Average U.S. Savings Account Balance: A Demographic Breakdown

American households had a median balance of $5,300 and an average balance of $41,600 in their transaction bank accounts in 2019, according to data collected by the Federal Reserve. Transaction accounts include savings accounts as well as checking, money market and call accounts and prepaid debit cards.

The median figure gives the best approximation of how much most Americans have saved, since the average figure is heavily skewed by high-income outliers with large deposits. Of course, these numbers vary even more across different cross-sections and demographics, including by age, income, ethnicity and education, which we break down below.

The median and average bank account balance in the U.S.

The median transaction account balance of $5,300 was calculated from almost 5,800 weighted responses to the 2019 Survey of Consumer Finances, a triennial survey by the U.S. Federal Reserve. This figure only reflects responses from households that had active transaction accounts at the time of the survey. The weighted average savings account balance was $41,600.

Year | Median bank account balance | Average bank account balance* |

|---|---|---|

| 2019 | $5,300 | $41,600 |

| 2016 | $4,790 | $42,580 |

| 2013 | $4,500 | $39,690 |

| 2010 | $4,120 | $38,000 |

| 2007 | $4,960 | $32,720 |

| 2004 | $5,150 | $36,860 |

| 2001 | $5,690 | $35,170 |

Dollar amounts are in 2019 dollars.

As you can see, the typical American savings account balance has changed substantially over time. While the total amount of savings account deposits has consistently increased over time, the distribution of that total has varied widely, as seen in the disparity between average and median savings balances shown in the figures above.

