Loans

Average Auto Loan Interest Rates: Facts & Figures

The national average for US auto loan interest rates is 5.27% on 60 month loans. For individual consumers, however, rates vary based on credit score, term length of the loan, age of the car being financed, and other factors relevant to a lender’s risk in offering a loan. Typically, the annual percentage rate (APR) for auto loans ranges from 3% to 10%.

Average Auto Loan Rates by Credit Score

Consumers with high credit scores, 760 or above, are considered to be prime loan applicants and can be approved for interest rates as low as 3%, while those with lower scores are riskier investments for lenders and generally pay higher interest rates, as high as 20%. Scores below 580 are indicative of a consumer’s poor financial history, which can include late monthly payments, debt defaults, or bankruptcy.

Individuals in this "subprime" category can end up paying auto loan rates that are 5 or 10 times higher than what prime consumers receive, especially for used cars or longer term loans. Subprime loans are sometimes offered to people buying a car with no credit.

Consumers with excellent credit profiles typically pay interest rates below the 60 month average of 4.21%, while those with credit profiles in need of improvement should expect to pay much higher rates. The median credit score for consumers who obtain auto loans is 711. Consumers in this range should expect to pay rates close to the 5.27% mean.

When combined with other factors relevant to an applicant’s auto loan request, including liquid capital, the cost of the car, and the overall ability to repay the loan amount, credit scores indicate to lenders the riskiness of extending a loan to an applicant. Ranging from 300 to 850, FICO credit scores are computed by assessing credit payment history, outstanding debt, and the length of time which an individual has maintained a credit line.

Average Interest Rates by Term Length

Most banks and credit unions provide payment plans ranging from 24 to 72 months, with shorter term loans generally carrying lower interest rates. The typical term length for auto loans is 63 months, with loans of 72 and 84 months becoming increasingly common. The higher APRs of longer term auto loans, however, can result in excessive interest costs that leave borrowers ‘upside down’—that is, owing more on the auto loan than the car actually costs.

Here’s a closer look at average interest rates across various loan terms for those with the strongest credit.

Auto Loan Term | Average Interest Rate |

|---|---|

| 36 Month | 4.21% |

| 48 Month | 4.31% |

| 60 Month | 4.37% |

| 72 Month | 4.45% |

While longer term loans allow for a lower monthly payment, the extra months of accumulating interest can ultimately outweigh the benefit of their lower short term cost, especially for the consumer purchasing an older used car whose value will depreciate quickly.

Terms of 72 and 84 months are also usually available only for larger loan amounts or for brand new models.

For example, when paid over the course of 48 months, a $25,000 loan at a 4.5% interest rate will result in monthly payments of $570 and a total cost of $27,364. When paid over the course of 84 months in $348 monthly payments, this same loan at the same interest rate costs a total of $29,190 — more than $1,800 pricier than at 48 months. For higher interest rates, the difference between short and long term payments will be even greater.

Average Rates for Auto Loans by Lender

Auto loan interest rates can vary greatly depending on the type of institution lending money, and choosing the right institution can help secure lowest rates. Large banks are the leading purveyors of auto loans. Credit unions, however, tend to provide customers with the lowest APRs, and automakers offer attractive financing options for new cars.

Banks and Credit Unions

Most banks who offer auto loans provide similar rates as low as 3% to the most qualified customers. However, there is much variance amongst banks in the highest allowed APR, with top rates ranging from as low as 6% to as high as 25%. Banks who provide higher rate loans will generally accept applicants with worse credit, while more risk averse lenders won’t offer loans to applicants with scores below the mid-600s.

The typical large bank has specific eligibility requirements for loans, including a mileage and age maximum for cars, and a dollar minimum for loans.

Generally, credit unions extend loans at lower interest rates than banks, have more flexible payment schedules, and require lower loan minimums (or none at all, in some cases). However, credit unions tend to offer loans exclusively to their membership, which is often restricted to certain locations, professions, or social associations.

Financial Institution | Lowest Auto Loan APR | Highest Auto Loan APR |

|---|---|---|

| Alliant | 3.24% | 18.19% |

| CapitalOne | 3.99% | 13.98% |

| PenFed | 1.99% | 18% |

| PNC Bank | 2.79% | 14.99% |

Dealerships

Automakers like Ford, GM, and Honda also provide loan financing options on new cars purchased from their dealerships. This type of financing is gaining popularity amongst new car buyers and comprises about half of all auto loans. Automakers provide baseline APRs as low as 0 or 0.9% to compete with traditional financiers like banks and credit unions, while also incentivizing customers to purchase a new car off the dealer’s lot rather than a used vehicle from another vendor. Low rates are restricted to the most qualified customers with excellent credit profiles, and not all loan applicants will be approved to receive credit from automakers.

