

| Aurora | $4,736 | Allstate | $2,729 |

| Austin | $1,928 | State Farm | $1,057 |

| Avon | $2,016 | Shelter | $1,348 |

| Avondale | $4,947 | Allstate | $2,278 |

| Bailey | $3,650 | American Family | $2,221 |

| Basalt | $2,012 | State Farm | $1,233 |

| Battlement Mesa | $1,977 | State Farm | $1,218 |

| Bayfield | $2,072 | State Farm | $1,329 |

| Bedrock | $2,140 | Farmers | $1,333 |

| Bellvue | $3,881 | Auto-Owners | $2,202 |

| Bennett | $4,963 | Auto-Owners | $2,838 |

| Berkley | $4,515 | State Farm | $2,636 |

| Berthoud | $3,878 | Allstate | $2,138 |

| Bethune | $5,561 | State Farm | $2,528 |

| Beulah | $4,652 | Allstate | $2,426 |

| Black Forest | $5,238 | Allstate | $2,716 |

| Black Hawk | $3,775 | American Family | $2,221 |

| Blanca | $2,536 | Shelter | $1,398 |

| Blende | $4,982 | Allstate | $2,233 |

| Blue River | $2,319 | Travelers | $1,185 |

| Boncarbo | $3,807 | Allstate | $2,130 |

| Bond | $2,183 | Shelter | $1,348 |

| Boone | $4,948 | Allstate | $2,306 |

| Boulder | $4,137 | Allstate | $2,387 |

| Bow Mar | $4,481 | State Farm | $2,621 |

| Branson | $4,460 | Auto-Owners | $2,589 |

| Breckenridge | $2,301 | Travelers | $1,185 |

| Briggsdale | $4,734 | Auto-Owners | $2,803 |

| Brighton | $4,546 | Allstate | $2,578 |

| Brookside | $3,298 | Allstate | $1,728 |

| Broomfield | $4,150 | Allstate | $2,218 |

| Brush | $5,429 | Allstate | $2,543 |

| Buena Vista | $2,144 | State Farm | $1,336 |

| Buffalo Creek | $4,340 | Allstate | $1,560 |

| Burlington | $5,794 | Allstate | $2,656 |

| Burns | $2,456 | Shelter | $1,348 |

| Byers | $5,382 | Auto-Owners | $2,961 |

| Cahone | $2,096 | Farmers | $1,389 |

| Calhan | $5,128 | Allstate | $2,867 |

| Campo | $5,010 | State Farm | $2,522 |

| Canon City | $3,272 | Allstate | $1,728 |

| Capulin | $2,245 | Shelter | $1,398 |

| Carbondale | $1,956 | State Farm | $1,077 |

| Carr | $4,347 | Allstate | $2,370 |

| Cascade | $4,996 | Allstate | $2,566 |

| Castle Pines | $4,801 | Auto-Owners | $2,701 |

| Castle Pines North | $4,777 | Auto-Owners | $2,701 |

| Castle Rock | $4,778 | Auto-Owners | $2,758 |

| Cedaredge | $2,022 | State Farm | $1,169 |

| Centennial | $4,698 | Auto-Owners | $2,741 |

| Center | $2,096 | State Farm | $1,095 |

| Central City | $3,615 | American Family | $1,914 |

| Chama | $2,667 | Nationwide | $1,384 |

| Cherry Creek | $4,735 | Auto-Owners | $2,747 |

| Cherry Hills Village | $4,616 | Auto-Owners | $2,733 |

| Cheyenne Wells | $5,613 | Auto-Owners | $2,606 |

| Chromo | $2,114 | Shelter | $1,398 |

| Cimarron | $2,179 | Shelter | $1,398 |

| Cimarron Hills | $5,051 | Allstate | $2,573 |

| Clark | $2,503 | State Farm | $1,675 |

| Clifton | $1,807 | State Farm | $846 |

| Climax | $2,416 | Shelter | $1,348 |

| Coal Creek | $4,060 | Allstate | $2,497 |

| Coaldale | $3,158 | Allstate | $1,744 |

| Coalmont | $2,445 | Shelter | $1,754 |

| Collbran | $2,203 | State Farm | $1,294 |

| Colorado City | $4,347 | State Farm | $2,425 |

| Colorado Springs | $4,936 | Allstate | $2,441 |

| Columbine | $4,539 | State Farm | $2,624 |

| Columbine Valley | $4,414 | State Farm | $2,637 |

| Commerce City | $4,677 | Allstate | $2,669 |

| Como | $3,277 | Travelers | $1,875 |

| Conejos | $2,263 | Shelter | $1,398 |

| Conifer | $4,712 | Auto-Owners | $2,659 |

| Cope | $5,346 | State Farm | $2,522 |

| Copper Mountain | $2,290 | Travelers | $1,385 |

| Cortez | $1,900 | State Farm | $990 |

| Cory | $2,115 | Shelter | $1,398 |

| Cotopaxi | $3,174 | Allstate | $1,744 |

| Cowdrey | $2,699 | Shelter | $1,754 |

| Craig | $2,142 | State Farm | $1,029 |

| Crawford | $2,245 | State Farm | $1,159 |

