Life Insurance

83 Million Americans Say Coronavirus Makes Them More Likely to Buy Life Insurance

The coronavirus pandemic has had a deep impact on everything from the larger economy to daily life. For many, it has exposed a lack of financial preparation for emergencies, and according to a recent ValuePenguin survey of over 1,000 U.S. adults, it has driven more interest in life insurance coverage.

Key findings

- While 25% are more likely to get life insurance as a result of the coronavirus, the answer differed significantly by gender: 38% of men said they would be more likely to buy life insurance now, verses just 14% of women.

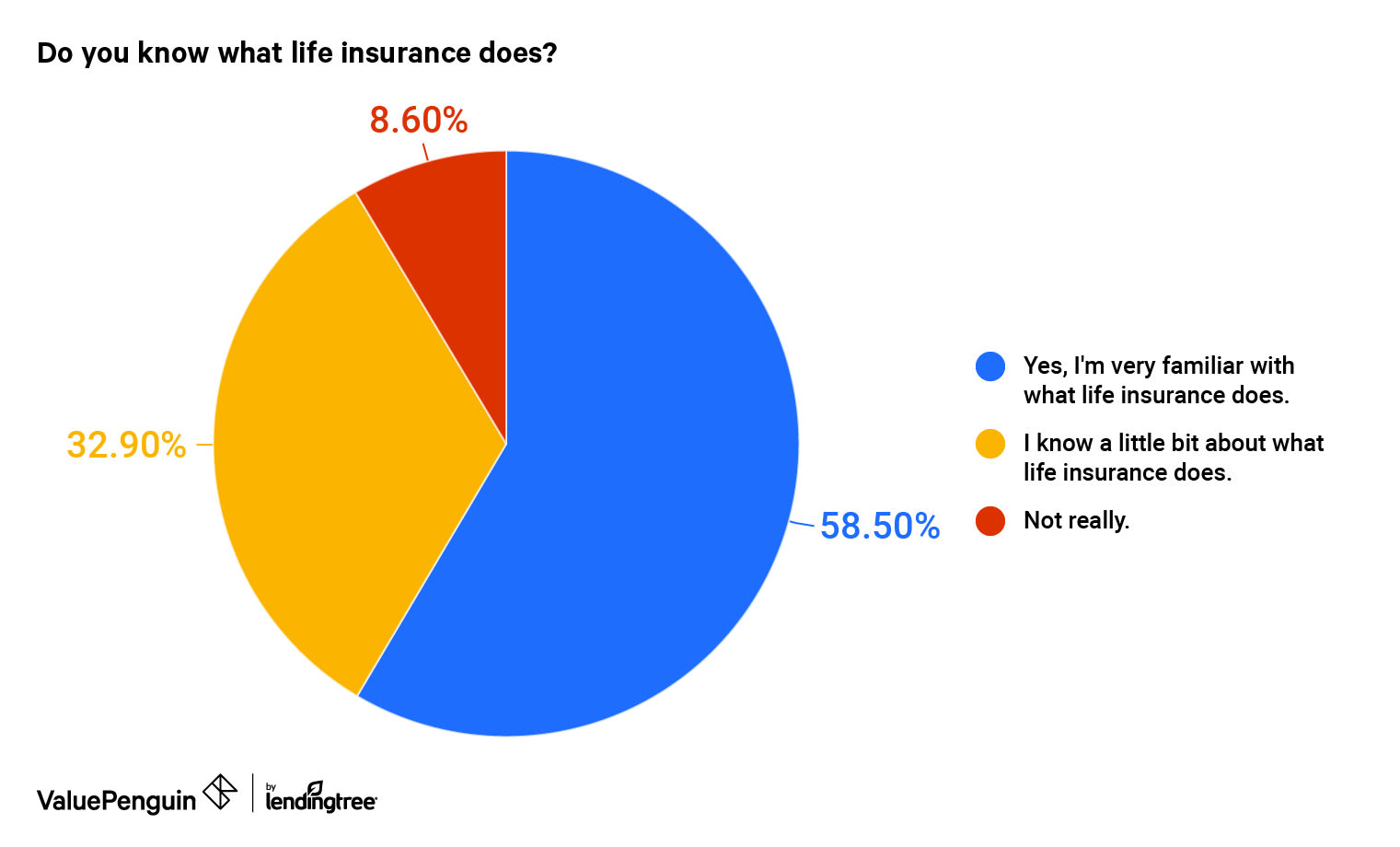

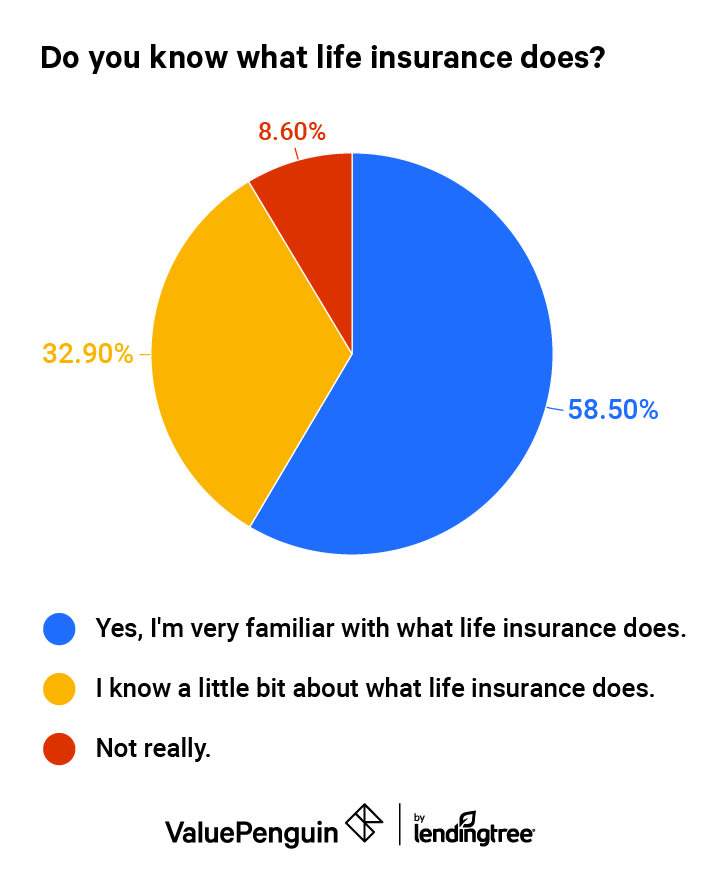

- While a majority of people have active life insurance, only 3 in 5 are "very familiar" with what it does. When asked whether they knew what life insurance does, 33% said they only know "a little bit," while 9% said "not really."

- More than 30% don't know how much life insurance an individual needs and most other respondents came in with estimates that were almost certainly too low for a typical scenario.

- The amount and type of life insurance that's best for you depends on a number of personal factors. The first step is determining the financial obligations you want to cover, like college tuition for your kids or mortgage debt.

1 in 4 say COVID-19 increased their interest in life insurance

When asked whether the pandemic had influenced their likelihood of getting life insurance, 25% of consumers said it had made them more likely to get coverage, however men were far more likely to respond this way. About 69% of those who responded positively were men, while only 14% of women said they were more likely to get coverage due to the pandemic.

The differences between men and women may be caused by several contributing factors. One possible explanation is based on the idea of the "breadwinner" needing a life insurance policy. While an increasing number of women are assuming the role of primary income earner for their households, 59% of U.S. households still have a male family member earning at least half the household's income.

Another finding of our survey was the difference between current policyholders and those without coverage. People who already had life insurance policies were more likely to say they would increase their insurance because of the pandemic (39%) than those with no coverage( 20%).

Most people already have some life insurance, but many aren't sure what it actually does

The survey results suggested more people want life insurance because of COVID-19, but also revealed that a considerable number of people don't have much information about how life insurance policies work. While 65% of all respondents said they already had life insurance in place, only about 60% were "very familiar" with what life insurance does.

Meanwhile, 33% of people professed to "know a little bit" while 9% said they don't really know what life insurance does. This relative lack of knowledge may be problematic, given the variety of policy types and benefits that make up the life insurance industry.

For example, the two most popular types of life insurance — term life and whole life insurance — differ widely in their pricing and benefits. Consumers must be informed about such differences in order to find the coverage that best fits their individual needs.

Consumers puzzle over how much life insurance is necessary

One of the most common questions regarding life insurance is how to calculate the proper amount of coverage. When asked how much life insurance is typically enough, 30% of consumers had no idea, while only 10% cited the common rule of thumb that coverage should be equal to 10 times your annual salary.