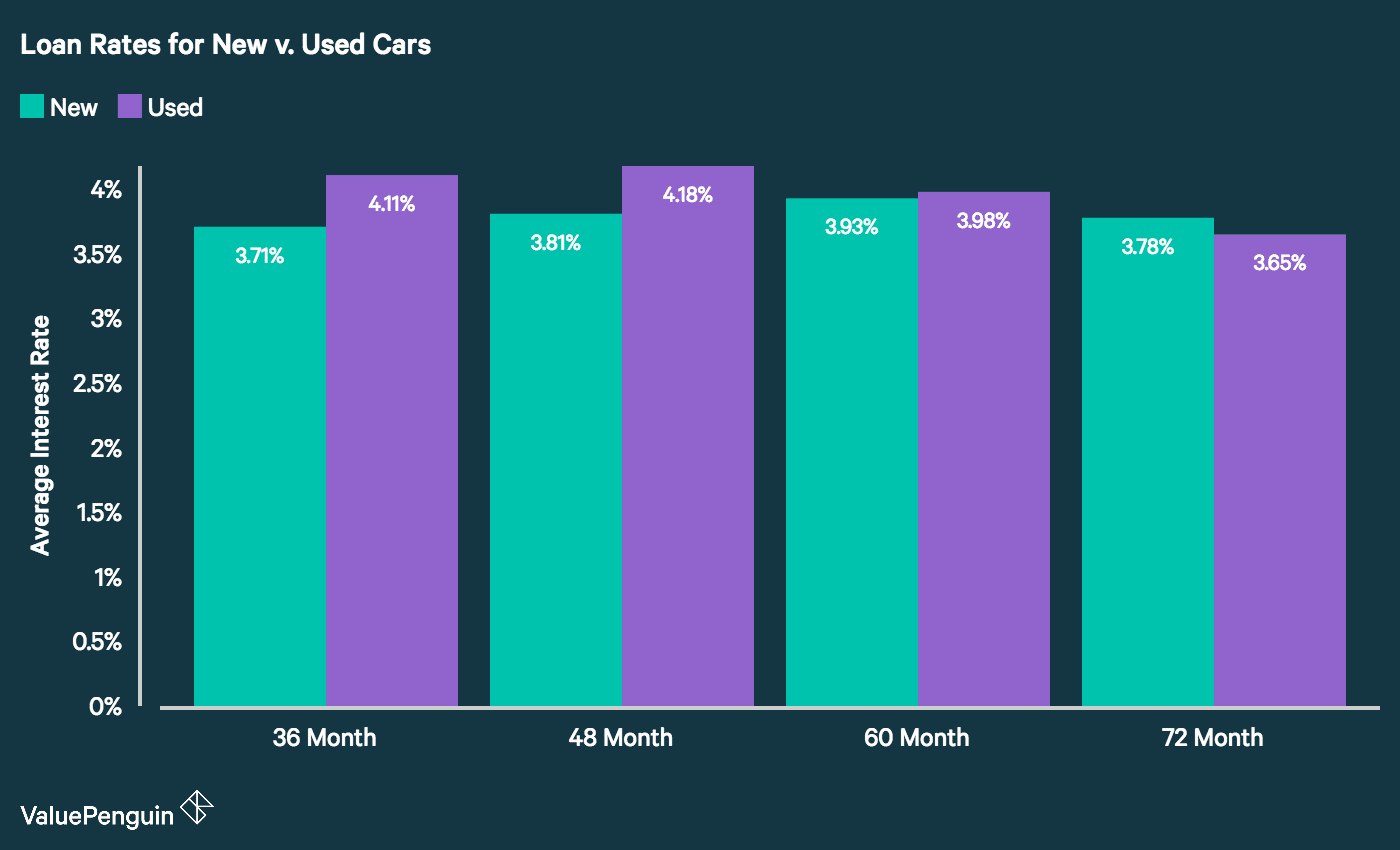

How Average Interest Rates Vary for Loans for New and Used Vehicles

The average interest rates on auto loans for used cars are generally higher than for loans on new models. Higher rates for used cars reflect the higher risk of lending money for an older, potentially less reliable vehicle. Many banks won’t finance loans for used cars over a certain age, like 8 or 10 years, and loans for the older models that are allowed often carry much higher APRs. One leading bank offers customers with good credit interest rates as low as 2.99% for purchasing a new model, but the minimum interest rate for the same loan on an older model from a private seller rises to 5.99%.

The typical auto loan drawn for a used car is substantially less than for a new model, with consumers borrowing an average of $20,446 for used cars and $32,480 for new. However, terms longer than 48 or 60 months are generally not allowed for older model used cars, as the potential risk for car failure grows with age.

Historical Auto Loan Rates

Auto loan rates are at historically low levels as a result of an overall low interest rate environment. Over the last decade, the average interest rate on a 48 month auto loan from a commercial bank has fallen by over 40%. This is largely a result of the 2009 financial crisis, after which interest rates were lowered to incentivize consumers to stimulate the economy by spending on items like cars rather than saving.

Loans from auto finance companies have historically carried lower rates than loans from commercial banks. The large car manufacturers have "captive finance" arms (e.g. Ford Finance, Chrysler Capital, GM Financial) that exclusively provide loans for consumers purchasing the parent company’s cars; this enables automakers to provide lower rates, as the car purchase, rather than the interest, is the manufacturer’s primary revenue stream.

Sources

"Consumer Credit - G.19" Federal Reserve

US Bank Auto Loans

Chase Auto Loans Calculator

myFICO Auto Loan Calculator

S&P Global Market Intelligence