| Creede | $2,098 | State Farm | $1,367 |

| Crested Butte | $2,012 | State Farm | $1,124 |

| Crestone | $2,226 | State Farm | $1,359 |

| Cripple Creek | $3,916 | Allstate | $1,958 |

| Crook | $5,332 | State Farm | $2,521 |

| Crowley | $5,208 | State Farm | $2,508 |

| Dacono | $4,281 | Allstate | $2,131 |

| Dakota Ridge | $4,580 | Allstate | $2,561 |

| De Beque | $2,146 | Shelter | $1,348 |

| Deer Trail | $5,444 | Allstate | $3,037 |

| Del Norte | $2,113 | State Farm | $1,044 |

| Delta | $1,882 | State Farm | $932 |

| Denver | $4,723 | State Farm | $2,726 |

| Derby | $4,662 | Allstate | $2,664 |

| Dillon | $2,318 | Travelers | $1,385 |

| Dinosaur | $2,458 | Farmers | $1,444 |

| Divide | $4,040 | Allstate | $2,719 |

| Dolores | $2,041 | State Farm | $1,283 |

| Dove Creek | $1,989 | Farmers | $1,170 |

| Dove Valley | $4,725 | Auto-Owners | $2,729 |

| Drake | $3,818 | Auto-Owners | $2,272 |

| Dumont | $3,102 | American Family | $1,911 |

| Dupont | $4,496 | Allstate | $2,220 |

| Durango | $2,042 | State Farm | $1,162 |

| Eads | $5,577 | Auto-Owners | $2,587 |

| Eagle | $2,081 | State Farm | $1,170 |

| East Pleasant View | $4,533 | State Farm | $2,545 |

| Eastlake | $4,341 | Allstate | $2,455 |

| Eaton | $4,443 | Allstate | $2,455 |

| Eckert | $1,921 | State Farm | $1,134 |

| Eckley | $5,616 | State Farm | $2,524 |

| Edgewater | $4,567 | State Farm | $2,604 |

| Edwards | $1,995 | Travelers | $1,294 |

| Egnar | $2,219 | Farmers | $1,271 |

| El Jebel | $1,985 | State Farm | $1,080 |

| El Moro | $4,058 | Allstate | $2,055 |

| Elbert | $5,175 | Allstate | $2,885 |

| Eldorado Springs | $4,473 | Allstate | $2,416 |

| Elizabeth | $5,122 | Auto-Owners | $2,865 |

| Empire | $3,038 | Allstate | $1,736 |

| Englewood | $4,589 | State Farm | $2,689 |

| Erie | $4,169 | Allstate | $2,185 |

| Estes Park | $3,234 | State Farm | $1,885 |

| Evans | $4,449 | Allstate | $2,395 |

| Evergreen | $4,194 | Auto-Owners | $2,589 |

| Fairmount | $4,492 | State Farm | $2,512 |

| Fairplay | $2,836 | Allstate | $1,703 |

| Federal Heights | $4,406 | State Farm | $2,602 |

| Firestone | $4,072 | Allstate | $2,137 |

| Flagler | $5,423 | Allstate | $2,909 |

| Fleming | $5,436 | Allstate | $2,675 |

| Florence | $3,360 | Allstate | $1,828 |

| Florissant | $4,216 | Auto-Owners | $2,623 |

| Fort Carson | $4,727 | Allstate | $2,432 |

| Fort Collins | $3,782 | State Farm | $2,297 |

| Fort Garland | $2,751 | Shelter | $1,398 |

| Fort Lupton | $4,458 | Allstate | $2,153 |

| Fort Lyon | $5,199 | Allstate | $2,223 |

| Fort Morgan | $5,393 | Allstate | $2,536 |

| Fountain | $4,954 | Allstate | $2,501 |

| Fowler | $4,656 | Allstate | $2,223 |

| Foxfield | $4,910 | Auto-Owners | $2,791 |

| Franktown | $5,074 | Auto-Owners | $2,839 |

| Fraser | $2,522 | Shelter | $1,754 |

| Frederick | $4,097 | Allstate | $2,146 |

| Frisco | $2,279 | Travelers | $1,385 |

| Fruita | $1,814 | State Farm | $922 |

| Fruitvale | $1,783 | State Farm | $858 |

| Galeton | $4,593 | State Farm | $2,496 |

| Garden City | $4,550 | Allstate | $2,442 |

| Gardner | $3,612 | Allstate | $2,083 |

| Gateway | $1,977 | Farmers | $1,333 |

| Genesee | $4,573 | Auto-Owners | $2,637 |

| Genoa | $5,060 | State Farm | $2,512 |

| Georgetown | $3,028 | American Family | $1,911 |

| Gilcrest | $4,428 | Allstate | $2,376 |

| Gill | $4,736 | State Farm | $2,496 |

| Glade Park | $2,095 | Farmers | $1,306 |

| Glen Haven | $3,635 | Allstate | $2,088 |

| Glendale | $4,744 | Auto-Owners | $2,764 |

| Gleneagle | $4,857 | State Farm | $2,702 |

| Glenwood Springs | $2,103 | Travelers | $1,310 |

