What Is a Car Insurance Policy Number?

Your policy number is the unique number your insurance company uses to identify your account.

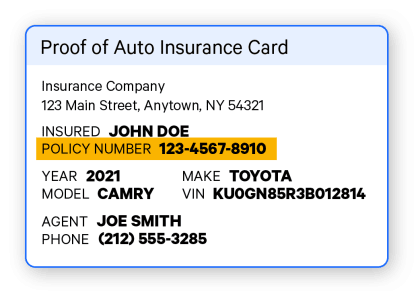

Your policy number is on your insurance card as well as bills and statements from your insurance company. You'll need your policy number after a car accident, during a traffic stop and any time you want to contact your insurance company.

Find Cheap Car Insurance Quotes in Your Area

Where can I find my car insurance policy number?

You can find your car insurance policy number on your insurance card or bill.

Your policy number is typically eight to 10 digits. If you have multiple cars, you might have all your cars listed on a single card. If you have a different number or card for each vehicle, it's common for only the last number to change. For example, one car on your policy might be 99999999-1, while another could be 99999999-2.

Your car insurance policy number will generally stay the same for as long as you stay with your company. However, your number might change if you let your policy lapse or if you change companies.

Find Cheap Car Insurance Quotes in Your Area

When do I need my car insurance policy number?

You'll need your own car insurance policy number after a car accident, during a traffic stop with the police and when you contact your company.

- After a car accident: If you're in an accident with another driver, you'll exchange insurance info, including the policy number. Each driver will use the info when filing a claim. You'll also provide your insurance card to the police if they come to the accident and file a police report. It's generally a good idea to have the police come to the scene of any accident. That's because the police report will serve as an objective record of what happened and where.

- If the police pull you over: You'll also have to provide your insurance policy number to the police during a traffic stop. The police will check to make sure you have the minimum amount of insurance your state requires.

- When contacting your insurance company: Your insurance company will likely ask for your policy number whenever you contact the company. So, you'll need it if you call to make changes to your policy or cancel your policy. However, your insurance company can generally look up your policy number using other info like your address or Social Security number.

What should I do if I lost my car insurance policy number?

If you lose your proof of insurance card, most insurance companies will mail you a paper copy or let you print out new cards from your online account.

You should keep at least two copies: a digital copy on your phone and a paper one in your glovebox. Every state except New Mexico allows you to use electronic proof of insurance on your smartphone. However, it's also good to have a paper copy as a backup. Plus, having a paper copy means you won't have to give a police officer your phone during a traffic stop.

When do I need someone else's policy number?

The most common time you'll need someone else's insurance policy number is if you're in an accident. If you're in a crash, you should ask the other driver for their insurance info, regardless of who appears to be at fault or the severity of the accident. Offering yours as well is a show of good faith and may encourage them to provide theirs.

Insurance cards can be small and difficult to read, so you should take a photo of the other driver's insurance card using your phone. That way, you don't have to depend on reading your own handwriting scribbled on the side of the road. Take a picture of the front and back of the card, and write down their full name and phone number, too.

After the accident, you'll use the other driver's insurance number when you call your insurance company and the other driver's company to file a claim.

What if I don't have all of the other driver's information?

Sometimes, especially in a high-stress environment after an accident, you might not get complete info about the other driver's insurance policy. Maybe you wrote the number down wrong or you forgot to take note of which insurance company they use. If that's the case, start by contacting the other driver, if you can. Hopefully, they'll be able to provide you with all the information you need.

If you can't reach the other driver and the police came to the scene of the crash, you can go to the police station and ask for a copy of the police report. You're entitled to a full copy of any police report that has your name on it, and the report will have the other driver's insurance info.

If you have the driver's name and policy number, but not the company name, you may be able to call around to see if you can find them.

Your own insurance agent may also be able to identify the number based on professional experience, so don't be afraid to ask.

Frequently asked questions

Is my VIN the same as my insurance policy number?

No, your VIN and your insurance policy number are different. Your car's vehicle identification number, or VIN, identifies your vehicle. VINs have 17 digits, contain both letters and numbers and are near the description of your car's make and model on the card. This is separate from your insurance policy number.

Is my insurance policy number the same as my AAA membership number?

If you get insurance coverage through a roadside assistance company like AAA, your insurance policy number will be different from your AAA membership number. You'll have a totally separate card and account identifier.

About the Author

Lead Writer

Matt Timmons is a Lead Writer on the insurance team at ValuePenguin, where he writes in-depth and timely pieces helping find the right coverage for them.

He's covered insurance at ValuePenguin since 2018, specializing in auto and home insurance, as well as life insurance. He's paid special attention to the EV insurance market, where prices are much higher than for gas cars.

Before he started writing about personal finance, Matt wrote about professional skills and online tools at an e-learning company.

How insurance helped Matt

During freshman orientation in college, Matt's iPod was stolen off his table while he was eating lunch. Luckily, he'd bought a college insurance plan the day before and he had money to buy a replacement before classes started.

Expertise

- Auto insurance

- Home insurance

- Insurance rate analysis

- Life insurance

Referenced by

- CNBC

- Miami Herald

- Yahoo! Finance

Education

- BA, Wesleyan University

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.