A West Coast Renter’s Guide to Affordable Living

Renting can provide people with many benefits like more flexibility and less maintenance responsibility. While it sometimes seems like a less savvy investment, as long as renters are also investing in other areas, it can be a fine long-term financial decision. Yet, renting was found to be unaffordable across 60% of the largest cities in each state. So where is renting the most affordable across the west coast?

West Coast State Affordability: Ranked Most to Least Affordable

Rank | State | Population | Renter affordability ratio |

|---|---|---|---|

| 1 | Wyoming | 563,626 | 25.58% |

| 2 | Utah | 2,763,885 | 28.29% |

| 3 | Montana | 989,415 | 28.50% |

| 4 | Idaho | 1,567,582 | 29.70% |

| 5 | Nevada | 2,700,551 | 30.11% |

| 6 | Washington | 6,724,540 | 31.17% |

| 7 | Colorado | 5,029,196 | 32.41% |

| 8 | Oregon | 3,831,074 | 32.67% |

| 9 | California | 37,253,956 | 35.38% |

With more people renting and the costs of rental properties increasing, it is important to seek affordable housing options. Remember, as a standard, when housing expenses exceed 30% of a person's income, they are considered burdened. ValuePenguin utilized this home affordability metric to determine which large cities in the West were most and least affordable to renters.

Key findings:

- Across the west, Colorado and Washington have seen the largest overall growth in annual rental housing costs in 2017, with both states increasing 6% year over year, respectively.

- Californians contribute the most of their salary to housing, with the average renter spending 35% of their income on housing. On the other hand, Wyoming renters are spending the least annually, on average just 26% of their income on housing.

- Sixty percent of large west coast cities were deemed unaffordable to renters, as they contribute over 30% of their income to rent annually.