| Golden | $4,448 | Auto-Owners | $2,614 |

| Granada | $5,343 | Auto-Owners | $2,637 |

| Granby | $2,468 | State Farm | $1,748 |

| Grand Junction | $1,802 | State Farm | $923 |

| Grand Lake | $2,633 | State Farm | $1,685 |

| Grand View Estates | $5,035 | Auto-Owners | $2,712 |

| Granite | $2,354 | Shelter | $1,398 |

| Grant | $3,321 | American Family | $1,912 |

| Greeley | $4,489 | Allstate | $2,422 |

| Green Mountain Falls | $5,008 | Auto-Owners | $2,792 |

| Greenwood Village | $4,697 | Auto-Owners | $2,734 |

| Grover | $4,646 | State Farm | $2,496 |

| Guffey | $3,169 | Allstate | $1,807 |

| Gunbarrel | $4,131 | Allstate | $2,287 |

| Gunnison | $2,200 | Shelter | $1,398 |

| Gypsum | $2,000 | State Farm | $1,100 |

| Hamilton | $2,285 | Allstate | $1,596 |

| Hartman | $5,131 | State Farm | $2,526 |

| Hartsel | $2,960 | Allstate | $1,816 |

| Hasty | $5,589 | Auto-Owners | $2,631 |

| Haswell | $5,378 | Allstate | $2,435 |

| Haxtun | $5,526 | Allstate | $2,761 |

| Hayden | $2,224 | State Farm | $1,316 |

| Henderson | $4,562 | Allstate | $2,595 |

| Hereford | $4,714 | State Farm | $2,496 |

| Hesperus | $2,180 | State Farm | $996 |

| Highlands Ranch | $4,628 | Auto-Owners | $2,690 |

| Hillrose | $5,312 | State Farm | $2,516 |

| Hillside | $3,128 | Allstate | $1,667 |

| Hoehne | $4,221 | Allstate | $2,435 |

| Holly | $5,414 | Auto-Owners | $2,615 |

| Holly Hills | $4,627 | Auto-Owners | $2,751 |

| Holyoke | $5,790 | Allstate | $2,784 |

| Homelake | $2,317 | Shelter | $1,398 |

| Hooper | $2,249 | Shelter | $1,398 |

| Hot Sulphur Springs | $2,485 | Shelter | $1,754 |

| Hotchkiss | $2,003 | State Farm | $1,339 |

| Howard | $3,078 | Allstate | $1,575 |

| Hudson | $4,835 | Allstate | $2,478 |

| Hugo | $5,303 | Allstate | $2,608 |

| Hygiene | $3,881 | Allstate | $2,404 |

| Idaho Springs | $3,281 | State Farm | $2,388 |

| Idalia | $5,242 | State Farm | $2,524 |

| Idledale | $4,677 | State Farm | $2,474 |

| Ignacio | $2,028 | State Farm | $1,084 |

| Iliff | $5,232 | State Farm | $2,521 |

| Indian Hills | $4,501 | Auto-Owners | $2,642 |

| Inverness | $4,722 | Auto-Owners | $2,729 |

| Jamestown | $4,533 | Auto-Owners | $2,518 |

| Jaroso | $2,637 | Nationwide | $1,384 |

| Jefferson | $3,054 | Allstate | $1,612 |

| Joes | $5,394 | Auto-Owners | $2,656 |

| Johnstown | $4,299 | Allstate | $2,404 |

| Julesburg | $5,545 | Allstate | $2,381 |

| Karval | $5,098 | State Farm | $2,512 |

| Keenesburg | $4,945 | Allstate | $2,704 |

| Ken Caryl | $4,530 | Allstate | $2,621 |

| Kersey | $4,806 | Allstate | $2,644 |

| Keystone | $2,325 | Travelers | $1,385 |

| Kim | $4,357 | State Farm | $2,443 |

| Kiowa | $5,062 | Auto-Owners | $2,915 |

| Kirk | $5,289 | State Farm | $2,524 |

| Kit Carson | $5,397 | Allstate | $2,927 |

| Kittredge | $4,350 | Auto-Owners | $2,614 |

| Kremmling | $2,268 | State Farm | $1,442 |

| La Jara | $2,194 | State Farm | $1,355 |

| La Junta | $5,137 | Allstate | $2,409 |

| La Salle | $4,476 | Allstate | $2,428 |

| La Veta | $3,645 | Allstate | $2,018 |

| Lafayette | $4,267 | Allstate | $2,416 |

| Lake City | $2,015 | State Farm | $1,074 |

| Lake George | $3,557 | American Family | $1,994 |

| Lakewood | $4,551 | State Farm | $2,566 |

| Lamar | $5,681 | Allstate | $2,698 |

| Laporte | $3,809 | Auto-Owners | $2,327 |

| Larkspur | $4,777 | Allstate | $2,760 |

| Las Animas | $5,252 | Allstate | $2,444 |

| Lazear | $2,115 | Shelter | $1,398 |

| Leadville | $2,241 | Shelter | $1,348 |

| Leadville North | $2,238 | Shelter | $1,348 |

| Lewis | $2,092 | Farmers | $1,231 |

| Limon | $5,315 | Allstate | $2,530 |