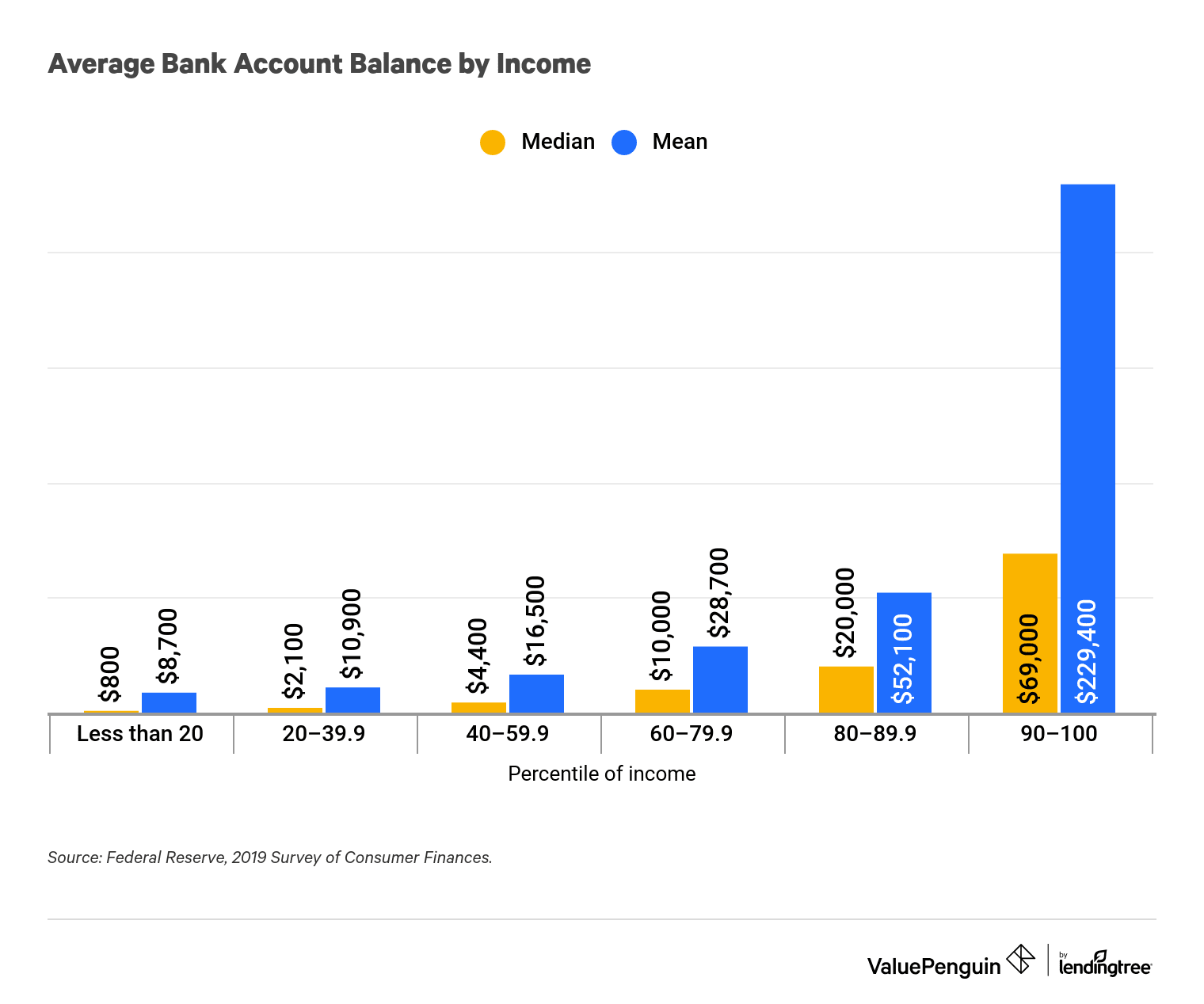

Average bank account balance by income

Unsurprisingly, the median size of household savings account balances was most heavily influenced by income. American households with higher incomes turned out to have much larger account balances compared to households in lower income groups.

Households with incomes in the 90th to 100th percentiles reported a far larger average balance than all other groups, likely because of a few extremely high-income outliers. Still, between 2013 and 2019, every income group experienced growth in their average and median account balances.

American Bank Account Balances By Income, 2016-2019

Percentile of income | 2016 average savings | 2019 average savings | 3-year change |

