How Does Personal Injury Protection Work in Minnesota?

Personal injury protection (PIP) is a mandatory form of car insurance for drivers in Minnesota. PIP pays for your own costs relating to... Read More

Compare life insurance quotes and find the best rates for a policy.

Life insurance can help protect your family financially if anything happens to you, but it’s important to make sure you’re not overpaying for the coverage you need.

Life insurance is a planning tool that provides financial protection for your dependents.

The asset provides a tax-free lump sum of money which is paid to your dependent after your death. Typically, life insurance is bought so that your dependents would be able to sustain payments for bills, college tuition or other after-life expenses.

Key components of life insurance policies are:

Every individual has a different financial situation and therefore will require different life insurance needs.

When calculating your needs you should consider what the life insurance will be used for and why you may need life insurance in general.

If you are young and do not have any dependents then buying life insurance may not be a necessary purchase at this point in your life. On the other hand, if you are starting a family in which the financial livelihood of the family relies on your salary, then you may want to consider purchasing some life insurance coverage and calculate your future needs.

When beginning to calculate how much life insurance you need, you should start by adding up your current and future financial obligations. This can include obligations such as:

After you have figured out your obligations, you can add up your current assets such as savings and college funds. Finally, by subtracting your current assets from the obligations you will arrive at a target amount for how much life insurance you will need. It is important to note that this is a rough estimate for coverage and it may be useful to purchase slightly more life insurance to compensate for unexpected financial situations that your dependents might face.

Life insurance companies will typically offer two different types of life insurance: term life insurance and permanent life insurance.

A term policy will last for a set period of time before expiring while permanent plans stay in effect for your entire life. Furthermore, some permanent life insurance policies will have a cash value component that will grow as you make premium payments.

Term life insurance | Permanent life insurance | |

|---|---|---|

| Period of coverage | Specified term, usually one to 30 years | Lifelong |

| Cash value | No | Yes |

| Average monthly premium | Cheap | Expensive |

Depending on your situation and what the purpose of your life insurance is, the type of life insurance that you need will change.

For example, if you are looking for a cheap policy to cover future financial obligations like college tuition, then choosing a term life insurance policy with a death benefit that matches the total tuition may be the best option. On the other hand, say you have Type 1 diabetes and have had problems with getting approved for life insurance. In this case, a permanent policy like guaranteed acceptance life insurance may be a better option for coverage.