| Lincoln Park | $3,277 | Allstate | $1,728 |

| Lindon | $5,286 | State Farm | $2,522 |

| Littleton | $4,587 | State Farm | $2,663 |

| Livermore | $3,819 | Auto-Owners | $2,219 |

| Lochbuie | $4,745 | Allstate | $2,595 |

| Log Lane Village | $5,303 | State Farm | $2,516 |

| Loma | $1,918 | State Farm | $1,082 |

| Lone Tree | $4,857 | Auto-Owners | $2,705 |

| Longmont | $4,151 | Allstate | $2,115 |

| Louisville | $4,307 | Allstate | $2,324 |

| Louviers | $4,564 | State Farm | $2,460 |

| Loveland | $3,791 | Auto-Owners | $2,150 |

| Lucerne | $4,569 | Allstate | $2,428 |

| Lyons | $4,210 | Auto-Owners | $2,470 |

| Mack | $2,105 | Farmers | $1,318 |

| Manassa | $2,237 | State Farm | $1,345 |

| Mancos | $1,989 | State Farm | $1,136 |

| Manitou Springs | $5,038 | Allstate | $2,686 |

| Manzanola | $5,207 | Auto-Owners | $2,635 |

| Marvel | $2,132 | Farmers | $1,208 |

| Masonville | $3,968 | Auto-Owners | $2,297 |

| Matheson | $5,388 | Allstate | $2,470 |

| Maybell | $2,636 | Farmers | $1,602 |

| Mc Clave | $5,097 | State Farm | $2,521 |

| Mc Coy | $2,124 | Shelter | $1,348 |

| Mead | $4,123 | Allstate | $2,009 |

| Meeker | $2,271 | State Farm | $997 |

| Meredith | $2,183 | Shelter | $1,348 |

| Meridian | $4,938 | Auto-Owners | $2,721 |

| Merino | $5,444 | State Farm | $2,521 |

| Mesa | $2,210 | Shelter | $1,348 |

| Mesa Verde National Park | $2,110 | Farmers | $1,208 |

| Milliken | $4,376 | Allstate | $2,398 |

| Minturn | $2,147 | Shelter | $1,348 |

| Model | $4,267 | State Farm | $2,443 |

| Moffat | $2,339 | Shelter | $1,398 |

| Molina | $2,057 | Shelter | $1,348 |

| Monarch | $2,531 | Shelter | $1,398 |

| Monte Vista | $2,176 | State Farm | $1,052 |

| Montrose | $1,882 | State Farm | $1,009 |

| Monument | $4,958 | Allstate | $2,542 |

| Morrison | $4,667 | Allstate | $2,536 |

| Mosca | $2,247 | Shelter | $1,398 |

| Mount Crested Butte | $2,015 | State Farm | $1,075 |

| Mountain View | $4,543 | State Farm | $2,597 |

| Mountain Village | $1,962 | Travelers | $1,183 |

| Nathrop | $2,201 | Shelter | $1,398 |

| Naturita | $2,221 | Shelter | $1,398 |

| Nederland | $4,303 | Auto-Owners | $2,383 |

| New Castle | $2,171 | Shelter | $1,348 |

| New Raymer | $4,743 | State Farm | $2,496 |

| Niwot | $4,091 | Allstate | $2,277 |

| North Washington | $4,517 | Allstate | $2,439 |

| Northglenn | $4,434 | Allstate | $2,324 |

| Norwood | $2,294 | Travelers | $1,183 |

| Nucla | $2,211 | State Farm | $1,078 |

| Nunn | $4,535 | Allstate | $2,535 |

| Oak Creek | $2,340 | Shelter | $1,754 |

| Ohio City | $2,178 | State Farm | $1,372 |

| Olathe | $1,911 | State Farm | $992 |

| Olney Springs | $4,881 | Allstate | $2,261 |

| Ophir | $2,142 | Travelers | $1,183 |

| Orchard | $5,117 | State Farm | $2,516 |

| Orchard Mesa | $1,808 | Nationwide | $1,018 |

| Ordway | $5,544 | Allstate | $2,607 |

| Otis | $5,535 | Allstate | $2,692 |

| Ouray | $1,983 | State Farm | $1,230 |

| Ovid | $5,562 | Allstate | $2,404 |

| Padroni | $5,261 | State Farm | $2,521 |

| Pagosa Springs | $2,115 | State Farm | $1,180 |

| Palisade | $1,873 | State Farm | $1,038 |

| Palmer Lake | $5,071 | State Farm | $2,476 |

| Paoli | $5,585 | State Farm | $2,521 |

| Paonia | $2,022 | State Farm | $1,169 |

| Parachute | $2,014 | Shelter | $1,348 |

| Paradox | $2,055 | Farmers | $1,328 |

| Paragon Estates | $4,130 | Allstate | $2,355 |

| Parker | $5,025 | Auto-Owners | $2,729 |

| Parlin | $2,152 | Shelter | $1,398 |

| Parshall | $2,476 | Allstate | $1,677 |

| Peetz | $5,381 | Auto-Owners | $2,755 |

| Penrose | $3,505 | Allstate | $1,783 |

| Perry Park | $4,840 | Allstate | $2,760 |