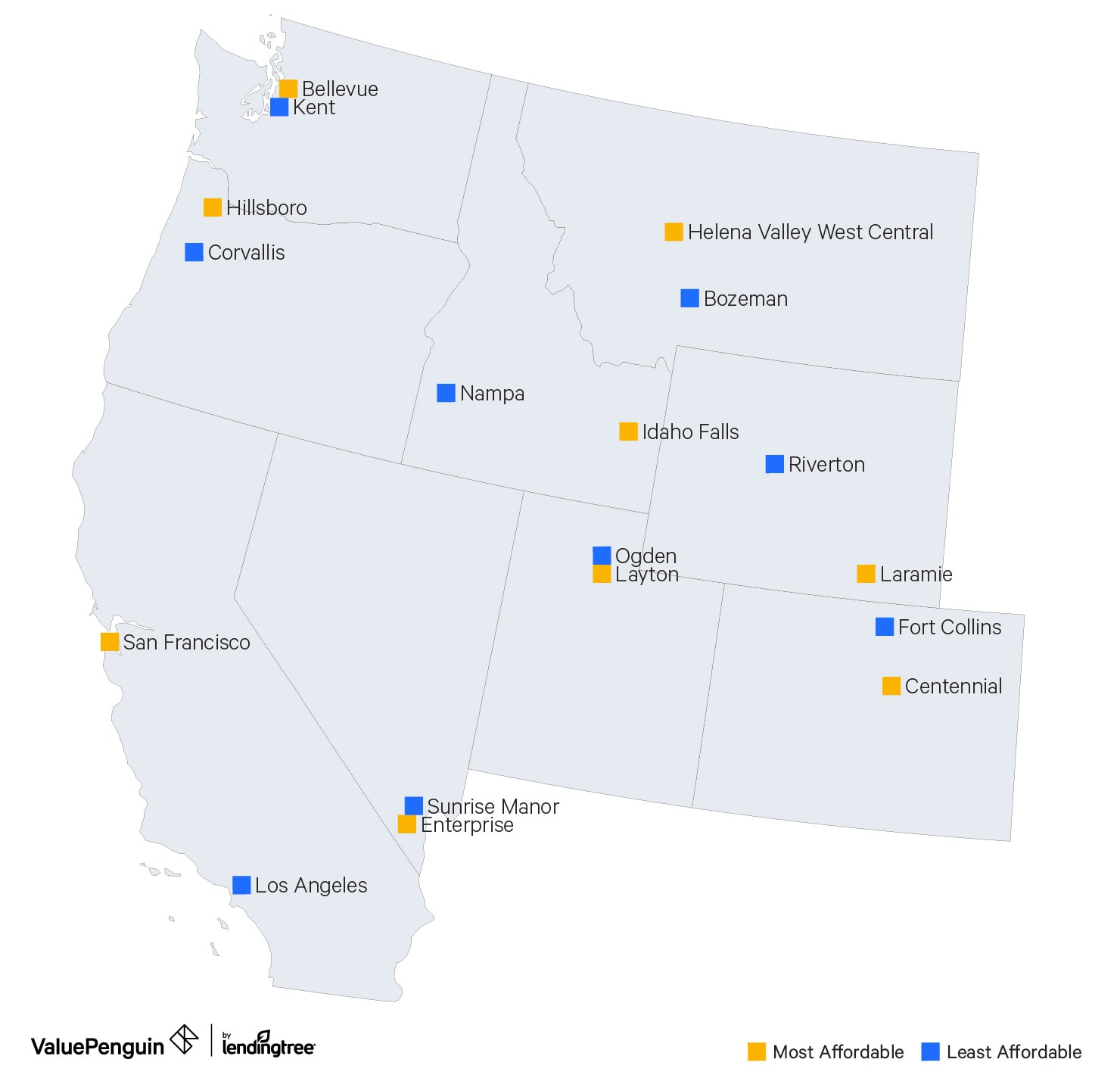

- Helena Valley West Central, Riverton and Green River, Wyoming, accounted for three of the five most affordable towns for renters in the West Coast.

- Corvallis, Eugene and Gresham, all located in Oregon, were the three most unaffordable cities for renters in the West Coast.

Which west coast towns are affordable in each state?

California:

Average renter spent 35% of income on housing

- There are many rumors as to the unaffordability of San Francisco, and San Franciscans were found to pay more on rent than other large California cities (average of $1,709 monthly or $20,508 annually). However, renters here also have the highest annual income at $76,386, which is more than double the average Fresno renter’s income. Due to this, San Francisco residents only pay 27% of their annual income on housing.

- In Los Angeles, the largest city in California, renters contribute 39% of their income to housing, which equates to an average of $15,624 annually. Our analysis also revealed that LA was one the most unaffordable cities in the entire West Coast for renters.

Oregon:

Average renter spent 33% of income on housing

- Hillsboro, located just 15 miles west of Portland, is the most affordable large city for renters in Oregon. Here, residents only contributed 26% of their annual income, or less than $15,000, on their home.

- While Corvallis renters spent only $973 a month on housing, they actually contribute 42% of their income annually, making it the least affordable city in Oregon for renters and in the entire West Coast.

Colorado:

Average renter spent 32% of income on housing

- The most affordable city in Colorado is situated 15 miles southeast of Denver. Centennial renters contribute just 28% of their income to housing.

- Fort Collins ranked most unaffordable city in Colorado and also fourth most unaffordable city in the West Coast, with residents spending 39% on their home annually.

Washington:

Average renter spent 31% of income on housing

- Seperated from Seattle by Lake Washington, Bellevue was the most affordable city for renters, with residents spending only 25% on housing annually. However, renters spent the most on monthly housing ($1,741), which was offset by their high income.

- Just south of Bellevue, Kent was the least affordable city, as renters here are spending 35% of their income on housing.

Idaho:

Average renter spent 30% of income on housing

- Idaho Falls renters spend $8,484 annually on housing, which equates to 27% of residents’ annual income, making this the most affordable city in Idaho.

- The least affordable city, Nampa, has renters spending 33% of their income on housing annually.

Nevada:

Average renter spent 30% of income on housing

- Southwest of Las Vegas, Enterprise is the most affordable city in Nevada, with residents spending just 26% of their income on rental housing annually. Enterprise renters have an average income of $62,238 — nearly double that of least affordable Sunrise Manor.

- Just 20 miles northeast of Enterprise, Sunrise Manor was the least affordable for renters. Renters here pay 34% of their income towards rent, though they pay nearly $6,000 less annually than most affordable Enterprise.

Montana:

Average renter spent 29% of income on housing

- Renters in Helena Valley West Central, the most affordable city, have the highest annual income in Montana ($58,938); renters here contribute just 19% to housing. This is the most affordable city for renters across the entire West Coast.

- While Bozeman residents have a lower annual income than Helena Valley West Central, renters here spend 33% of their income, or $11,472, on housing annually.

Utah:

Average renter spent 29% of income on housing

- Only 15 miles separates the most and least expensive cities, both of which are located north of Salt Lake City. Layton residents spend 24% of their income on housing annually, which is the lowest of all Utah’s large cities.

- In Ogden, on the other hand, renters spend just over the recommended threshold, contributing 31% of their income to housing.

Wyoming:

Average renter spent 26% of income on housing

- Riverton ranks as the most affordable city in Wyoming and second most affordable in the West Coast. Here, renters pay just 23% of their income, or $8,892, on housing annually. Two other Wyoming cities, Green River and Gillette, also rank as third and fifth most affordable across the west.

- Situated 50 miles outside of Cheyenne, Laramie is Wyoming’s least affordable city. Here, renters spend 36% on housing annually.

Contributing factors that determine renter affordability

When determining where you can live affordably, renters should also include how much it would cost to protect personal belongings. Nationally, renters insurance in the U.S. costs an average of $187 annually. In the Western states analyzed, the average renters insurance policy was 11% below the national average, priced at just $168 annually.

Montana and Utah had the most affordable renters insurance among Western states, priced at just $145 annually. California had the most expensive renters insurance, averaging $207 annually.