|---|---|---|---|

| Less than 20 | $600 | $800 | 33% |

| 20–39.9 | $1,800 | $2,100 | 17% |

| 40–59.9 | $4,000 | $4,400 | 10% |

| 60–79.9 | $8,700 | $10,000 | 15% |

| 80–89.9 | $19,900 | $20,000 | 1% |

| 90–100 | $65,900 | $69,000 | 5% |

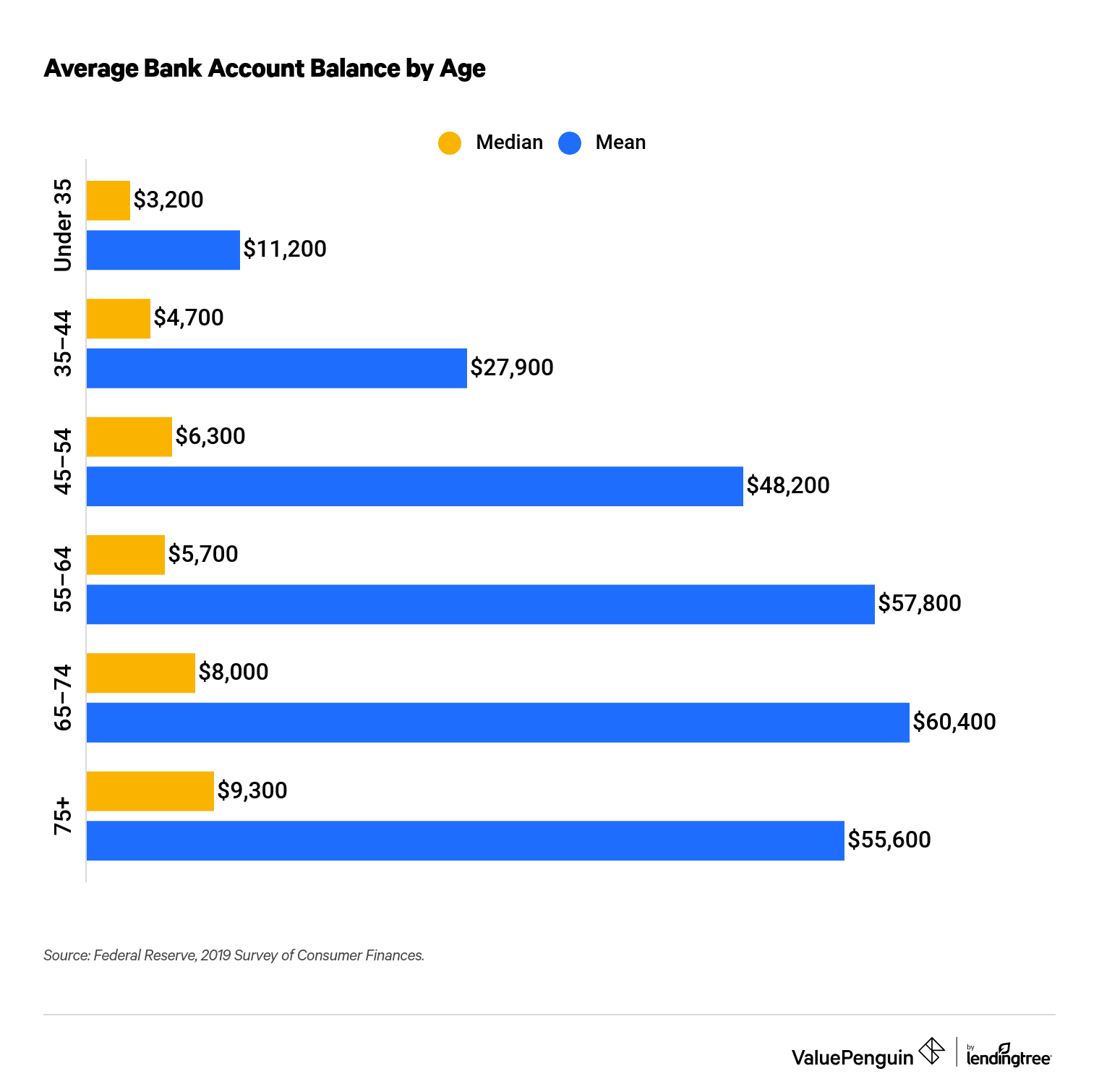

Bank account balance by age

Generally, the survey data for bank accounts supported the idea that households with older individuals are likely to have higher balances in their savings accounts. The one exception to this trend was that households headed by someone 45 to 54 years old reported a higher average balance than their older counterparts in the 55 to 64 age group.

The oldest group did report the highest median savings balance by a small margin. At the other end of the spectrum, households under the age of 35 had the lowest median balance of $3,200, along with the lowest average balance of $11,200. As in other cases, the large difference between average and median balance reflects the presence of high-income outliers in every age bracket.