| Peyton | $5,240 | Auto-Owners | $2,828 |

| Phippsburg | $2,304 | Allstate | $1,677 |

| Pierce | $4,267 | Auto-Owners | $2,562 |

| Pine | $4,377 | Auto-Owners | $2,629 |

| Pine Brook Hill | $4,253 | Allstate | $2,311 |

| Pinecliffe | $4,008 | State Farm | $2,469 |

| Pitkin | $2,273 | Shelter | $1,398 |

| Placerville | $2,330 | Travelers | $1,183 |

| Platteville | $4,318 | Allstate | $2,117 |

| Pleasant View | $2,082 | Nationwide | $1,090 |

| Poncha Springs | $2,417 | Shelter | $1,398 |

| Ponderosa Park | $5,120 | Auto-Owners | $2,865 |

| Powderhorn | $2,107 | Shelter | $1,398 |

| Pritchett | $5,003 | State Farm | $2,522 |

| Pueblo | $4,886 | Allstate | $2,226 |

| Pueblo West | $4,753 | Allstate | $2,225 |

| Ramah | $4,982 | State Farm | $2,476 |

| Rand | $2,428 | Auto-Owners | $1,723 |

| Rangely | $2,254 | Farmers | $1,533 |

| Red Cliff | $2,234 | Shelter | $1,348 |

| Red Feather Lakes | $3,643 | Auto-Owners | $2,090 |

| Redlands | $1,902 | State Farm | $1,214 |

| Redvale | $2,129 | Shelter | $1,398 |

| Ridgway | $2,046 | State Farm | $1,147 |

| Rifle | $1,909 | State Farm | $927 |

| Rockvale | $3,395 | Allstate | $1,646 |

| Rocky Ford | $5,357 | Auto-Owners | $2,609 |

| Roggen | $4,715 | State Farm | $2,496 |

| Rollinsville | $3,511 | American Family | $1,861 |

| Romeo | $2,313 | Shelter | $1,398 |

| Roxborough Park | $4,684 | Auto-Owners | $2,707 |

| Rush | $5,271 | State Farm | $2,476 |

| Rye | $4,440 | Allstate | $2,199 |

| Saguache | $2,120 | State Farm | $1,278 |

| Salida | $2,219 | State Farm | $1,337 |

| Salt Creek | $4,953 | Allstate | $2,233 |

| San Luis | $2,615 | Shelter | $1,398 |

| Sanford | $2,210 | State Farm | $1,396 |

| Sargents | $2,518 | Shelter | $1,398 |

| Security-Widefield | $4,953 | Allstate | $2,448 |

| Sedalia | $4,880 | Auto-Owners | $2,695 |

| Sedgwick | $5,469 | State Farm | $2,520 |

| Seibert | $5,450 | Allstate | $2,786 |

| Severance | $4,195 | Allstate | $2,406 |

| Shaw Heights | $4,349 | Allstate | $2,238 |

| Shawnee | $3,484 | Allstate | $1,882 |

| Sheridan | $4,571 | State Farm | $2,669 |

| Sheridan Lake | $5,352 | State Farm | $2,521 |

| Sherrelwood | $4,581 | State Farm | $2,655 |

| Silt | $1,949 | State Farm | $1,162 |

| Silver Plume | $2,963 | Allstate | $1,708 |

| Silverthorne | $2,286 | Travelers | $1,362 |

| Silverton | $1,930 | State Farm | $1,111 |

| Simla | $5,317 | Allstate | $2,767 |

| Slater | $2,397 | Shelter | $1,754 |

| Snowmass | $2,129 | Shelter | $1,348 |

| Snowmass Village | $2,082 | State Farm | $1,177 |

| Snyder | $5,424 | Allstate | $2,545 |

| Somerset | $2,149 | Shelter | $1,398 |

| South Fork | $2,114 | State Farm | $1,150 |

| Springfield | $5,011 | Allstate | $2,725 |

| Steamboat Springs | $2,218 | Travelers | $1,348 |

| Sterling | $5,406 | Allstate | $2,597 |

| Stonegate | $5,023 | Auto-Owners | $2,712 |

| Stoneham | $4,826 | State Farm | $2,496 |

| Strasburg | $5,224 | Auto-Owners | $2,897 |

| Stratmoor | $4,994 | Allstate | $2,393 |

| Stratton | $5,749 | Allstate | $2,682 |

| Sugar City | $5,089 | State Farm | $2,508 |

| Sugarloaf | $4,243 | Auto-Owners | $2,513 |

| Superior | $4,295 | Allstate | $2,324 |

| Swink | $4,981 | State Farm | $2,510 |

| Tabernash | $2,485 | Shelter | $1,754 |

| Telluride | $1,945 | State Farm | $1,027 |

| The Pinery | $5,076 | Auto-Owners | $2,712 |

| Thornton | $4,448 | Allstate | $2,391 |

| Timnath | $3,674 | Auto-Owners | $2,363 |

| Todd Creek | $4,451 | Allstate | $2,372 |

| Toponas | $2,272 | Allstate | $1,677 |

| Towaoc | $1,951 | State Farm | $1,067 |

| Trinchera | $4,189 | Allstate | $2,298 |