Large west coast towns ranked as most affordable to least affordable

Rank | City | State | Annual household income | Annual rental housing costs | Renter affordability ratio |

|---|---|---|---|---|---|

| 1 | Helena Valley West Central | MT | $58,938 | $11,052 | 18.75% |

| 2 | Riverton | WY | $38,889 | $8,892 | 22.87% |

| 3 | Green River | WY | $39,821 | $9,432 | 23.69% |

| 4 | Layton | UT | $46,384 | $11,112 | 23.96% |

| 5 | Gillette | WY | $46,339 | $11,136 | 24.03% |

| 6 | Jackson | WY | $63,845 | $15,504 | 24.28% |

| 7 | Bellevue | WA | $84,155 | $20,892 | 24.83% |

| 8 | Casper | WY | $41,040 | $10,248 | 24.97% |

| 9 | Enterprise | NV | $62,238 | $16,332 | 26.24% |

| 10 | Hillsboro | OR | $57,054 | $14,988 | 26.27% |

| 11 | Millcreek | UT | $44,944 | $11,868 | 26.41% |

| 12 | Rock Springs | WY | $40,973 | $10,872 | 26.53% |

| 13 | Orem | UT | $42,423 | $11,364 | 26.79% |

| 14 | San Francisco | CA | $76,386 | $20,508 | 26.85% |

| 15 | Miles City | MT | $32,708 | $8,844 | 27.04% |

| 16 | Sheridan | WY | $35,217 | $9,540 | 27.09% |

| 17 | Sandy | UT | $53,121 | $14,424 | 27.15% |

| 18 | Idaho Falls | ID | $31,106 | $8,484 | 27.27% |

| 19 | Centennial | CO | $67,376 | $18,648 | 27.68% |

| 20 | Post Falls | ID | $40,710 | $11,340 | 27.86% |

| 21 | Cheyenne | WY | $37,408 | $10,476 | 28.00% |

| 22 | West Jordan | UT | $49,691 | $14,016 | 28.21% |

| 23 | Sparks | NV | $42,119 | $11,964 | 28.41% |

| 24 | Helena | MT | $33,529 | $9,564 | 28.52% |

| 25 | Carson City | NV | $36,181 | $10,416 | 28.79% |

| 26 | Caldwell | ID | $32,912 | $9,480 | 28.80% |

| 27 | Henderson | NV | $49,314 | $14,208 | 28.81% |

| 28 | Spring Valley | NV | $45,532 | $13,152 | 28.89% |

| 29 | Havre | MT | $27,024 | $7,848 | 29.04% |

| 30 | Coeur d'Alene | ID | $36,410 | $10,584 | 29.07% |

| 31 | Evanston | WY | $26,526 | $7,716 | 29.09% |

| 32 | Billings | MT | $33,995 | $9,912 | 29.16% |

| 33 | Lewiston | ID | $27,852 | $8,208 | 29.47% |

| 34 | Reno | NV | $36,834 | $10,872 | 29.52% |

| 35 | Helena Valley Southeast | MT | $35,226 | $10,464 | 29.71% |

| 36 | Great Falls | MT | $26,533 | $7,956 | 29.99% |

| 37 | West Valley City | UT | $40,786 | $12,240 | 30.01% |

| 38 | Beaverton | OR | $46,645 | $14,064 | 30.15% |

| 39 | Meridian | ID | $40,435 | $12,192 | 30.15% |

| 40 | Salt Lake City | UT | $35,056 | $10,572 | 30.16% |

| 41 | Seattle | WA | $54,700 | $16,524 | 30.21% |

| 42 | Salem | OR | $33,844 | $10,332 | 30.53% |

| 43 | Twin Falls | ID | $29,730 | $9,084 | 30.55% |

| 44 | Kalispell | MT | $29,355 | $8,988 | 30.62% |

| 45 | Vancouver | WA | $41,335 | $12,660 | 30.63% |

| 46 | Yakima | WA | $30,835 | $9,468 | 30.71% |

| 47 | St. George | UT | $37,194 | $11,424 | 30.71% |

| 48 | Thornton | CO | $51,356 | $15,828 | 30.82% |

| 49 | Provo | UT | $30,826 | $9,516 | 30.87% |

| 50 | Paradise | NV | $35,271 | $10,896 | 30.89% |

| 51 | North Las Vegas | NV | $44,096 | $13,680 | 31.02% |

| 52 | Arvada | CO | $46,599 | $14,496 | 31.11% |

Housing costs represent the median amount spent per month. Affordability is determined by comparing annual housing costs and income.

Methodology

ValuePenguin analyzed population and rental housing cost data from the Census Bureau's American FactFinder database and Standard Home Affordability report. The 10 most populated cities in each of the following states, as determined by the 2010 Census, were included in our analysis to make up our complete west coast sample size: California, Colorado, Idaho, Montana, Nevada, Oregon, Utah, Washington and Wyoming.

About the Author

Content Marketing Manager

Callie McGill previously oversaw content partnerships for LendingTree-owned domains. She earned her B.A. in Advertising from Penn State University and her work has been published on Yahoo! News, MSN, Mashvisor and more.

Editorial Note: The content of this article is based on the author’s opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.