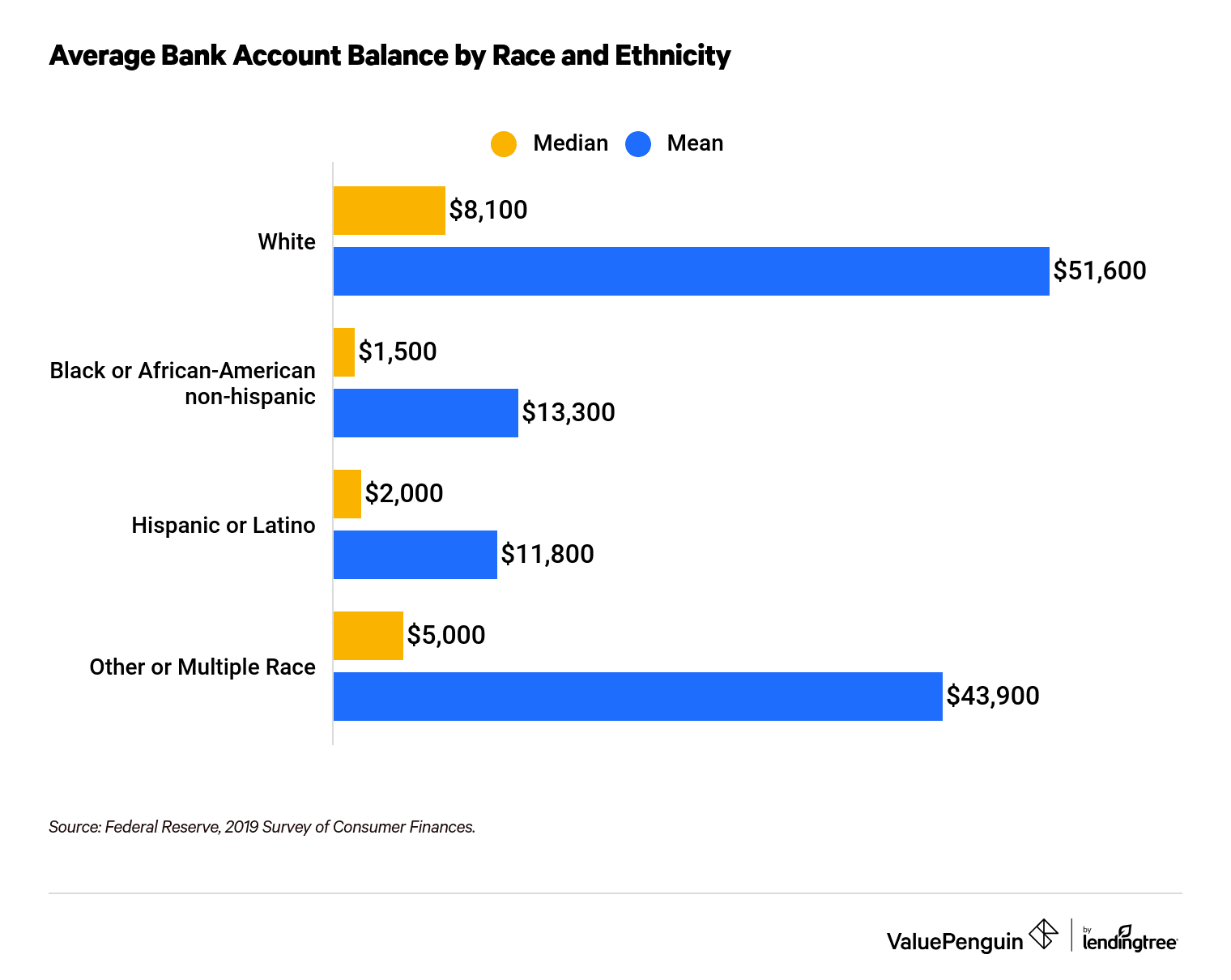

Bank account balance by race

According to the data collected by the Federal Reserve in 2019, the average account balance of Black and Hispanic households was significantly lower than the average balances for non-Hispanic whites and groups classified as "other or multiple race." According to the Federal Reserve, the "other" group in the Survey of Consumer Finances consisted of "respondents identifying as Asian, American Indian, Alaska Native, Native Hawaiian, Pacific Islander, other race and all respondents reporting more than one racial identification."

The contrasts in bank account balances between households of different races are likely due to differences in broader economic factors. Income, for instance, may be a major factor in determining the level of savings that a household accumulates. According to the Census Bureau's 2019 data, white non-Hispanic households had a median income of $76,057, while Hispanic and Black households had median incomes of $56,113 and $45,438, respectively.

Bank account balance by education level

Perhaps unsurprisingly, the Federal Reserve's data also shows that individuals with a college degree are more likely to have a higher bank account balance. This group's average balance in 2019 takes the lead over the next tier by more than $55,000.

This savings discrepancy between education levels can likely be attributed to the more extensive career opportunities — and higher pay — that are typically offered to those with higher levels of education.

Unfortunately, given the increasing cost of higher education, it may prove difficult for those with only $1,000 to $3,900 in their bank accounts — the median balance range for those without a college degree — to save and pay their way to a college degree and, thus, more robust savings.