| Trinidad | $3,967 | Allstate | $2,055 |

| Twin Lakes | $4,258 | Auto-Owners | $2,584 |

| Two Buttes | $4,982 | State Farm | $2,522 |

| Upper Bear Creek | $3,843 | American Family | $1,911 |

| Usaf Academy | $4,708 | Allstate | $2,542 |

| Vail | $2,088 | Shelter | $1,348 |

| Vernon | $5,420 | Auto-Owners | $2,667 |

| Victor | $3,888 | Allstate | $1,894 |

| Vilas | $4,624 | State Farm | $2,522 |

| Villa Grove | $2,261 | Shelter | $1,398 |

| Vona | $5,231 | State Farm | $2,528 |

| Walden | $2,444 | State Farm | $1,735 |

| Walsenburg | $3,774 | Allstate | $1,953 |

| Walsh | $5,182 | Auto-Owners | $2,612 |

| Ward | $4,255 | Auto-Owners | $2,458 |

| Watkins | $4,878 | Allstate | $2,742 |

| Welby | $4,497 | Allstate | $2,439 |

| Weldona | $5,291 | Allstate | $2,637 |

| Wellington | $3,900 | Allstate | $2,357 |

| West Pleasant View | $4,501 | State Farm | $2,505 |

| Westcliffe | $3,335 | American Family | $1,865 |

| Westminster | $4,402 | Allstate | $2,396 |

| Weston | $3,913 | State Farm | $1,948 |

| Wetmore | $3,810 | Allstate | $2,254 |

| Wheat Ridge | $4,521 | State Farm | $2,570 |

| Whitewater | $1,934 | State Farm | $976 |

| Wiggins | $5,341 | Allstate | $2,882 |

| Wild Horse | $5,240 | State Farm | $2,522 |

| Wiley | $5,484 | Allstate | $2,647 |

| Windsor | $4,181 | Allstate | $2,406 |

| Winter Park | $2,578 | Shelter | $1,754 |

| Wolcott | $2,178 | Shelter | $1,348 |

| Woodland Park | $3,998 | Allstate | $2,630 |

| Woodmoor | $4,931 | Allstate | $2,542 |

| Woodrow | $5,055 | State Farm | $2,522 |

| Woody Creek | $2,249 | Shelter | $1,348 |

| Wray | $5,450 | Allstate | $2,593 |

| Yampa | $2,220 | State Farm | $1,339 |

| Yellow Jacket | $2,051 | State Farm | $1,034 |

| Yoder | $5,327 | Allstate | $2,847 |

| Yuma | $5,790 | Allstate | $2,715 |

Rates are for a policy with $350,000 of dwelling coverage.

What home insurance coverage do I need in Colorado?

Colorado homeowners need to make sure their homes are protected against hail, wildfires, theft and vandalism.

A standard home insurance policy typically covers these types of damage. But you may want to upgrade your coverage to make sure you're fully protected.

Does Colorado home insurance cover hail damage?

Hail is the No. 1 cause of damage to homes in Colorado. Home insurance almost always pays for damage caused by hail. This can include damage to your roof, siding and windows, as well as any leaks that may have resulted from hail damage.

However, most home insurance companies don't pay for hail damage that's only cosmetic. So if hail dents your siding but doesn't cause a leak, your insurance company probably won't pay to replace it.

If you're worried about hail damage, American Family offers a number of coverage add-ons to upgrade your protection.

- American Family's roof damage coverage pays the full cost to replace your roof, even if it's older or had wear and tear before it was damaged. In comparison, most home insurance policies pay based on your roof's current value, which may not be enough to fully cover the cost of a new roof.

- The company also offers matching undamaged siding coverage. So if only a portion of your siding is damaged, American Family will pay extra to replace all of your siding if you can't find matching materials. This is especially helpful if you want to preserve your curb appeal.

- American Family also offers hidden water damage coverage, which could be helpful if hail causes a leak but you don't find it right away. Most home insurance policies have a time limit on leaks, so if water is causing unseen damage for a few months before you find out, it may not be covered.