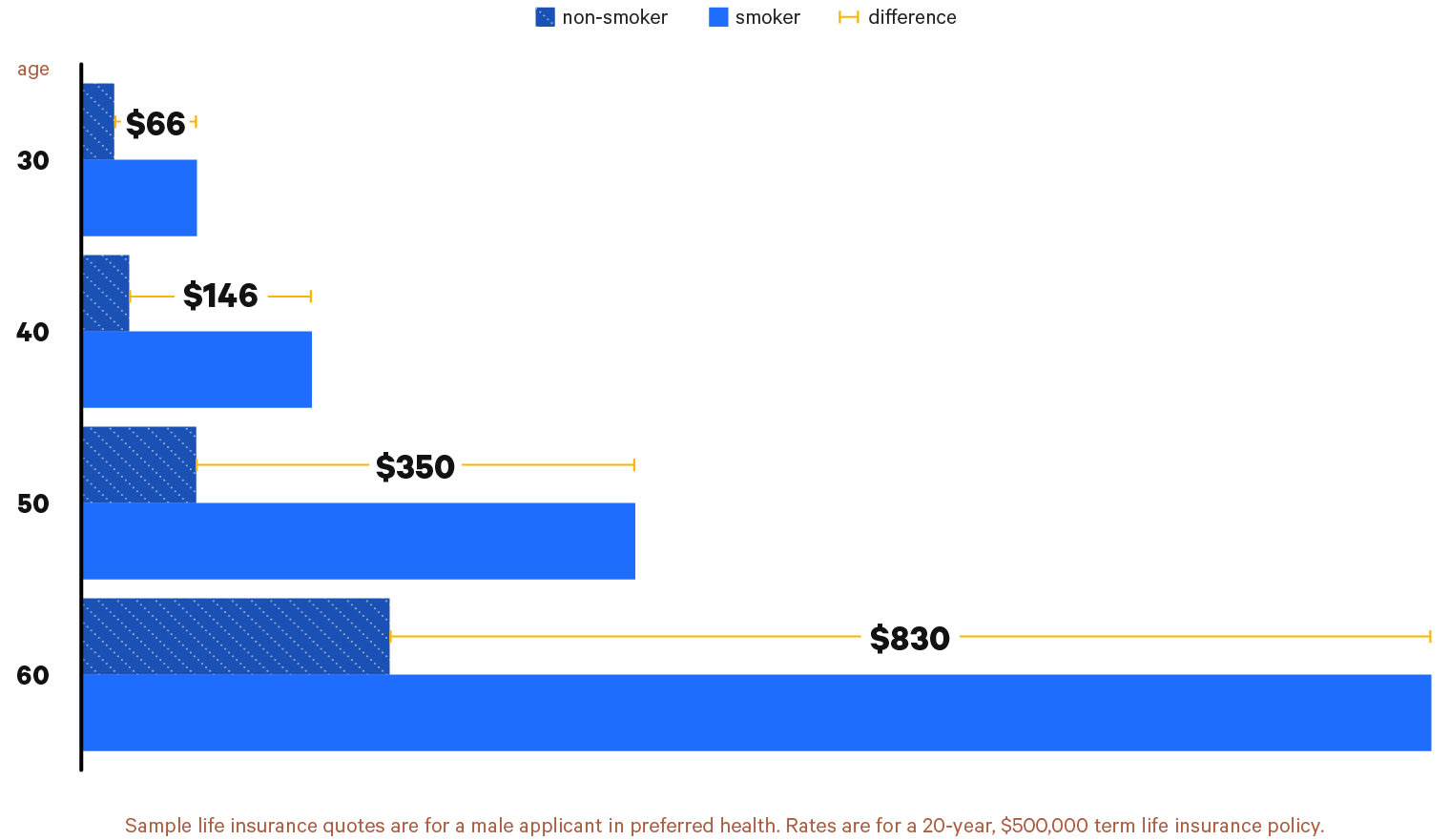

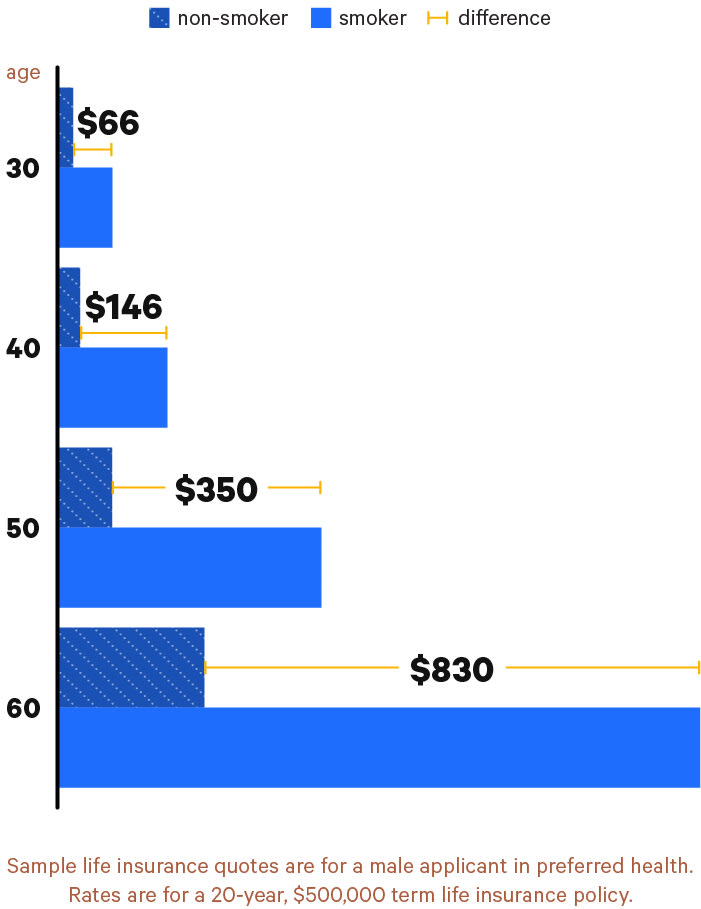

The cost of your life insurance policy will be dependent on a variety of factors including your health, age, occupation and if you smoke. However, the largest determinant will be if you are a smoker.

Smokers will have an average cost of life insurance that is 306% higher when compared to a nonsmoker.

Find Cheap Life Insurance Quotes in Your Area

When searching for the best cheap life insurance we would recommend getting life insurance quotes from as many insurers as possible. To aid you in this process we have provided detailed reviews of some of the best life insurance companies in the industry.

You will notice that many life insurance providers will have favorable underwriting requirements for certain individuals. For example, if you smoke you may find that Northwestern Mutual will have some of the best smoker life insurance rates available. Additionally, some insurers will specialize in certain products such as Mutual of Omaha which has one of the cheapest guaranteed whole life insurance products in the industry.

Personal injury protection (PIP) is a mandatory form of car insurance for drivers in Minnesota. PIP pays for your own costs relating to... Read More

All auto insurance companies in Washington State are required to offer at least $10,000 of personal injury protection (PIP) insurance to... Read More

Personal injury protection isn't mandatory in Maryland, but you will have to provide PIP insurance coverage for any guests riding in your... Read More

Personal injury protection (PIP) insurance is required for all drivers in Oregon and must provide at least $15,000 of coverage per person... Read More

Your license and registration may be suspended if you drive without insurance in Arizona.... Read More

Full coverage car insurance costs $611 per month for a 17-year-old, on average. State Farm usually has the cheapest rates for 17-year-old... Read More

Drivers in Delaware are required to carry personal injury protection (PIP) coverage as part of their auto insurance policy. PIP insurance... Read More

Private placement life insurance (PPLI) is for wealthy people who want to invest in hedge funds but avoid the high tax rates that come with... Read More

If you fail to maintain auto insurance on a vehicle registered in your name, your license and registration may be suspended.... Read More

License and registration suspensions can occur in Maryland for committing serious driving violations, such as driving without insurance or... Read More

Utah requires all car owners to carry personal injury protection (PIP) insurance, which pays for medical costs, lost income and other... Read More

Driving without auto insurance is a misdemeanor offense in Georgia, which could result in the suspension of your registration and license,... Read More