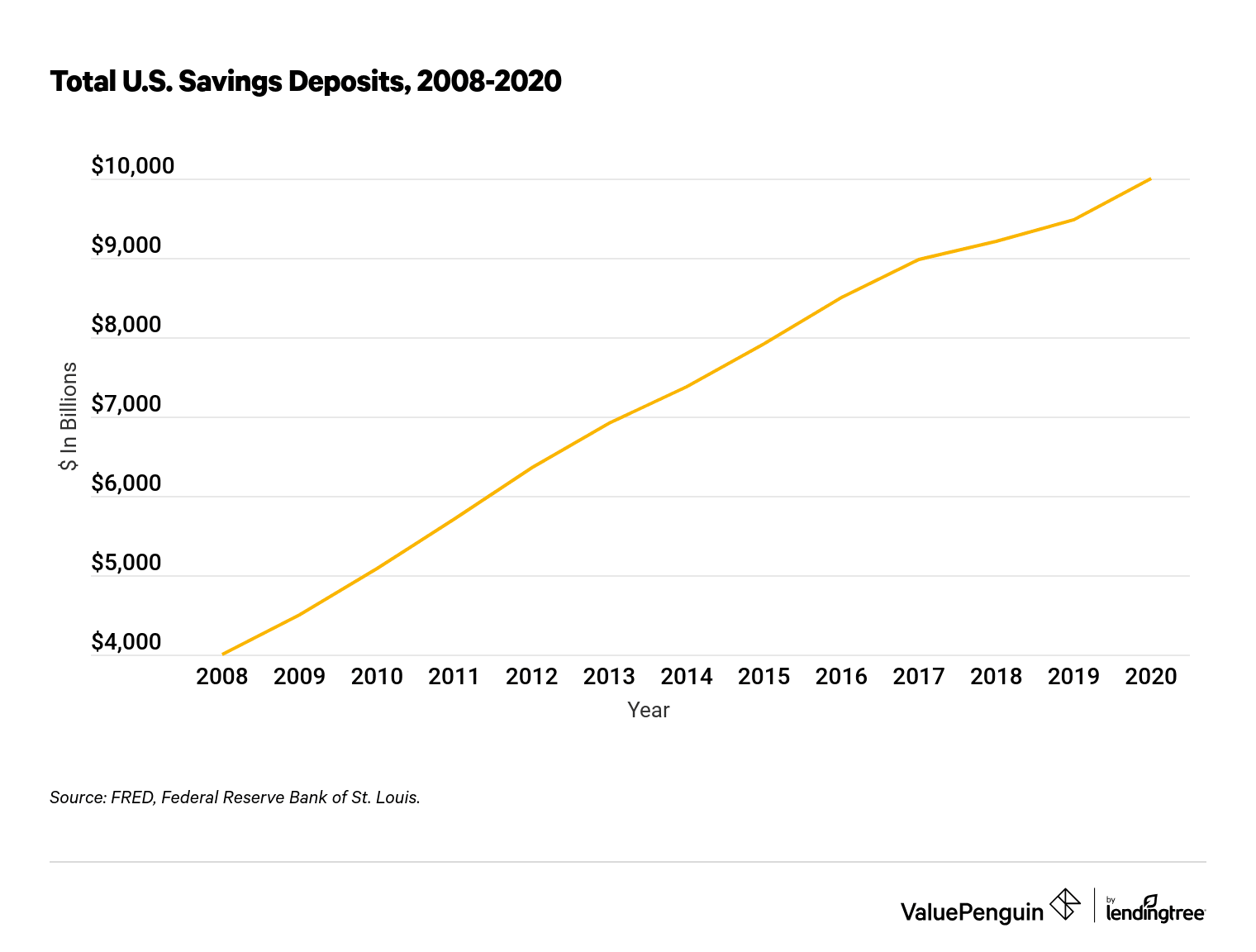

Historical trends in the average American savings account balance

Looking at savings accounts specifically, the total amount of American savings account deposits has grown steadily ever since the government started collecting data in 1959. Additionally, the economic crisis that began in 2008 prompted a sharp uptick in the rate of savings growth.

Savers similarly increased their savings rates in February 2020 when it became clear that the coronavirus pandemic would take a global economic toll. Total savings reached a fever pitch soon after the outbreak arrived in the U.S., hitting over $10.91 trillion in late April 2020.

But that positive trend in total deposits doesn't necessarily mean that the majority of U.S. households are saving more money. Per Federal Reserve data, the median transaction account balance actually decreased between 2001 and 2010, only resuming growth after 2010. Given that households across several demographics saw their savings decrease, the growth in total savings was likely due to a few households with extremely high savings.

Notably, the swift decline in interest rates on savings has not halted or slowed the growth of the savings account balance total in the U.S. Even as the national rate fell continuously since 2009, when record-keeping began, until settling at 0.06% APY from 2013 to 2018, the sum of all savings deposits continued to grow at the same pace throughout that time.

How much should you have in savings?

Now that you know what the average American savings and bank account balances look like, you're probably wondering where your savings stand and how much you should have stored away. In general, you will want to aim to have three to six months of expenses available, a figure that varies from person to person.

If you're not sure how much to save, start by aiming for three months' worth of expenses for your emergency fund. You may want to save more like six to nine months' worth, depending on your situation. This bigger savings cushion can come in handy if you have kids and a mortgage to cover, for example, or if you are your household's only source of income.

If none of these amounts are feasible for you, remember that saving any amount at any frequency is better than saving nothing at all.

How to easily boost your savings account balance

However much you set aside each month, you'll want to keep more money in an interest-bearing savings account than in your checking account, as this will give your funds a better chance at earning interest. The key to choosing a savings account is to find one that works for you — and not the other way around — which you can do by keeping these factors in mind:

- Look for a high interest rate: First, look for a high-rate savings account. A high rate will grow your money more efficiently as it sits in the account, often without you doing anything. Be aware that some accounts may have certain balance or transaction requirements.

- Make sure you're paying minimal fees: You don't want savings account fees to cut into your funds. Find an account that doesn't charge a monthly or quarterly service fee, or at least make sure that the fee is waivable through requirements you can easily meet. You can also get an account that avoids fees for overdrafts, withdrawals and ATM use to keep even more of your money where it belongs — in your savings account.

Once you have your savings account set up, another easy hack to boost your savings is to set up automatic transfers from your checking (or similar) account to your savings account. You can choose the amount and the frequency of these transfers, but making them automatic can guarantee a growing savings balance.

About the Author

Banking Writer

Lauren is a former Deposits and Investing Writer for ValuePenguin, with years of experience chasing the best savings account rates out there. She also covers deposits and investing for MagnifyMoney and DepositAccounts. Lauren’s work has been covered by the New York Times, Wall Street Journal, MSN, Univision, Acorns and more. Lauren graduated from the University of Rochester, where she majored in English. Prior to joining LendingTree, she was a writer at SmartAsset.

Editorial Note: The content of this article is based on the author’s opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.