Is wildfire damage covered by home insurance in CO?

Homeowners insurance typically includes wildfire coverage. However, your insurance company may not offer coverage for wildfires if you live in a high-risk area.

If your homeowners insurance doesn't include wildfire coverage, consider buying a separate wildfire insurance policy

Nearly 19% of structures in Colorado have a moderate to extreme risk for wildfire damage. Together these structures would cost around $141 billion to rebuild.

The counties with the highest wildfire risk in Colorado are:

- Gilpin

- Clear Creek

- Park

- Custer

- Hinsdale

If you live in an area with a very high risk for wildfires, you may have trouble getting even the most basic home insurance coverage. In that case, you can apply for a policy from the Colorado FAIR Plan. As the state's "insurer of last resort," the FAIR plan offers policies to people who can't get coverage elsewhere.

Does home insurance cover theft and vandalism in Colorado?

Colorado has the second-highest property crime rate in the U.S., which includes theft and vandalism. Homeowners insurance usually covers property crime.

However, if you have expensive items such as valuable jewelry, firearms, sports equipment or artwork, you should consider getting extra coverage for those items. That way, your insurance company will pay enough for you to fully replace those items if something happens to them.

Pueblo and Denver both rank in the top 15 for highest property crime rates among large U.S. cities .

If you live in either of these cities, you should consider taking extra steps to protect your home, such as an alarm system that contacts a call center in an emergency. Many home insurance companies offer a discount when you install a monitored alarm, so it may also save you money on your home insurance bill.

Tips for getting cheaper home insurance in Colorado

You can lower your Colorado home insurance rates by shopping around, finding discounts and raising your deductible.

It's important to compare rates when shopping for home insurance. For example, you could save more than $4,000 per year by switching from the most expensive home insurance in Colorado, Farmers, to the cheapest home insurance, Allstate.

Many companies offer discounts that can lower your monthly home insurance rate. The number and type of discounts will differ from company to company, but common discounts include home-auto bundling, discounts for installing safety systems such as burglar and fire alarms, and paperless billing discounts when you pay online.

Before your home insurance coverage starts, you'll need to pay a certain amount of money toward your home repairs, called a deductible. You can adjust your deductible up or down when you buy a policy. If you set a higher deductible, you'll pay a lower monthly rate.

Keep in mind, you're responsible for paying your entire deductible. You should never set your deductible higher than what you can easily afford to pay from your savings account.