However, even that rule of thumb is often insufficient for an accurate estimate of a person's life insurance needs. Ultimately, the amount of coverage you have should be enough to meet all of your future financial obligations, minus the assets that would be liquidated on your passing.

Consider the example of a married homeowner with young children. In the event of an untimely death, the surviving spouse would potentially be left to shoulder at least three ongoing financial obligations:

- Monthly mortgage payments

- The cost of care and education for the children, including college tuition

- The cost of maintaining the family's standard of living (on a single income)

This list also excludes the one-time cost of a funeral, which could run up to $10,000. Calculating these needs may be uncomfortable, but its important for an individual to realistically gauge their life insurance coverage needs in order to minimize the financial difficulties their family could face.

How you can get started with life insurance

At ValuePenguin, we're keenly interested in the way insurance operates and how everyday consumers can get the best value out of their coverage. That's why we've done our best to clarify some of the common points of confusion identified in the survey.

How much does life insurance cost?

The average cost of life insurance depends on your personal details, the type of policy and how much coverage you're getting.

As a baseline example, we've found that a $500,000 term life policy lasting 20 years would cost an average of $30 per month for a 35-year-old nonsmoker. Note that whole life insurance tends to be on the pricier side because it lasts your entire life and can also build cash value over time.

What kind of life insurance policy should I get?

In most cases, we find that term life insurance is the most affordable and convenient way to obtain effective coverage. Unlike whole life policies and other types of permanent life insurance, a term life policy will not last forever. But it will last long enough to cover costs that eventually wind down, such as a mortgage or a child's college tuition.

How do I calculate my life insurance needs?

Calculating how much coverage you need leads to a unique result for each person. Some may want life insurance to cover the cost of supporting their children until adulthood, while others may also want to make sure their spouse receives support well into retirement.

At minimum, adding up the following:

- 1. The lifetime cost of your current financial obligations, including mortgage and other payments on jointly held debt.

- 2. The total cost of child care until your children reach adulthood, along with the amount you plan to contribute to their college education.

- 3. Subtract the value of your brokerage accounts, savings accounts and any existing life insurance policies, since these assets can be liquidated to cover your family's needs on top of the payout from your new life insurance policy.

Methodology

ValuePenguin commissioned Qualtrics to conduct an online survey of 1,136 U.S. adults, with the sample base proportioned to represent the overall population. The survey was fielded between May 5, 2020 and May 8, 2020.

About the Author

Insurance Analyst

Chris Moon is a former Product Manager for ValuePenguin with years of experience in addressing critical questions about mortgages and homeowners insurance. He spends his time evaluating insurance providers and policy features to understand where consumers might find the most cost-effective coverage. Chris has contributed insights to the New York Times and many other publications.