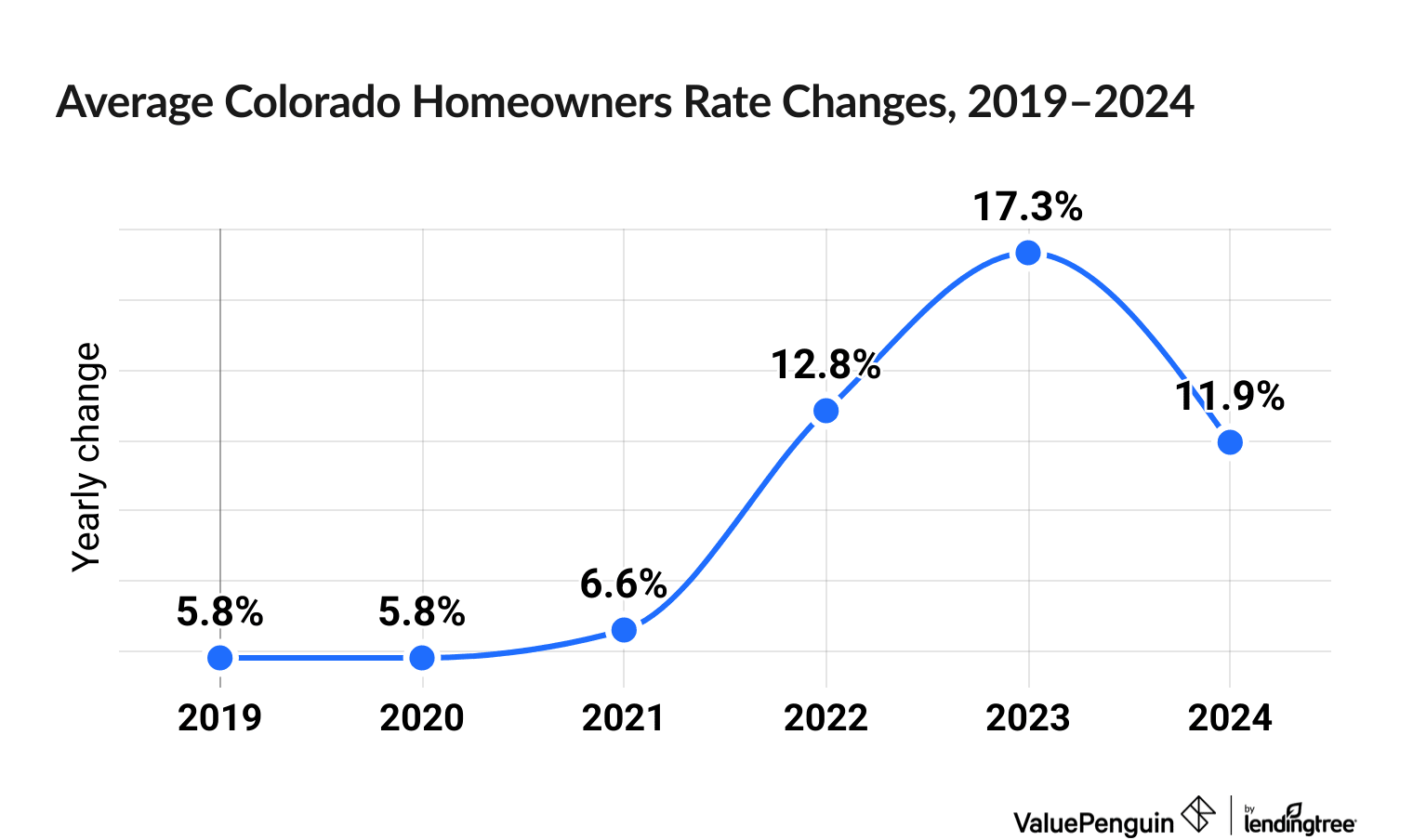

How has the cost of Colorado home insurance changed over time?

Home insurance rates in Colorado rose nearly 89% over the last five years.

Colorado homeowners have experienced substantial jumps in their home insurance rates, with an average increase of nearly 17% in 2025 and 15% in 2024.

Home insurance rate increases in Colorado, 2021–2025

Year | Rate increase |

|---|---|

| 2021 | 6.59% |

| 2022 | 12.43% |

| 2023 | 16.65% |

| 2024 | 15.30% |

| 2025 | 16.96% |

Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

Five companies more than doubled their home insurance rates in Colorado over the last five years: Progressive (154%), Liberty Mutual (139%), Nationwide (128%), Auto-Owners (114%) and American Family (102%).

Chubb has had the smallest rate increase over that time period, at just less than 42%.

Frequently asked questions

How much is the average house insurance in Colorado?

The average homeowners policy in Colorado costs $4,310 per year. That's 80% more than the national average of $2,395 per year.

Who has the most affordable homeowners insurance in Colorado?

Allstate has the most affordable homeowners insurance in Colorado. You'll pay $2,487 on average per year for $350,000 of dwelling coverage, which is 42% less than the Colorado state average.

What is the best homeowners insurance company in Colorado?

Auto-Owners, Allstate and State Farm are the best home insurance companies in Colorado. But the best company for you will depend on your priorities. For example, you should consider Allstate if you want the best rate, while Auto-Owners is a better choice if customer service tops your list of must-haves.

Why is Colorado homeowners insurance so expensive?

Colorado homes are at a high risk of damage from a variety of natural disasters, including hail, severe storms and wildfires, which raises rates. In addition, the rising cost of labor and materials in recent years has increased the cost of home repairs.

Methodology

To find the best homeowners insurance in Colorado, ValuePenguin collected quotes from the top companies across every residential ZIP code in the state. Rates are for a 45-year-old married man with no prior insurance claims. Quotes are for a 2,464-square-foot home built 42 years ago, based on the average home age and size in Colorado.

Quotes include the following coverage limits:

- Dwelling coverage: $200,000, $350,000, $500,000 or $1 million

- Personal liability: $100,000

- Medical payments: $1,000

- Deductible: $1,000

Insurance rate data from Quadrant Information Services was used in this analysis. Quadrant's rates were taken from public filings and should be used for comparative purposes only.

The National Association of Insurance Commissioners (NAIC), the J.D. Power customer satisfaction survey and ValuePenguin's ratings were used when creating home insurance company ratings.

Sources:

About the Author

Senior Writer

Lindsay Bishop is a Senior Writer at ValuePenguin, where she educates readers about home, auto, renters, flood and motorcycle insurance.

Lindsay began her career in the insurance and financial industry in 2010. She was a licensed auto, home, life and health insurance agent and held Series 6 and 63 financial licenses.

After a hiatus from the financial sector, Lindsay returned to the industry as a content writer for ValuePenguin in 2021. She enjoys having the opportunity to help readers make smart decisions about their insurance so they can be prepared for anything life throws their way.

When Lindsay isn't writing about insurance, you can find her spending time with family, enjoying the outdoors on Sunday long runs or riding her Peloton.

How insurance helped Lindsay

As a homeowner for 15 years located in South Carolina, Lindsay has plenty of experience navigating the coastal insurance market and managing the claims process. That includes successfully negotiating a full roof replacement claim.

Expertise

- Home insurance

- Car insurance

- Flood insurance

- Renters insurance

- Motorcycle insurance

Referenced by

- CNBC

- Yahoo Finance

- Miami Herald

Education

- BS/BA Economics, University of Nevada Las Vegas

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.